You pull your credit reports because you're finally getting serious about buying a home. Then you see a name you don't recognize: NCB Management Services. For many people, that's the moment the stress starts. Is it a lender? A scam? A sign that mortgage approval is now out of reach?

Take a breath. In most cases, the right response starts with understanding what you're looking at and documenting everything carefully. A collection account doesn't automatically end your homebuying plans, but it does mean you need to slow down, verify the details, and make decisions based on records instead of pressure.

This guide addresses the question: what is NCB Management Services, and will walk you through it in plain English. You'll learn what the company does, how a collection account can affect mortgage readiness, what your rights are, and what steps to take if NCB contacts you or appears on your credit report.

Table of Contents

- Understanding NCB Management Services

- How a Collection Account Can Affect Your Mortgage Application

- Know Your Rights The Fair Debt Collection Practices Act

- A Step-by-Step Guide to Responding to NCB

- Sample Debt Validation Letter Template

- Strategies for Resolving a Validated Collection

- When to Seek Professional Credit Repair Help

- Frequently Asked Questions About NCB Management Services

Understanding NCB Management Services

NCB Management Services, Inc. is a U.S.-based debt collection and accounts receivable management company founded in 1994 and headquartered in Trevose, Pennsylvania, according to NCB's company information. The same company description says it operates as a national debt buyer, which means it may acquire delinquent accounts from original creditors rather than lend money directly.

What NCB Management Services does

In plain language, NCB is generally involved after an account has already gone wrong. A person may have fallen behind on a bill, the original creditor may have assigned the account for collection, or the debt may have been sold. At that point, a company like NCB enters the picture.

That distinction matters. If you see NCB on your credit report or get a letter from them, you're usually not dealing with the company that originally gave you the credit or service. You're dealing with a collector or debt buyer that is trying to recover on a delinquent account.

NCB's stated business areas include debt tied to healthcare, financial services, and telecommunications. Those categories come up often in consumer credit problems, and they can overlap with other collection agencies such as healthcare revenue recovery group when unpaid accounts move through the recovery system.

Why consumers usually see NCB's name

Consumers don't know who NCB is until they receive a letter, a call, or notice a collection tradeline on a credit report. That surprise creates confusion because the name on the collection item may not match the hospital, lender, card issuer, or phone provider the consumer remembers.

Practical rule: Don't assume a collection is valid just because the name appears on your credit report. Start by matching the account to your own records.

A useful way to think about NCB is this:

| Term | Plain-English meaning |

|---|---|

| Original creditor | The company that first issued the account or bill |

| Debt collector | A company trying to collect on an unpaid account |

| Debt buyer | A company that may purchase delinquent debt and then collect on it |

Once you understand that role, the next question becomes more important than the name itself. How does a collection account affect your ability to buy a home?

How a Collection Account Can Affect Your Mortgage Application

A collection account can disrupt a mortgage file even when the original bill seems minor. Legal-help materials discussing NCB note that a collection entry, especially one tied to medical, telecom, or financial-service debt, can complicate underwriting and delay approval for FHA, VA, USDA, and conventional mortgage applications, as described in this NCB overview.

Why mortgage lenders pay attention to collections

Mortgage underwriting is built around risk, consistency, and documentation. A collection account can raise several questions for a lender at once. Is the debt accurate? Is it resolved? Could new collection activity appear again before closing? Does the file show a pattern of missed obligations?

Even when a borrower has enough income for the payment, collections can still slow things down because underwriters often want a clean explanation and supporting paperwork. If the account is disputed, paid, settled, or still open, each status can lead to different follow-up requests from the lender.

This is why homebuyers often feel blindsided. They aren't just dealing with credit score concerns. They're dealing with file stability.

What this means for FHA VA USDA and conventional loans

Each loan type has its own underwriting approach, but all of them care about whether the credit profile looks reliable. An unresolved collection can trigger added review, requests for letters of explanation, proof of payment, proof of settlement, or updated credit documentation before the loan moves forward.

Here are the practical issues collections often create during mortgage prep:

- Timing problems: A lender may pause progress while you gather records.

- Documentation gaps: If ownership of the debt changed hands, you may need a clearer paper trail.

- Underwriter concern: Recent or active collection activity can suggest unresolved financial stress.

- Closing delays: Even a manageable issue can hold up final approval if it appears late in the process.

Mortgage underwriting isn't only about what you owe. It's about whether the documents tell a consistent story.

If you've ever wondered why a small collection creates such a large headache, that's the reason. The issue isn't always the balance itself. It's the uncertainty around the account.

For readers comparing systems in different countries, Demystifying French mortgage eligibility for foreigners offers a useful outside view of how underwriting standards can vary while still focusing on documentation, repayment history, and lender confidence.

A good mortgage-readiness approach starts early. Review your reports before you apply, identify any collection tradelines, and avoid making rushed payments without understanding how the account is being reported and what the lender will want to see afterward.

Know Your Rights The Fair Debt Collection Practices Act

When a collector contacts you, the law matters. You are not required to guess your way through the process. NCB's FAQ states that it accepts written or oral requests to stop calls at a workplace, and its public materials also direct consumers to submit account-specific disputes and requests in writing. Those practical rules fit into the broader framework of consumer protections explained through CFPB and FTC credit regulations.

Rights that matter in everyday collection situations

The Fair Debt Collection Practices Act, often called the FDCPA, sets rules for how many third-party collectors may communicate with consumers. You don't need to memorize the statute to use it well. You just need to know what to document and when to speak up.

These are the rights consumers most often need in real life:

- Right to request validation: If a collector contacts you about a debt, you can ask for information that helps confirm what the debt is and why the collector says you owe it.

- Right to limit workplace calls: If you tell a collector not to call you at work, that request matters.

- Right to demand communication stop: Consumers can send a written cease-communication request.

- Right to be free from harassment: Repeated abusive behavior, threatening language, or deceptive pressure isn't part of lawful collection practice.

What to do if communication crosses the line

The smartest response is usually a calm one. Keep screenshots, save voicemails, log dates, and keep copies of every letter. If a phone call turns heated, end it and move the conversation back to writing.

A short contact log can help:

| What to track | Why it matters |

|---|---|

| Date and time | Helps establish a timeline |

| Phone number or letter source | Identifies who contacted you |

| Summary of what was said | Preserves details while fresh |

| Your response | Shows that you asserted your rights |

Keep this standard: If it isn't in writing, treat it as incomplete.

Many consumers feel powerless when a collection account appears. In reality, documentation gives you an advantage. The law doesn't erase debt automatically, but it does require a process, and that process works better when you create a clear record from the start.

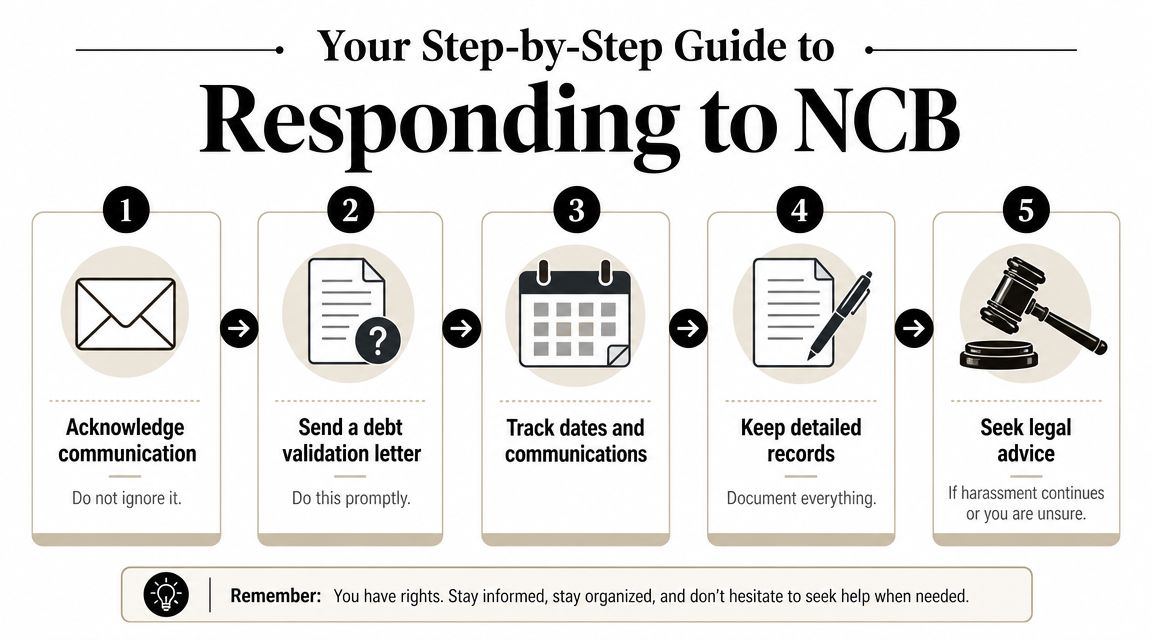

A Step-by-Step Guide to Responding to NCB

If NCB contacts you or appears on your report, don't ignore it. But don't rush into payment either. Start with verification, organization, and written communication.

Your first moves after contact

NCB states that account-specific disputes, document requests, and cease-communication requests must be submitted in non-electronic writing to its Trevose, Pennsylvania address, according to the company site. That detail is important because it tells you exactly how to handle serious account issues.

Use this sequence:

Pause before acting

Read the letter or review the credit entry carefully. Look for the account number, creditor name, and any dates listed.Request validation in writing

If you don't recognize the account, or if the details look incomplete, send a debt validation letter promptly.Avoid verbal promises

Don't agree on the phone that the debt is yours if you haven't reviewed the documentation.Pull your credit reports

Compare what NCB is reporting against the entries on your files and your own billing records.

How to build a clean paper trail

Many consumers make mistakes. They call, talk through the issue, and assume the problem is being handled. Later, they have no record of what was said.

A safer process looks like this:

- Send certified mail: It creates proof that your request was mailed and delivered.

- Keep copies of everything: Save your letter, envelope, mailing receipt, and any response.

- Create one folder for the account: Include credit report screenshots, billing records, notes, and all correspondence.

- Track deadlines and follow-ups: Write down when you sent the request and when a reply arrives.

If you're sending sensitive records like statements, identity documents, or account correspondence, this guide on securely sending documents for businesses can help you think through safer delivery methods and record retention.

A collection dispute is easier to manage when your file is better organized than the collector's.

If the account later becomes part of mortgage underwriting, your paper trail can also help explain the issue to a lender. Clear records don't guarantee a specific outcome, but they often reduce confusion and last-minute scrambling.

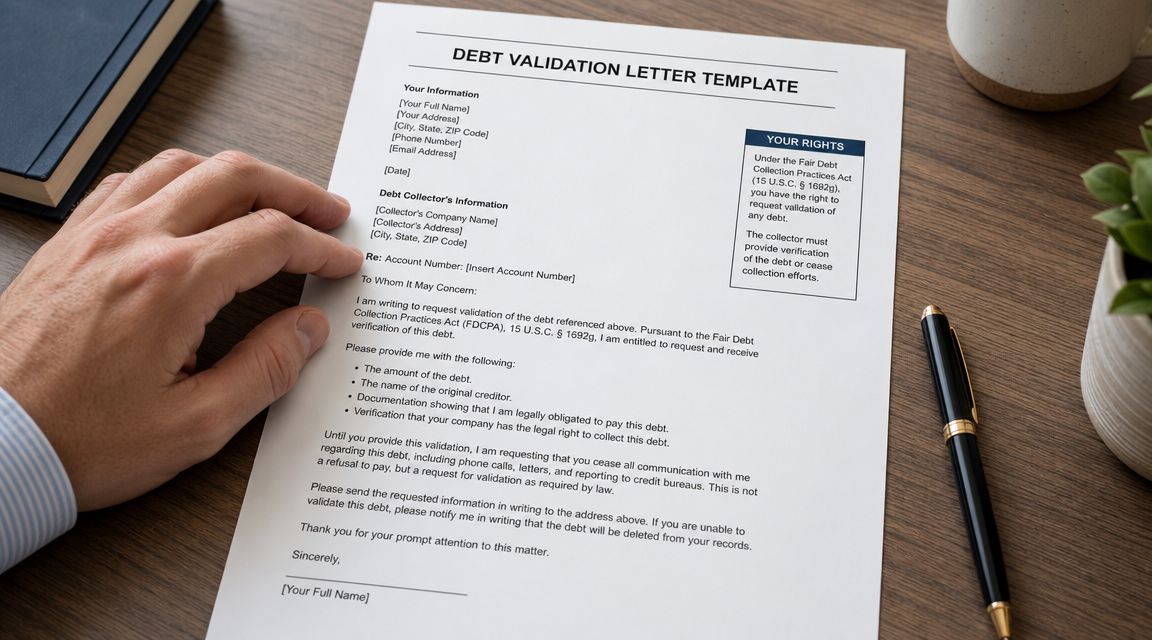

Sample Debt Validation Letter Template

Most consumers feel more confident once they have words on the page. A debt validation request doesn't have to be fancy. It just needs to be clear, respectful, and specific enough to show that you're asking for documentation.

How to use this template

Before mailing the letter, fill in your name, current address, the date, and any account reference number shown on the letter or credit report. Keep your wording simple. You're not trying to argue every detail yet. You're asking for records.

Mail it in a way that creates delivery proof. Then save a copy for your file.

If you'd like more examples of how to dispute collection letters effectively, it helps to compare formats and keep your language consistent.

Copy and paste template

[Your Full Name][Your Address][City, State ZIP][Date]NCB Management Services, Inc.

[Use the mailing address listed on your notice or current company correspondence]Re: Account Number [Insert Account Number]

To Whom It May Concern,

I am writing regarding the account referenced above. I am requesting validation of this debt and documentation sufficient to identify the original creditor, the amount claimed, and the basis for your claim that I am responsible for this account.

Please provide any records you rely on to support the account, including account identification details and any information showing transfer or assignment if the debt was obtained from another party.

If this account is being reported to any consumer reporting agency, please ensure that the information reported is complete and accurate. If you determine that the account information is inaccurate, outdated, unverifiable, or otherwise should not be reported as presently stated, please correct or update your reporting as appropriate.

I request that future communication about this matter be in writing.

Sincerely,

[Your Signature][Your Printed Name]

That letter doesn't admit the debt is yours. It asks the company to support what it's claiming with documents.

Strategies for Resolving a Validated Collection

If the account comes back validated and the records appear accurate, the issue shifts from verification to resolution. At that point, your goal is to choose a path that fits your budget, your timeline, and your financing plans.

Common resolution paths

There are several ways people handle a valid collection:

| Option | What it means | Main consideration |

|---|---|---|

| Pay in full | You satisfy the claimed balance | May help clean up lender questions, but you still want written proof |

| Settle for less | You negotiate a reduced payoff | Get the terms in writing before paying |

| Request deletion | You ask whether the collector will remove the tradeline after payment | This isn't always granted |

| Leave it unresolved temporarily | You delay action while reviewing mortgage timing and budget | Can create underwriting issues later |

For homebuyers, the key question isn't just, "Can I pay this?" It's also, "How will my lender view this account once I do?" Some lenders care most about whether the collection is resolved and documented. Others may still want explanation letters or updated reports after payment or settlement.

Resolve the account in writing, and keep the final proof where you can find it quickly.

Special caution with newer debt types

A growing problem involves newer obligations that don't have the same clear paper trail as older credit card or loan accounts. Legal-help materials discussing NCB note that Buy Now, Pay Later debt can create confusion around credit reporting and disputes because the documentation trail may be less clear than with traditional credit cards, as described in this overview of NCB collection issues.

That matters because consumers may not immediately recognize the debt source. A missed installment from a fintech product, app-based lender, or pay-in-four plan may later appear under a collector's name with limited context.

If you're dealing with a difficult file, multiple collection accounts, or unclear ownership records, some consumers look for expert collection removal services to help review documentation and dispute any reporting that appears inaccurate, outdated, unverifiable, or misleading. Results vary, and the outcome depends on the account history, records available, and how creditors or bureaus respond.

When to Seek Professional Credit Repair Help

Some collection issues are straightforward. Others become complicated fast. If you're preparing for a mortgage, juggling multiple negative accounts, or trying to decode records that don't match, outside help can save time and reduce mistakes.

Situations where outside help makes sense

Professional help may be worth considering when:

- You have several collections at once: It's harder to keep timelines, letters, and account histories organized.

- A mortgage application is approaching: Mortgage credit repair often depends on fixing reporting issues before underwriting starts.

- The account records look inconsistent: Names, balances, dates, or ownership details may not line up.

- You need a file review, not just a dispute letter: Sometimes the bigger issue is overall lender readiness.

This is also where cost questions come up. If you're comparing service models, local pricing discussions like Alabama credit repair costs can help you understand how consumers evaluate fees and structure.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation to better understand your options. As with any credit repair or credit restoration process, results vary based on your records, creditor responses, reporting history, and current credit behavior.

Frequently Asked Questions About NCB Management Services

Is NCB Management Services a lender

No. NCB describes itself as a debt buyer and accounts receivable management company, not an original lender.

Does NCB always report collection accounts to the credit bureaus

NCB's FAQ states that it does not credit report accounts placed for collection by third-party creditors that are non-purchased accounts. That doesn't mean the underlying debt can't affect your file in other ways.

Should I call NCB or write to them

For account-specific disputes, document requests, and cease-communication requests, written communication is usually the safer route because it creates a record.

Can a collection stop me from getting a mortgage

It can complicate underwriting and delay approval, especially if the account is unresolved or poorly documented.

What if I don't recognize the debt

Request validation and compare any response to your credit reports, statements, and personal records before taking further action.

| FAQs | Quick answer | Why it matters |

|---|---|---|

| What is NCB Management Services | A debt collector and debt buyer | Helps you understand why their name appears after default |

| Should I pay immediately | Usually not before reviewing records | Prevents rushed mistakes |

| Do I need documentation | Yes | It protects your rights and helps with lenders |

| Can I dispute the account | Yes, if details are inaccurate or unclear | Disputes should be based on records |

If you're dealing with a collection account and trying to prepare for a mortgage, auto loan, apartment approval, or general credit rebuilding, Superior Credit Repair offers educational, compliance-focused help. The process centers on reviewing your reports, identifying inaccurate, outdated, unverifiable, or misleading items, and building a practical strategy for stronger long-term credit habits. Results vary, and any dispute or credit repair outcome depends on documentation, account history, bureau responses, and your current credit behavior.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile.