A collection letter often shows up at the worst time. Maybe you're getting ready to apply for a mortgage, trying to qualify for an auto loan, or cleaning up old accounts so your credit report makes more sense. Then a collector sends a notice for a debt you barely recognize, an amount looks off, or the account is so old that you're not even sure who originally owned it.

That's where a free debt validation letter can help. It gives you a formal way to ask the collector to prove what they're trying to collect. This also allows you to slow the process down and respond carefully instead of reacting out of stress. For people working on credit repair, credit restoration, or mortgage credit repair, that distinction matters.

Many consumers also get tripped up by a second issue. A debt validation letter goes to the collector. A credit report dispute goes to the credit bureaus. Those are separate processes, and knowing how they work together can make your next steps much clearer.

Table of Contents

- Understanding the Debt Validation Letter and Your Rights

- When to Send a Debt Validation Letter and When to Pause

- What to Include in Your Letter Free Templates

- How to Send Your Letter to Create a Legal Paper Trail

- Common Pitfalls and Advanced Strategies

- From Debt Validation to a Lender-Ready Credit Profile

Understanding the Debt Validation Letter and Your Rights

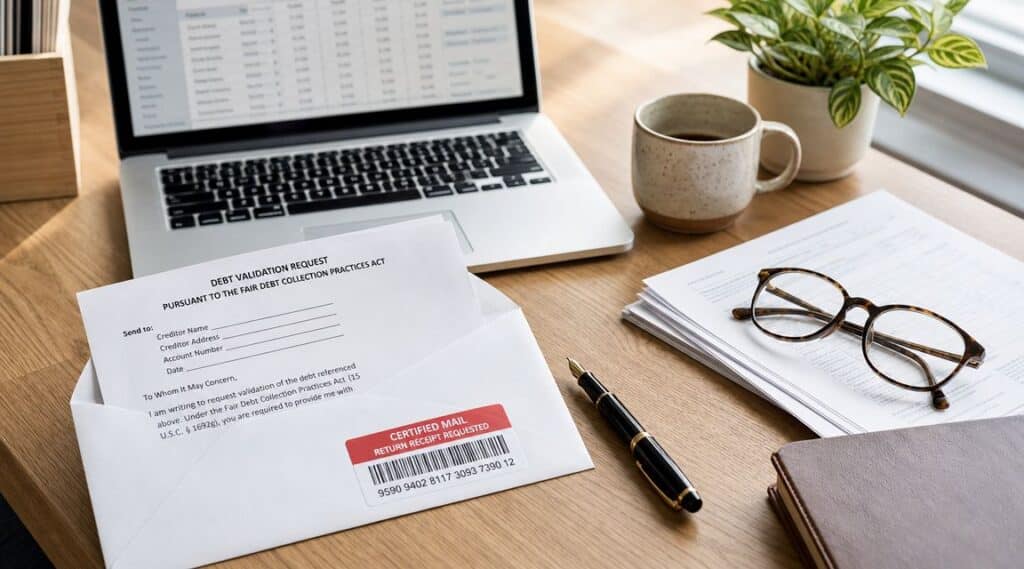

You open a collection notice while trying to get your credit ready for a mortgage. The letter says you owe money, the balance looks unfamiliar, and your first instinct is to either pay fast or set it aside. A debt validation letter gives you a more careful option. It lets you ask the collector to show the basis for the claim before you decide your next move.

Why this letter matters

A debt validation letter is part of the Fair Debt Collection Practices Act process. That matters because the FDCPA governs what a debt collector must tell you and how you can dispute a collection claim with that collector. The Consumer Financial Protection Bureau explains that a collector generally must send a validation notice with key information about the debt and your dispute rights under federal law, including how to dispute it in writing within the validation period, in its guide to debt collection communications and validation information.

That is different from a credit report dispute under the Fair Credit Reporting Act. The FCRA process is the one you use with Equifax, Experian, and TransUnion, or with a data furnisher, when an account is being reported inaccurately. The two systems work like two separate lanes on the same road. One lane asks the collector, "Prove you have the right debt and the right amount." The other asks the credit bureaus, "Correct or remove inaccurate reporting."

This distinction gets missed in a lot of guides, and it matters if you are preparing for mortgage underwriting. A lender does not only care whether a collection exists. The lender also cares whether your file is accurate, documented, and stable. Before you pay, settle, or negotiate, you need to know whether the debt is yours, whether the amount is right, and whether the collector can back up the claim with records.

Practical rule: A collection notice is a claim, not automatic proof.

This can be especially useful with old collections, medical bills, charged-off accounts, or debts sold from one company to another. If collection calls and pressure are part of the problem too, this resource offers help for Utah individuals overwhelmed by debt.

What a collector must tell you

A proper validation notice should give you a starting file to review. The Federal Trade Commission explains that debt collectors must provide basic information such as the name of the creditor and the amount of the debt, along with information about your right to dispute it, in its overview of debt collection FAQs and consumer rights.

In plain language, your letter asks for the foundation behind the demand. You may want enough detail to confirm the original creditor, the amount being claimed, account-level records, and whether the collector has connected the debt to you correctly. If names, balances, or dates do not line up, that can affect more than the collection file. It can also affect what appears on your credit reports.

That is where the FDCPA and FCRA can work together in a mortgage-prep strategy. First, you deal directly with the collector and request validation. Then, if the account is being reported inaccurately to the bureaus, you use the separate credit reporting dispute process to address the tradeline itself. One process tests the debt claim. The other tests the accuracy of the reporting.

If you are still sorting out your options at a broader level, some readers start with educational material on free credit repair in Alabama and what real help can look like.

When to Send a Debt Validation Letter and When to Pause

A common mistake happens right after a collection notice arrives. Someone sees the balance, gets anxious about credit damage, and either pays too fast or disputes the wrong thing with the wrong party. For mortgage preparation, timing matters because you may be dealing with two separate tracks at once. Debt validation under the FDCPA is your request to the collector for proof and account details. A credit report dispute under the FCRA is your request to the bureaus to investigate whether the tradeline is being reported accurately. Those tracks can support each other, but they are not the same process.

The best time to send a debt validation letter is usually soon after the collector's first written notice. The Consumer Financial Protection Bureau explains that a debt collector must send a validation notice and that you generally have a 30-day period to dispute the debt in writing after receiving it, as outlined in the CFPB's debt collection rule summary and validation notice guidance. Sending your letter during that window preserves some of the strongest procedural protections tied to validation.

Send the letter when the account raises a real identification or balance question, such as:

- You do not recognize the account. The collector's name may be unfamiliar, or the original creditor may not be clear.

- The amount appears off. Interest, fees, credits, or prior payments may not match your records.

- The debt may belong to another person. Mixed files and identity confusion still happen.

- The account is old and you need facts before discussing payment.

- You are preparing for mortgage underwriting and need to confirm what is owed before deciding whether to settle, document, or dispute reporting.

A simple way to view the timing question is this. Validation checks the collector's claim. Credit reporting disputes check the accuracy of what appears on your reports. If a collection account shows up while you are getting ready for a home loan, start by confirming the debt with the collector if the claim itself is unclear. If the tradeline on your reports also contains wrong dates, balances, or ownership details, that is a separate FCRA issue to address with the bureaus.

Pause when the account is old, unclear, or tied to a larger strategy

Pause does not mean ignore it. Pause means avoid casual phone calls, avoid admissions, and avoid making a payment before you understand the account.

That matters most with older debts. Depending on state law, making a payment or acknowledging a debt can create legal and strategic issues you did not intend. The Federal Trade Commission warns consumers to be careful with time-barred debt and to understand the consequences before agreeing to pay, in its guidance on old debts and debt collection rights.

A careful approach makes sense in situations like these:

| Situation | Why a pause helps |

|---|---|

| Very old account | You may need to confirm age, ownership, and enforceability before discussing payment |

| Limited records | Missing statements, changing account numbers, or sold debt can make the file harder to verify |

| Fintech or app-based debt | The payment history and contract trail may require closer review |

| Mortgage prep with tight timelines | You may need to coordinate collector validation, bureau disputes, and lender documentation in the right order |

For borrowers trying to clean up a file before underwriting, cost and timing often shape the plan too. If you are comparing outside help with a do-it-yourself approach, this breakdown of what people really pay for credit repair in Alabama can help you set expectations.

One final timing point matters. Written requests create a paper trail. The CFPB provides sample letters for disputing a debt with a collector, and using mail with tracking gives you proof of when the request was sent and received, which is useful if the account later becomes part of a reporting dispute or underwriting review, as shown in the CFPB's sample letters for debt collection responses.

Keep the letter factual, limited, and in writing. You are asking for information, not starting a negotiation.

What to Include in Your Letter Free Templates

A good free debt validation letter is simple, specific, and restrained. It doesn't need dramatic legal language. It needs clear identification, a direct dispute, and a focused request for documentation.

The process is more standardized now. The Consumer Financial Protection Bureau's model forms reflect current debt-collection rules, and modern notices are expected to include an itemized breakdown of the debt, including principal, fees, interest, and credits, plus account details when available, as described in Experian's overview of debt validation letters.

The core pieces every template should contain

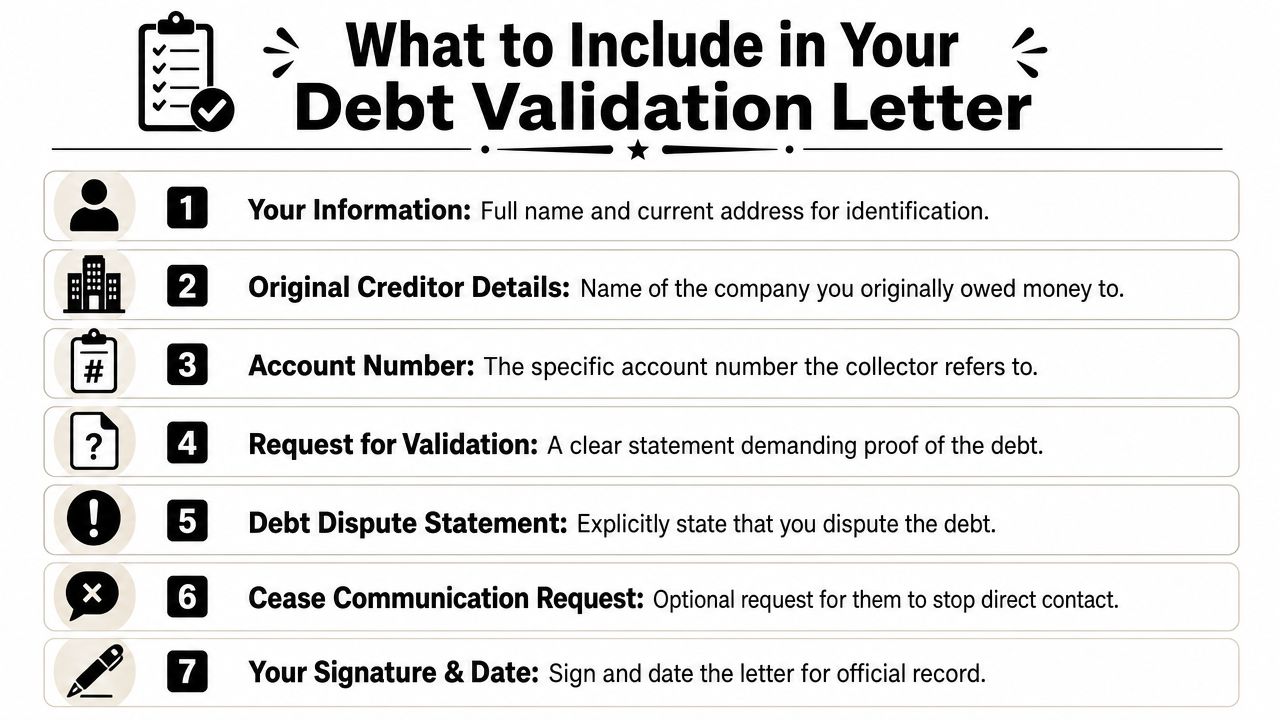

Include these basics in your letter:

- Your identifying information. Your full name, current mailing address, and the date.

- Collector reference details. The account number or reference number listed in the notice.

- A direct dispute statement. State that you dispute the debt and request validation.

- A request for documentation. Ask for the original creditor, amount claimed, and supporting account details.

- A limited-purpose tone. Make clear you are requesting validation, not admitting liability.

- Your signature. Sign and keep a copy for your records.

You can also ask for an itemization of the balance if the amount doesn't make sense. That's useful when someone is trying to rebuild credit after multiple collections or sort out charge-off dispute help before buying a home.

For readers comparing cost and process questions around credit restoration services, this guide on credit repair costs in Alabama and what people really pay gives additional context on the broader dispute and review process.

Free debt validation letter template for a standard dispute

Use this when you received a collection notice and need basic proof.

[Your Full Name][Your Address][City, State ZIP][Date] [Collector Name][Collector Address][City, State ZIP]Re: Account Number [Account Number]

To Whom It May Concern,

I am writing in response to your recent notice regarding the account referenced above. I dispute this debt and request validation of the account.

Please provide the name of the original creditor, the amount you claim is owed, and documentation supporting your claim that I am legally responsible for this debt.

Please also provide any account details you have available that support the balance and ownership history of this account.

This letter is not a refusal to pay. It is a request for validation and documentation of the alleged debt.

Sincerely,

[Your Signature][Your Printed Name]

Why these lines matter:

- “I dispute this debt.” That tells the collector this is not a routine inquiry.

- “Request validation.” That frames the letter around the legal process, not negotiation.

- “Not a refusal to pay.” That helps keep the tone factual and avoids unnecessary escalation.

- “Original creditor.” This is critical when debt has been sold or reassigned.

Template for a more detailed itemization request

Use this version when the amount looks inflated or confusing.

[Your Full Name][Your Address][City, State ZIP][Date] [Collector Name][Collector Address]Re: Account Number [Account Number]

To Whom It May Concern,

I dispute the alleged debt referenced above and request full validation.

Please provide the name of the original creditor, the amount claimed, the date of last payment, and an itemized breakdown of the balance, including any principal, interest, fees, and credits included in your calculation.

If available, please include documents showing the basis for the amount you are attempting to collect and the account details associated with this debt.

This correspondence is for the purpose of requesting validation of the alleged debt.

Sincerely,

[Your Signature][Your Printed Name]

This version is useful for collections dispute help, especially where balances grew over time and you need to separate the original account from later charges.

Template for a medical collection account

Medical collections often confuse consumers because the provider, billing company, and collector may all be different.

[Your Full Name][Your Address][City, State ZIP][Date] [Collector Name][Collector Address]Re: Account Number [Account Number]

To Whom It May Concern,

I am writing to dispute the medical debt referenced above and request validation.

Please provide the name of the original medical provider or creditor, the amount you claim is owed, and documentation showing the account details associated with this collection.

If available, please include the date of service, the date of last payment, and any itemization that explains how the current amount was calculated.

This letter is a request for validation of the alleged debt.

Sincerely,

[Your Signature][Your Printed Name]

Medical collection credit repair often requires separate follow-up. The collector issue is one track. The credit reporting issue may be another.

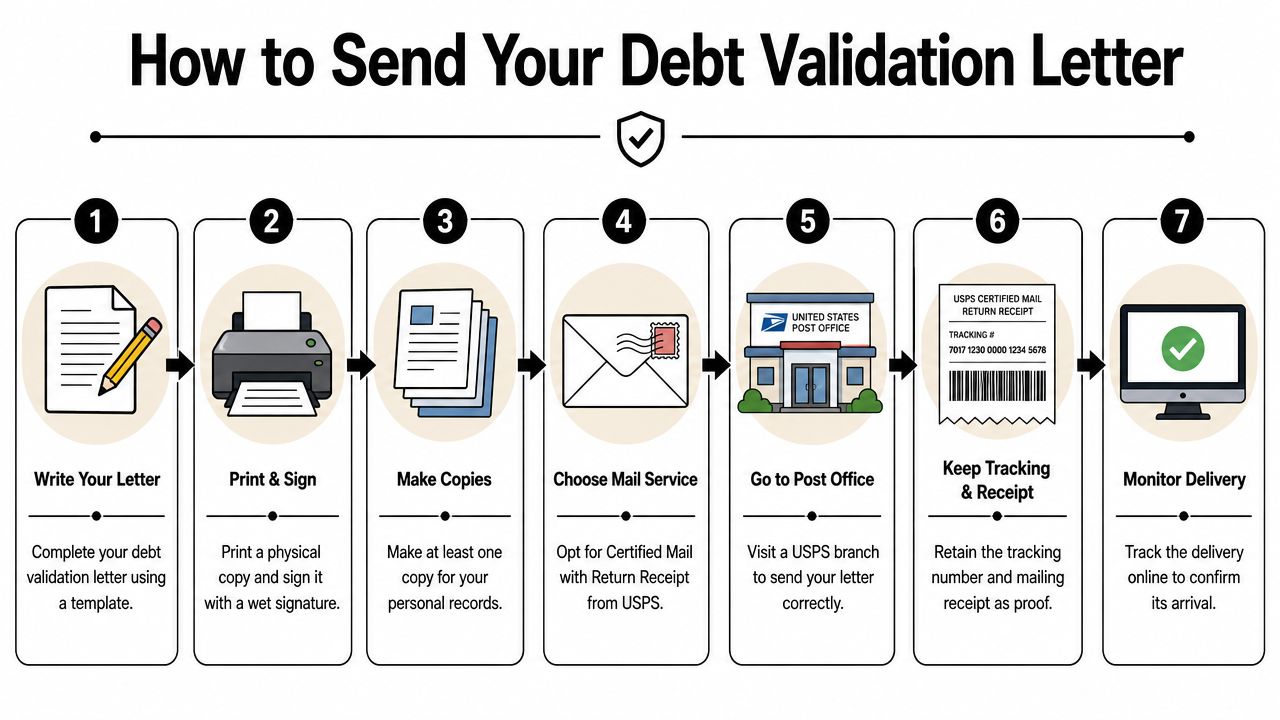

How to Send Your Letter to Create a Legal Paper Trail

You send the letter, wait two weeks, and then a collector says it never arrived. That is the problem this step solves.

A debt validation letter does two jobs at once. It asks the collector to verify the account under the FDCPA, and it creates a dated record of what you asked for and when you asked for it. For mortgage preparation, that record can matter later if an underwriter asks how you handled a collection account. It also helps you keep the FDCPA track separate from the FCRA track, which is your dispute process with the credit bureaus.

Mailing method matters

If you want a paper trail, send the letter in a way you can prove. The collector may process thousands of letters. Your goal is to be able to show the date you mailed it, the address you used, and whether delivery was completed. The USPS Certified Mail service page explains the mailing options that give you mailing and delivery records.

A simple routine works well:

- Print the final letter. Keep the version you sent.

- Sign and date it. That helps show it was a formal written request.

- Make a copy before mailing. A scanned PDF is fine if it is readable.

- Use USPS Certified Mail or another trackable mailing service. Tracking is what turns a letter into evidence.

- Save the receipt, tracking number, and delivery confirmation. Put them with the letter copy.

A good paper trail works like a receipt folder for a large purchase. If questions come up later, you are not relying on memory.

What to keep in your records

Set up one file for each collection account. Physical, digital, or both is fine. The important part is consistency.

Keep these items together:

- The collector's first notice. Keep the envelope if it shows a date.

- Your signed letter. Save the exact copy you mailed.

- Mailing proof. Store the receipt and tracking details.

- Delivery proof. Save confirmation once the letter is delivered.

- Any collector response. Letters, statements, or account summaries all belong in the file.

- Your credit report snapshots. At this point, the FDCPA and FCRA processes start to separate clearly.

That last item causes confusion for many consumers. A validation letter goes to the collector and asks, “Show me what you are collecting and why.” A credit bureau dispute asks the bureaus, “Show me why this account is being reported this way.” Those are different legal tracks. If you are preparing for underwriting, keeping both records side by side helps you show a clean timeline of what was challenged, what was verified, and what was corrected. Readers who want more context on how reporting codes can affect review may also want to understand what HRRG means in the credit reporting context.

Why this matters later

A documented mailing process can help in three common situations. The collector says your request was never received. The collector responds with incomplete information and you need to compare dates and documents. A lender asks for an explanation of a collection account during mortgage review.

In each case, your records make the conversation simpler. You are no longer saying, “I think I sent something.” You are showing what you sent, when you sent it, and what happened after that.

Keep the process organized and plain. Clear records usually carry more weight than long explanations.

Common Pitfalls and Advanced Strategies

Most mistakes happen when people act too quickly. They call the collector, start explaining their life story, or offer a small payment to “show good faith” before they know whether the account is accurate or enforceable.

Mistakes that can hurt your position

Avoid these common errors:

- Admitting the debt casually. Keep your language neutral until documentation is reviewed.

- Handling everything by phone. Written communication creates a better record.

- Ignoring age-related issues. Older accounts need a more careful strategy.

- Assuming validation equals deletion. Collector proof and bureau reporting are not the same thing.

A validation request can ask for the original creditor, amount owed, last payment, and whether the statute of limitations has expired, which highlights how central age and enforceability are, especially with fintech or BNPL-related accounts, according to OVLG's explanation of debt validation requests.

How to think about fintech and BNPL collections

Fintech and Buy Now, Pay Later accounts can be messy. The consumer may remember using an app, but not the lender behind it. The collector may have limited records. The credit reporting may not match how the account was originally presented.

That's why documentation matters more, not less.

Ask questions such as:

- Who was the original creditor?

- What was the date of last payment?

- Is the claimed balance fully explained?

- Is the account still legally enforceable?

For consumers dealing with several account types at once, including collections, late payments, or charge-offs, services like credit repair support from Superior Credit Repair can be one way to organize a documentation-based review of the full credit file. The key is to keep the process factual. Results vary, and the right strategy depends on the account history, reporting details, and supporting records.

From Debt Validation to a Lender-Ready Credit Profile

A free debt validation letter is often the first smart move when a collection account appears out of nowhere or doesn't look right. It helps you ask better questions, preserve your records, and avoid rushing into payment decisions without documentation.

But it's only one part of a stronger credit strategy. A lender-ready file usually requires more than addressing one collection. You may also need to review late payments, utilization, charge-offs, reporting accuracy, account stability, and how your current behavior supports long-term rebuilding. That's especially true for first-time homebuyers preparing for FHA, VA, USDA, or conventional loan review.

If you're trying to connect individual disputes to a larger financing goal, it can help to look at the broader picture of credit repair and consulting in Birmingham, Alabama. The right next step isn't always immediate dispute activity. Sometimes it's a full file review, a timeline, and a realistic plan.

FAQs

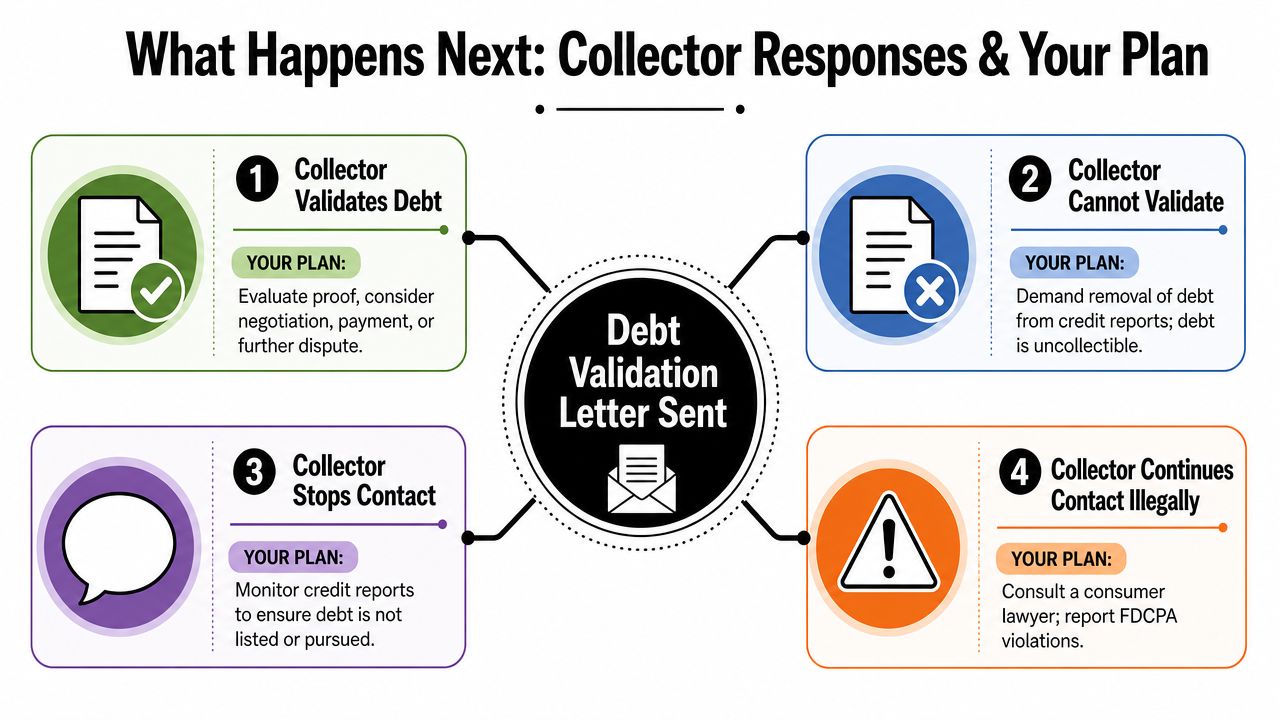

Does a free debt validation letter remove a collection from my credit report

Not by itself. A debt validation letter is sent to the collector. Credit report removal involves a separate dispute process with the credit bureaus if the reporting is inaccurate, outdated, unverifiable, or misleading.

Should I send a debt validation letter before paying a collection

In many cases, yes, especially if you don't recognize the debt, the amount seems wrong, or the account appears old. It's usually better to understand what's being collected before you agree to payment or negotiation.

What should I ask for in a debt validation letter

A practical request often includes the original creditor, amount owed, account number or reference number, supporting account details, date of last payment, and information that helps you evaluate whether the debt is still enforceable.

Can a debt validation letter help with mortgage preparation

It can. For mortgage credit repair and lender readiness, it helps you verify whether a collection account is accurate before deciding how to address it. That can make the next steps more organized for underwriting preparation.

What if the collector responds but the credit report still shows the account incorrectly

That usually means you may need a separate credit bureau dispute. Validation and credit reporting are related, but they are not the same legal workflow.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation through Superior Credit Repair to better understand your options.