You're getting ready for a mortgage application, and suddenly an old credit card account shows up in the conversation. Maybe it's a parent's card you were added to years ago. Maybe it helped you build credit at first, but now the balance is high, the history is messy, or the lender wants a cleaner file before underwriting.

That's where many people get stuck. They know the account is only there because they're an authorized user, but they're not sure whether they should remove it, how to remove it, or what happens after the removal request goes through.

Knowing how to remove authorized user status matters most when you're trying to make your credit profile easier for a mortgage lender to understand. FHA, VA, USDA, and conventional lenders all look for stability, accuracy, and manageable debt. If an authorized user account is helping, you may leave it alone. If it's creating confusion, high utilization, or documentation problems, removal may be the right move.

Table of Contents

- What Is an Authorized User and Why Does It Matter

- The Impact of Authorized User Accounts on Your Credit

- Removing an Authorized User from Your Credit Card

- Requesting Your Own Removal as an Authorized User

- Disputing the Account with the Credit Bureaus

- Expected Timelines and Credit Score Changes

- Next Steps and Frequently Asked Questions

- Frequently asked questions

- Will removing a positive authorized user account hurt my mortgage chances

- Can I remove myself if the primary cardholder will not respond

- Does removing the account close the credit card

- Will the account disappear from my credit report right away

- What should I do if I'm close to mortgage underwriting

What Is an Authorized User and Why Does It Matter

A common mortgage scenario looks like this. A couple is ready to buy their first home. Their lender pulls credit and spots an old credit card account from college. One borrower was added as an authorized user by a parent years ago. The account isn't theirs in the legal sense, but it still shows on the credit report and now it's raising questions because the balance is high.

An authorized user is someone who's allowed to use a credit card account, but the primary cardholder remains responsible for the bill. In plain English, you can have charging access without being the person the bank expects payment from.

That setup can be useful. Families often use it to help a young adult begin building credit or to make household spending easier. But when you're preparing for a home loan, the same account can become a problem if it adds risk, confusion, or extra explanation during underwriting.

Two reasons people remove authorized users

Sometimes the primary account holder wants to remove someone. That usually happens after a relationship changes, a family arrangement ends, or the account holder wants tighter control over account security.

Other times, the authorized user wants out. That often happens before a mortgage, refinance, or apartment application because they want their credit report to reflect only accounts that are their own.

Practical rule: If an account creates more underwriting questions than credit benefit, it's worth reviewing whether removal makes sense.

A clean credit report doesn't mean a perfect credit report. It means the report is accurate, understandable, and consistent with your real financial picture. That matters when a loan officer is reviewing utilization, payment history, account stability, and overall lender readiness.

If you want a broader background on how these accounts work before deciding whether to remove one, see Superior Credit Repair tradeline insights.

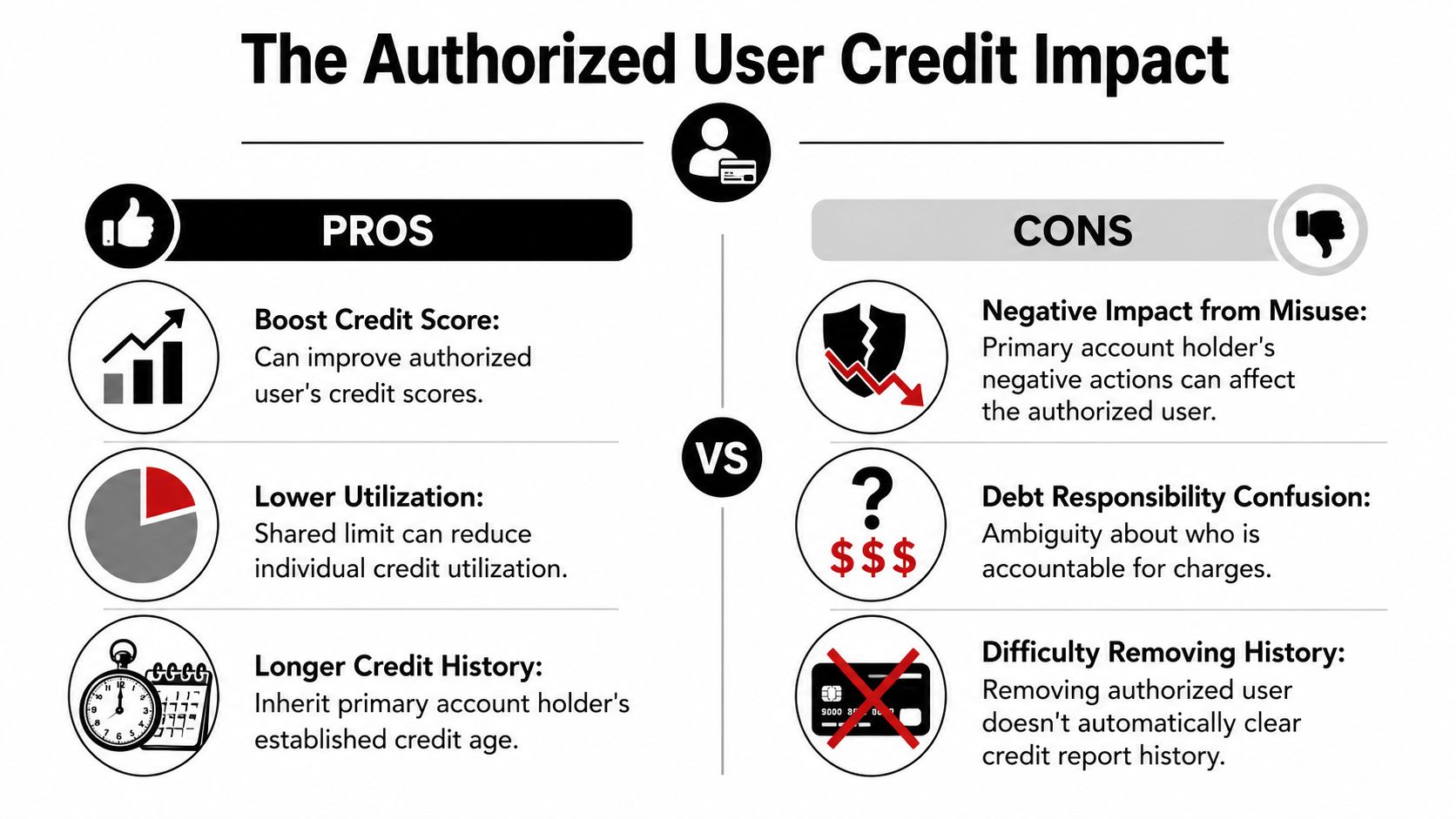

The Impact of Authorized User Accounts on Your Credit

Authorized user accounts can help or hurt. The effect depends on the age of the account, the balance, the payment pattern, and how the mortgage lender interprets it during review.

Why these accounts can help

If the primary cardholder manages the account well, an authorized user may benefit from the account's established history. That can make a thin credit file look more seasoned and sometimes improve how the overall profile appears.

A strong authorized user account may support these areas:

- Payment history: An account with clean history can make your report look more stable.

- Utilization: If the card has a modest balance relative to its limit, it may help your revolving profile look healthier.

- Credit age: Older accounts can make a file appear more mature.

- Account mix: It can add another revolving line to the report.

- Overall profile depth: Some borrowers look more established with more reporting history.

That said, mortgage preparation isn't just about whether an account helps a credit score. It's also about whether the file makes sense to an underwriter.

Why they can also become a mortgage problem

A good authorized user account can still be a liability when you're trying to qualify for financing. If the balance is high, the lender may ask questions about access, responsibility, or whether the account should be counted in any part of the review. Even when it doesn't create a direct debt obligation, it can complicate the file.

Here's where readers often get confused. They assume a “positive” authorized user account is always worth keeping. That isn't always true for a homebuyer.

| Issue | Why it matters before a mortgage |

|---|---|

| High balance | It can make your revolving profile look strained |

| Recent account activity | It may raise underwriting questions about who is using the card |

| Late or uneven history | It can make the file harder to explain |

| Relationship changes | Divorce, separation, or family conflict can create documentation issues |

| Dependence on another person's account | Lenders often prefer a borrower to show stable credit in their own name |

Even if the account helped you in the past, your goal before a mortgage is often independence and clarity. You want the lender to see a credit profile that reflects your own habits, your own obligations, and your current ability to manage debt.

If you've noticed an unexpected change after being added to or tied to another person's account, this guide on what causes credit scores to fall can help you think through the reasons.

Removing an Authorized User from Your Credit Card

If you're the primary cardholder, the removal process is usually straightforward. For most major issuers, you can remove an authorized user by calling the number on the back of the card or by using the bank's online or mobile account tools, according to CFPB guidance on removing an authorized user.

The practical steps for the primary cardholder

Think of this as an account maintenance request, not a credit bureau dispute. The bank is changing who has access to the account.

A clean process usually looks like this:

Verify your identity

The issuer will confirm that you're the primary cardholder or otherwise authorized to make account changes.Request removal clearly

State that you want the authorized user removed from the account. Use the person's full name as it appears on the card account.Ask about immediate shutdown

Confirm whether the physical card, digital wallet access, and any app-based permissions are disabled right away.Discuss a new card number if needed

If the authorized user had access to the full card number, ask whether the issuer recommends issuing a new number to prevent post-removal misuse.Review recurring charges

Don't assume saved payment methods disappear on their own. Merchant billing tokens or stored credentials may still be active until updated.Document the request

Keep notes of the date, time, representative name, and what you were told. If the situation is sensitive, a written follow-up can help create a paper trail.

The most common mistake is removing the person from the account but leaving the card number active in subscriptions, digital wallets, or stored merchant profiles.

CFPB guidance also says the removed user should be notified after the account change is complete. That's not just courtesy. It reduces confusion and helps prevent accidental use after access should have ended.

A simple phone script you can use

If you're nervous on the call, keep it simple:

“I'm the primary cardholder. I want to remove an authorized user from my account today. Please confirm when their card access and digital access will stop. If they had access to the account number, please tell me whether I should request a new card number as well.”

If the representative says the online portal can do it faster, use the portal. If they say a secure message or written request is better for documentation, follow that instruction and save a copy.

Bank procedures vary. In many cases the change takes effect immediately, but you should still confirm exactly what “removed” means at that issuer. It may mean card privileges stop at once while background systems update afterward.

