HRRG most commonly stands for Healthcare Revenue Recovery Group, a medical debt collection agency. If you're seeing HRRG on your credit report, it usually means an unpaid healthcare-related bill was placed with a collection company, not that a hospital or doctor's office is reporting under a strange acronym.

That can feel unsettling, especially if you're checking your credit while getting ready to buy a home, finance a car, or clean up your reports after a lender asked questions. A collection account often looks more alarming than it is. The key is to slow down, identify what the entry means, and respond in a documented, organized way.

Many people first search what is HRRG because they don't recognize the name at all. That's normal. Collection agencies often appear on reports without much context, and medical billing can be especially confusing because a single visit may involve multiple providers, statements, and handoffs.

A calm review matters most when mortgage plans are involved. A collection account can affect how a lender views your file, even when the balance seems small or the account information looks incomplete. If you handle it correctly, you give yourself a better chance to protect your credit profile and move forward with clear next steps.

Table of Contents

- What Is This "HRRG" Entry on My Credit Report?

- Decoding HRRG Healthcare Revenue Recovery Group

- How an HRRG Collection Impacts Your Credit and Mortgage Goals

- Understanding Your Rights When Dealing with Debt Collectors

- A Step-by-Step Plan for Responding to HRRG

- When to Partner with a Credit Repair Professional

- Frequently Asked Questions About HRRG and Medical Collections

What Is This "HRRG" Entry on My Credit Report?

When people pull a credit report before applying for financing, they expect to see familiar lenders. They don't expect a short acronym that looks like an error code. If HRRG appears, the most practical reading is that a medical debt collection account has entered the picture.

In plain English, this usually means a healthcare bill was not resolved with the original provider and was later placed with a third-party collector. That third party is often easier to spot on the credit report than the original bill itself, which is why the entry feels abrupt.

A common point of confusion is this. HRRG is not a credit repair company. It's generally connected to collection activity on healthcare accounts. That matters because your response should focus on verification, report accuracy, and documentation, not on assuming the debt is automatically valid just because it appears on a report.

If you're also searching for help with broader report cleanup, it can help to understand how collection items fit into an overall credit repair and score review process. A collection entry is only one part of the file. Mortgage lenders also look at payment history, utilization, account stability, and whether negative items are accurate and properly reported.

Practical rule: Don't treat an unfamiliar collection name as proof that you owe it. Treat it as a signal to investigate.

Three questions usually matter first:

- Who is HRRG collecting for? The original source is often a hospital, physician group, emergency provider, or another healthcare-related creditor.

- Is the account accurate? Names, balances, dates, and ownership details need to match your records.

- What does this mean for financing? If you're preparing for a mortgage, even one collection account can trigger added lender review.

The good news is that confusion is fixable. Once you know what HRRG likely represents, the next step is to separate the company itself from the debt details tied to your file.

Decoding HRRG Healthcare Revenue Recovery Group

What HRRG does

Healthcare Revenue Recovery Group is a real debt collection company in the United States. According to Healthcare Revenue Recovery Group, BBB records show the business was started and incorporated on December 21, 2004, with a BBB file opened on January 22, 1996, and the company identifies itself as a licensed collection agency with Tennessee license number 602493115.

Those details matter because they help answer a basic fear many consumers have. This is not some anonymous name that appeared from nowhere. It's an established collections operation connected to the healthcare billing world.

The company's role is usually straightforward. A medical provider or related healthcare entity has an unpaid account. Instead of continuing to pursue the balance internally, that account is sent to or managed by a collections firm. The collector then contacts the consumer and may also report the account through the credit reporting system.

That's why the credit report name often doesn't match the doctor's office you remember. The provider and the collector are different parties.

Why the company details matter

Knowing HRRG is a licensed, established collection agency helps you respond professionally. It tells you there's a structured business process behind the account, and structured processes usually leave records. That is useful if you need to request verification, compare dates, or challenge incomplete reporting.

It also helps to understand the healthcare side of the equation. Medical providers often focus on getting paid for services already delivered, and many practices outsource that work as part of maximizing medical practice cash flow. From the provider's perspective, that's revenue recovery. From the consumer's perspective, it's a collections issue that needs careful review.

Here's the practical distinction:

| Party | Role |

|---|---|

| Original healthcare provider | Provided treatment or services |

| HRRG | Attempts to collect the unpaid account |

| Credit bureaus | Display reported account information if furnished |

That distinction helps with disputes. If you ask for validation, you're not asking HRRG to repeat a balance. You're asking for enough documentation to show what the account is, where it came from, and why it belongs to you.

A collector's presence on your report doesn't erase your right to ask for proof.

For many readers, this is the point where the issue becomes less mysterious. HRRG is not a random code. It's the name of a healthcare collections company. The more important question becomes what that entry means for your borrowing plans, especially if you're trying to become mortgage-ready.

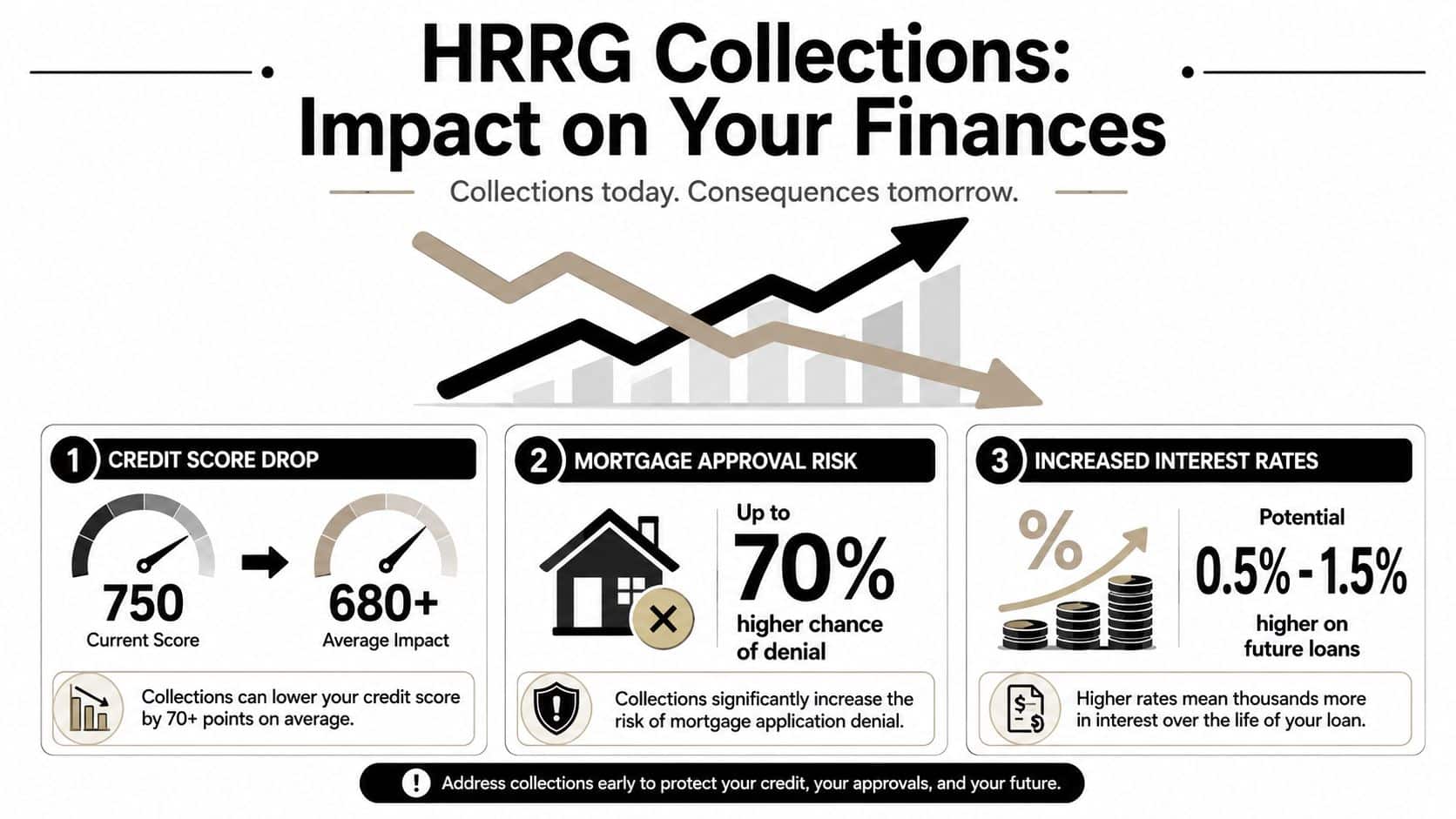

How an HRRG Collection Impacts Your Credit and Mortgage Goals

A collection account can affect more than your score. It can shape how a lender interprets your entire file. That's especially true when you're preparing for a mortgage and the underwriter is reviewing not only what appears on the report, but also whether any unresolved collection suggests ongoing risk.

Why mortgage lenders care about collections

Mortgage underwriting is more conservative than everyday consumer lending. A credit card issuer may approve based on a broad score range and current income. A mortgage lender usually looks deeper. They often review collections in the context of payment reliability, disputed debts, monthly obligations, and file stability.

An HRRG account can create problems in several ways:

- Credit profile concerns. A collection suggests a past obligation wasn't resolved as expected.

- Underwriter questions. Lenders may ask whether the debt is valid, paid, disputed, or still open.

- Documentation delays. If the file goes into manual review, closing can slow down while paperwork is gathered.

- Debt-to-income pressure. Depending on the loan file and lender standards, unresolved obligations may complicate affordability analysis.

This is one reason many homebuyers look for help understanding FICO-focused credit repair factors before mortgage review. A mortgage file is rarely judged by one item alone. The issue is how that item interacts with the rest of the report.

What this can mean for home loan timing

Not every HRRG collection leads to denial, and not every lender treats collections the same way. Still, the presence of a medical collection can change the conversation. A lender may ask for explanation letters, proof of payment, evidence of dispute, or confirmation that the account information is inaccurate and under review.

If you're aiming for FHA, VA, USDA, or conventional financing, the practical takeaway is this: an unresolved collection can become a mortgage-readiness issue even before it becomes a legal issue.

Consider two borrowers with similar income:

- One has clean reports, low utilization, and no open collection disputes.

- The other has an HRRG collection with unclear creditor details and no written records.

The second borrower may spend more time answering lender questions, even if the debt later turns out to be inaccurate or incomplete.

Mortgage underwriting is often about confidence. Clean documentation gives lenders confidence. Unclear collections take confidence away.

That doesn't mean you should rush to pay first and ask questions later. It means you should move quickly to verify the account, organize records, and decide on the best response before you're deep into a purchase contract or rate lock window.

For first-time homebuyers, this is often the hidden problem. They think they only need a better score. In reality, they also need a file that looks explainable, documented, and stable.

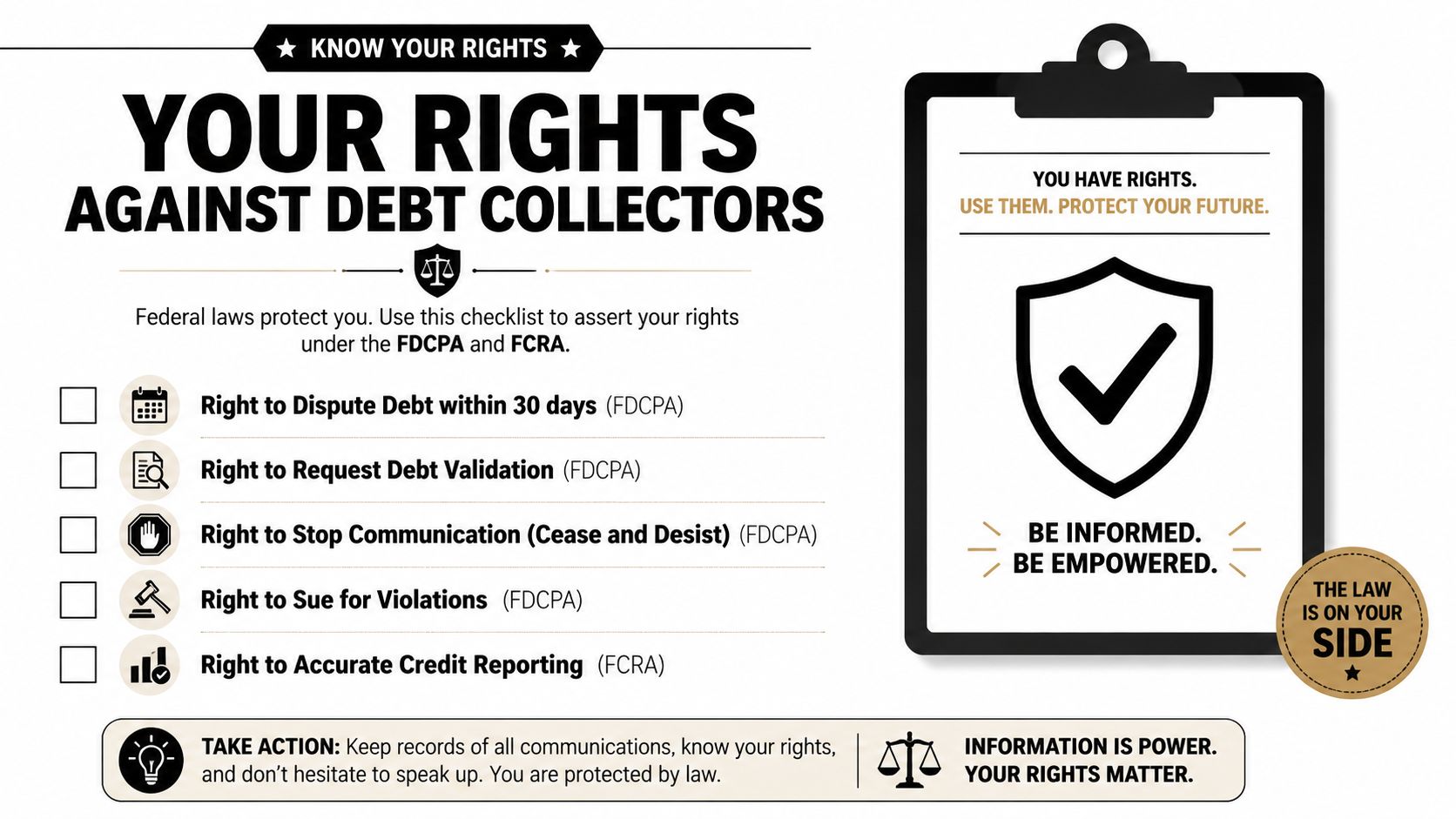

Understanding Your Rights When Dealing with Debt Collectors

When a collection company contacts you, the most important shift is mental. You don't have to argue, panic, or guess. You need a paper trail. Consumer protection rules give you a framework for that.

What debt validation really means

The core issue in many collection disputes is whether the collector can show enough detail to support the account. Consumer guidance discussed in this video on debt validation and credit reporting strategy emphasizes that the key technical question is whether HRRG can substantiate the debt with original creditor details, dates of activity, and a complete balance history. That's why written verification matters when information is incomplete, inaccurate, or not properly supported under frameworks such as the FCRA and FDCPA.

That idea sounds technical, but the day-to-day meaning is simple. If a collector says you owe a debt, you can ask them to show the basis for that claim in writing.

A useful way to think about validation is to compare it with a receipt trail. You're looking for enough information to answer questions like:

- Where did this debt start?

- Who was the original creditor?

- What service or account created the balance?

- Do the dates line up with your records or insurance activity?

- Does the amount make sense from start to finish?

If the file lacks those basics, the account may still be reported, but it may also be vulnerable to challenge.

Why written records matter

Phone calls create pressure. Letters create evidence. If your goal is to dispute negative accounts, rebuild your credit profile, or prepare for a home loan, written communication is much more useful than verbal back-and-forth.

That's also why people dealing with larger disputes sometimes research court procedure in their area. If a collection matter ever escalates, a practical consumer resource like this guide to OC small claims can help you understand how documentation and organized evidence matter in legal settings too.

Keep your records in one place:

- Collection letters from HRRG

- Credit report copies showing the account

- Medical billing statements or provider notices

- Insurance EOBs

- Certified mail receipts if you send disputes or validation requests

- A call log with dates, times, and names

If you need a broader understanding of compliant dispute help, this overview of free credit repair help without the hype explains why documentation-based processes matter more than promises.

Key point: Your strongest position usually comes from written proof, not from a long phone call.

Consumers often feel powerless because debt collection sounds legal and urgent. In reality, your advantage starts with accuracy. If the information is wrong, incomplete, outdated, or unsupported, that matters.

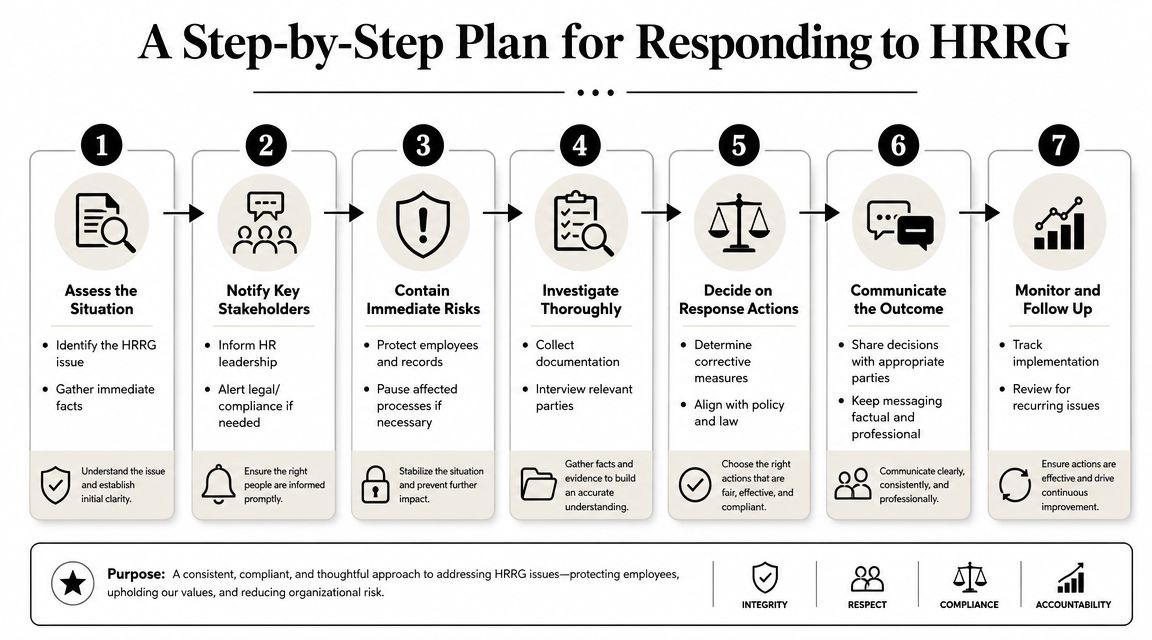

A Step-by-Step Plan for Responding to HRRG

The best response to HRRG is organized, not emotional. You're trying to determine whether the account is valid, whether the reporting is accurate, and what action makes sense for your credit and financing timeline.

Start with verification, not panic

If you receive a notice or see HRRG on your report, don't ignore it. But don't assume immediate payment is the first move either. First, gather your own records.

Look for any provider statements, insurance correspondence, old payment receipts, or explanation of benefits forms. If medical billing language is confusing, this how to read explanation of benefits guide can help you compare insurer paperwork with what a collector is trying to recover.

Then take these opening steps:

- Pull your credit reports and confirm exactly how the account is listed.

- Check identifying details such as the account name, dates, and balance information.

- Compare the entry to your own medical records and insurance paperwork.

- Send a written debt validation request if the account is unfamiliar, unclear, or questionable.

A lot of people lose ground here because they rely on memory. Medical accounts often involve rushed visits, multiple providers, and insurance adjustments. Documentation beats memory every time.

Review the response carefully

Once you request validation, slow down and examine what comes back. You're looking for substance, not just a restated claim.

Use this checklist:

| Review item | What to look for |

|---|---|

| Original creditor | A clear healthcare provider or billing entity |

| Dates of activity | Dates that match treatment or account history |

| Balance trail | Enough detail to understand how the amount was calculated |

| Personal identifiers | Information tying the account to you accurately |

| Completeness | Records that do more than repeat a number |

If the response is thin, inconsistent, or missing critical facts, that may support a dispute. If the documentation is clear and consistent, then you can evaluate whether resolving the account makes sense based on your goals.

For readers trying to clean up multiple report issues at once, a broader credit repair service overview can help frame how collections, late payments, balances, and account stability all interact.

Don't ask only, “Do I remember this?” Ask, “Can this account be documented clearly and reported accurately?”

Choose the next move based on evidence

Once you've reviewed the information, your next step usually falls into one of three lanes.

- If the account appears inaccurate. Dispute the reporting with the credit bureaus and keep copies of all supporting records.

- If the account is yours but details are incomplete. Continue pressing for proper documentation and monitor how the account is reported.

- If the account is valid and mortgage timing matters. Consider discussing payment or settlement options, but get terms in writing and think through how that resolution fits your lender's requirements.

This is also where timing matters. If you plan to apply for a mortgage soon, don't make random changes to your credit file without understanding how an underwriter may read them. A quick payment can feel productive, but documentation still matters if the lender later asks what the account was and how it was resolved.

A strong response plan is usually calm and repeatable:

- keep everything in writing

- verify before admitting

- dispute what can't be supported

- resolve valid issues strategically

- save every document for future lender review

That approach won't guarantee a specific outcome, but it does put you in a better position than reacting under pressure.

When to Partner with a Credit Repair Professional

Some HRRG issues are manageable on your own. Others become messy fast. That's especially true if you're facing a mortgage deadline, juggling several negative accounts, or trying to tell the difference between a valid collection and an account that's being reported poorly.

Professional help often makes sense when the situation includes one or more of these factors:

- Mortgage preparation when a lender has already flagged collections, disputed accounts, or report inconsistencies.

- Multiple problem items such as charge-offs, late payments, and medical collections appearing across different bureaus.

- Poor documentation when the collector's response doesn't clearly establish the original account history.

- Limited time if work, family obligations, or stress make it hard to manage letters, follow-ups, and bureau disputes carefully.

A good credit repair process isn't about shortcuts. It's about review, documentation, and compliant dispute work. That's why people often compare providers and costs before deciding whether outside help makes sense. If you're weighing that decision, this page on what people really pay for credit repair in Alabama gives useful context on how consumers think about cost and value.

The right time to get help is usually before confusion turns into delay. That's particularly true for homebuyers who need a lender-ready credit profile, not just a better-looking report. Results always vary based on the credit file, account history, documentation, and how creditors or collectors respond.

Frequently Asked Questions About HRRG and Medical Collections

Can HRRG stay on my credit report if I don't recognize the debt?

Yes, it can still appear while you investigate it. But appearance alone doesn't settle the question of accuracy. If you don't recognize the account, ask for written validation and compare the reported details to your records.

If the account information is inaccurate, incomplete, outdated, or unverifiable, that can support a dispute. The stronger your documentation, the clearer your position.

Should I pay HRRG right away if I'm trying to buy a house?

Not automatically. A mortgage goal creates urgency, but urgency isn't the same as strategy. First confirm whether the debt is valid and how your lender wants collections handled in your specific loan scenario.

Some buyers hurt their own file by acting before they understand the reporting, the lender's conditions, or whether the account is even being described correctly. A cleaner mortgage path usually starts with verified facts.

Can I ask HRRG for a pay-for-delete?

You can ask, but you shouldn't assume it will happen. Collection outcomes vary, and no one should promise deletion in exchange for payment as a guaranteed result.

If you discuss payment, get all terms in writing before sending money. Keep copies for your records in case a lender later asks how the account was resolved.

How do I contact HRRG if I need account access?

Public-facing information described by SoloSuit's HRRG overview shows that HRRG offers 24-hour online account access, lists office hours as Monday through Friday from 8:30 a.m. to 10:00 p.m. Eastern Time, and provides contact channels including 800-984-9115 and a payment mailing address at P.O. Box 5406, Cincinnati, OH 45273. Those details suggest an established, multi-channel collections operation rather than a small local office.

That said, using a phone number or portal doesn't replace your need for written records. If the issue affects your credit report, keep your own copies of everything.

What if the account information looks incomplete or wrong?

That's one of the most important red flags to take seriously. An account may deserve review if the original creditor is unclear, the dates don't line up, the balance history is hard to follow, or the identifying information doesn't match your records.

When that happens, stick with documented communication. Ask for verification, save all responses, and dispute inaccurate reporting through the proper channels if the information can't be supported.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. If you're dealing with HRRG, medical collections, late payments, or other issues affecting mortgage readiness, you can request a free credit analysis or consultation through Superior Credit Repair to better understand your options.