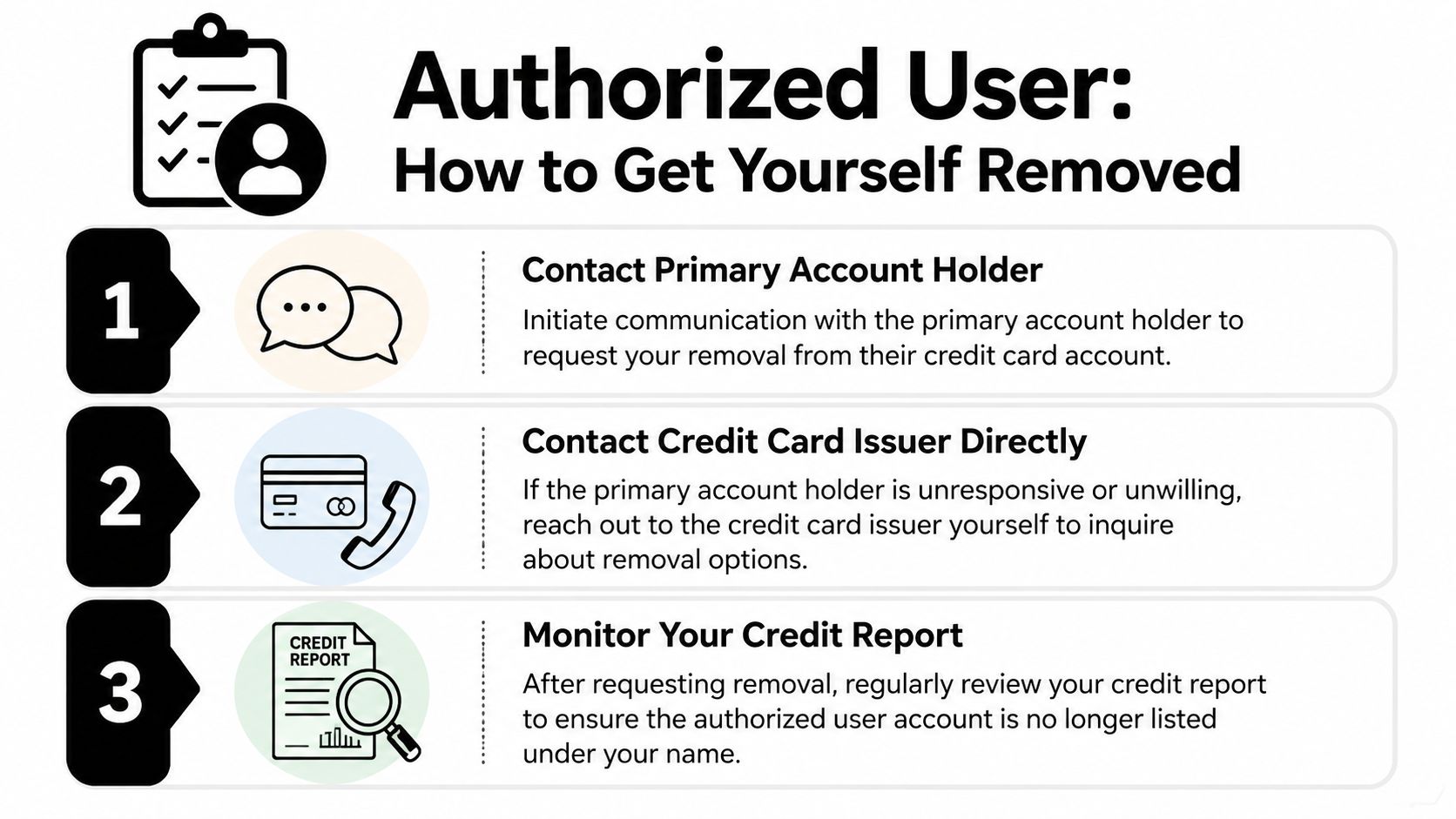

Requesting Your Own Removal as an Authorized User

If you're the authorized user and want your own name removed, the process can feel less predictable. That's because some issuers still want the primary cardholder involved, while others may process your request directly after identity verification.

Start with the cleanest path

The simplest route is usually to contact the primary cardholder first and ask them to request your removal. That avoids delay and gives the bank the clearest authorization trail.

Use plain language. You don't need to overexplain.

Try something like this:

- Keep it direct: “I'm preparing for a mortgage and need my credit report to reflect only my own accounts.”

- Ask for confirmation: Request a screenshot, secure message copy, or written confirmation once the bank processes the removal.

- Set a short timeline: If you're on a lending deadline, say so.

This approach works best when the relationship is stable. If it isn't, move quickly to the issuer.

If the primary cardholder will not help

When the primary won't cooperate, isn't reachable, or the relationship has ended, contact the card issuer yourself. Bankrate notes that the cleanest method is to ask the issuer to remove you as an authorized user and confirm whether the bank requires identity verification or follow-up from the primary cardholder. Policies vary, and some issuers may still honor the request depending on internal policy, as described in Bankrate's overview of removing yourself as an authorized user.

Here's the part many borrowers miss. Removal from the account doesn't always erase every form of access instantly across all systems. Stored card numbers, subscription billing tokens, and merchant-initiated charges may continue until the merchant updates the credentials.

If you've used that card anywhere, do this before or right after removal:

- Replace payment methods: Update subscriptions, streaming services, delivery apps, and any autopay merchants.

- Remove wallet access: Delete the card from Apple Pay, Google Wallet, or similar tools if you ever had access.

- Monitor statements if possible: If the relationship allows, ask the primary holder to watch for post-removal transactions.

If mortgage timing matters, don't assume the credit report will reflect the change just because the card stops working. Account access and credit reporting are related, but they aren't the same thing.

Another point to verify is reporting. Some issuers and bureaus may handle the post-removal history differently. If you're trying to become mortgage-ready, confirm what will happen rather than assuming one universal rule applies across every system.

Disputing the Account with the Credit Bureaus

Removing yourself from the credit card account and removing the tradeline from your credit report are not always the same event. That distinction causes a lot of stress for mortgage applicants.

A lender may pull your report and still see the account even after the bank has already ended your authorized user access. That doesn't always mean anything is wrong. It may mean only that the reporting cycle hasn't caught up yet, or the bureaus haven't updated the file.

Why removal from the card is not always the end

The issuer controls account access. The credit bureaus control what appears on your report based on furnished data. If the account still reports after you've been removed, you may need to dispute the reporting and explain that you are no longer associated with the account as an authorized user.

This is where documentation matters. Save every piece of evidence connected to the removal request.

Helpful records include:

- Issuer confirmation: Any letter, secure message, email, or call note showing that you were removed

- Proof of identity: A copy of identification and proof of address if the bureau requests it

- Credit report copy: Highlight the account you are disputing

- Short explanation: State that you were an authorized user, you've been removed, and you request the report be updated to reflect that status

What to include in your dispute

You can dispute online or by mail, but many consumers prefer written disputes when they're close to a mortgage process because written records are easier to organize and resend if needed.

A basic dispute letter can follow this structure:

| Part of letter | What to say |

|---|---|

| Your identifying information | Full name, address, date of birth, and report reference details if available |

| Account identification | Creditor name and account reference as shown on the report |

| Reason for dispute | State that you were listed as an authorized user and have been removed from the account |

| Requested action | Ask the bureau to investigate and update or remove the account from your file as appropriate |

| Supporting documents | List copies of the proof you included |

A simple wording example:

I am disputing the reporting of this account on my credit file. I was listed only as an authorized user and I have been removed from the account. I am requesting an investigation and an update to my credit report based on my current non-associated status.

Keep the letter factual. Don't add arguments you can't document. Don't exaggerate. Mortgage underwriting responds better to clean records than emotional explanations.

If you want a model for organizing a compliant written dispute, review these steps for writing a credit dispute.

For borrowers dealing with multiple reporting issues at once, including authorized user confusion plus collections, late payments, or outdated account information, Superior Credit Repair can review your reports, identify questionable items, and explain a documentation-based plan. That kind of review doesn't guarantee any particular result, but it can help you decide what to challenge, what to leave alone, and what to fix before you apply for a mortgage.

Expected Timelines and Credit Score Changes

People usually want two answers right away. How long will this take, and what will it do to my score? The honest answer is that both depend on who initiates the change, how the issuer handles reporting, and what role the account was playing in your overall file.

What usually happens first

On the issuer side, the access change is often handled quickly. As noted earlier from the CFPB-linked guidance, many issuers process removal as a customer service account change, and Bankrate notes that it should take effect immediately in many cases, though procedures vary by bank.

That doesn't mean your credit report will look different the same day. Reporting systems update on their own schedules, and if you need the tradeline changed on the report itself, the credit bureau side may take longer.

For mortgage applicants, the practical lesson is simple. Build in time. Don't wait until the week before underwriting to start removing an account that may need follow-up documentation.

If you're trying to coordinate this with a larger homebuying timeline, this mortgage readiness credit timeline can help you think about sequencing.

How your score might react

Here, expectations need to stay realistic.

If the authorized user account had a high balance or problematic history, removing it may help your profile look cleaner. If the account was older and well managed, removal could reduce some of the benefit you were receiving from that account's age or utilization profile.

That means a score can move in either direction, or not move much at all. None of those outcomes automatically means the decision was wrong.

A mortgage-ready profile is not always the same as the highest possible score on paper. Lenders also care about clarity, stability, and whether the report reflects your own credit behavior.

For many homebuyers, removing an authorized user account is less about chasing a quick score change and more about reducing underwriting friction. A cleaner, more independent file can make the loan process easier to explain and document.

Next Steps and Frequently Asked Questions

If you're trying to figure out how to remove authorized user status before applying for a mortgage, stay focused on the order of operations. First decide whether the account is helping or hurting. Then contact the issuer through the right channel. After that, document everything and watch your credit reports carefully.

If the account is tied to a larger credit cleanup, professional guidance can be useful. If you've been asking can you pay for credit help, the key is choosing a process-driven, compliance-focused option that explains your rights, reviews your documentation, and avoids guarantees.

Frequently asked questions

Will removing a positive authorized user account hurt my mortgage chances

It might change your score or the appearance of your file, but that doesn't automatically hurt your mortgage chances. If the account creates confusion, high utilization, or dependency on someone else's credit, removal may still be the better move.

Can I remove myself if the primary cardholder will not respond

Sometimes yes. Issuer policies vary. Contact the card issuer directly, verify your identity, and ask whether they will process an authorized user removal request without the primary holder.

Does removing the account close the credit card

No. Removing an authorized user usually removes that person's access. It does not usually close the primary cardholder's account.

Will the account disappear from my credit report right away

Not always. The account may continue to appear until the next reporting cycle or until you dispute the reporting if an update is still needed.

What should I do if I'm close to mortgage underwriting

Move early, keep records, and avoid assumptions. Confirm the account change with the issuer, update any saved payment methods, and review your reports so you know exactly what a lender is likely to see.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation to better understand your options.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

Superior Credit Repair provides educational support for consumers working on credit repair, credit restoration, and mortgage readiness. If you want help reviewing your credit report for inaccurate, outdated, unverifiable, or misleading items, or you need a clearer plan before applying for home, auto, business, or personal financing, you can learn more through Superior Credit Repair.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile.