You may be closer to buying a home than you think, and still not be ready.

A lot of first-time buyers do the hard parts right. They save for closing costs, pay down debt, and keep their spending under control. Then the lender pulls credit and says the file is too thin. That catches people off guard because the score on the screen doesn't look terrible. But mortgage lending doesn't run on hope or headlines. It runs on documentation, account history, and patterns an underwriter can trust.

That's where tradelines come in. Adding tradelines to credit can help when it's done the right way, for the right reason, and early enough in the mortgage preparation process. It can also backfire if you treat it like a shortcut.

Table of Contents

- Why a Good Score Is Not Enough for Mortgage Approval

- Understanding the Three Paths to Adding Tradelines

- The Risks and Rewards What Mortgage Lenders Really See

- How to Ethically Add an Authorized User Tradeline

- Building a Lender-Ready Profile Beyond One Tradeline

- How Superior Credit Repair Guides Your Next Steps

- Frequently Asked Questions About Adding Tradelines

Why a Good Score Is Not Enough for Mortgage Approval

The couple who thought they were ready

A couple comes in after getting serious about buying their first home. They've been renting, working steadily, and trying to do things the responsible way. Their score looks decent enough to them. Then the mortgage lender reviews the file and says the problem isn't only the score. The problem is the history behind it.

That happens more often than people expect. A lender wants to see more than a number. They want to see that you've managed credit over time in a way that looks stable, predictable, and real. If your report has very few accounts, very recent accounts, or big gaps in activity, the file can look weak even when the score looks acceptable.

Point Predictive notes that adding tradelines to a credit profile is an important way to address thin-file risk, and that establishing 2–3 legitimate tradelines with low utilization and on-time payments is a compliant way to improve file stability for FHA and VA readiness, as explained in this review of how fake tradelines affect lending.

Practical rule: Mortgage lenders don't approve a score. They approve a borrower file.

If you want to understand the broader approval standard, start with how lenders approve home loans. It puts the score in context, which is where most buyers get tripped up.

What a tradeline actually is

In plain English, a tradeline is one account on your credit report. A credit card is a tradeline. An auto loan is a tradeline. A student loan is a tradeline. Each one tells a lender something about how you borrow and repay.

When people talk about adding tradelines to credit, they usually mean one of two things. They either mean adding a legitimate account relationship that reports to the bureaus, or they mean trying to force a quick score increase by getting attached to someone else's account. Those are not the same strategy.

Used correctly, tradelines can help a first-time homebuyer build a fuller report. Used recklessly, they can make the file look manipulated. That difference matters most at underwriting, not during the initial online prequalification screen.

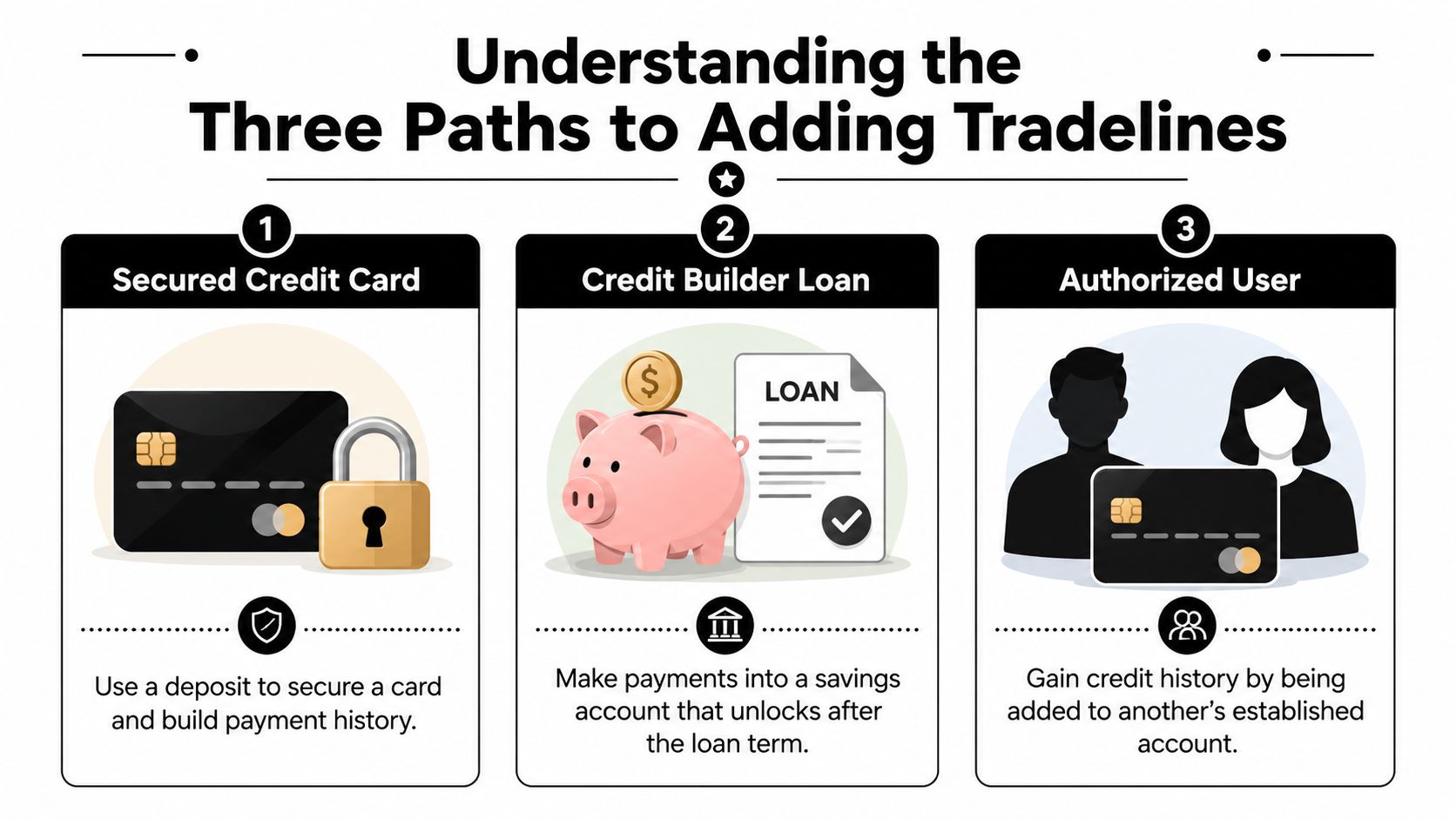

Understanding the Three Paths to Adding Tradelines

A lot of online advice lumps every tradeline tactic into one bucket. That's sloppy. Mortgage lenders don't view these paths the same way, and you shouldn't either.

Experian explains that a tradeline is a specific credit account on your report, and that this account data is what scoring models use. It also notes that open accounts remain indefinitely and closed accounts in good standing typically remain for 10 years, which is why account stability matters so much when you're adding tradelines to credit.

Path one authorized user status

This is the most common personal credit strategy. A parent, spouse, or trusted family member adds you as an authorized user to an existing credit card account. If the issuer reports authorized users, that account may appear on your report.

This path can help if the account is old, well-managed, and carries a low balance relative to the limit. It can hurt if the account has late payments, high utilization, or unstable balances.

Best fit:

- Thin files: People with very little revolving credit history

- Family-supported rebuilding: Buyers who have a trusted relative with a clean, established account

- Early mortgage prep: Borrowers planning ahead, not scrambling before underwriting

Path two joint accounts you actually share

A true joint account is different. Both parties are responsible for the debt. This isn't a reporting trick. It's a real credit obligation.

For a married couple or long-term partners managing finances together, a joint account can make sense. For casual arrangements, it usually creates more risk than value. If one person overspends or misses payments, both reports can take the hit.

Here's the practical difference:

| Method | Control | Risk to you | How an underwriter may view it |

|---|---|---|---|

| Authorized user | Limited | You inherit reported history | Can help if it looks organic |

| Joint account | Shared | Full responsibility | Stronger if managed well |

| Purchased tradeline | Almost none | High | Often viewed with skepticism |

If you're comparing options, this guide on the benefits of tradelines for credit is useful for understanding where tradelines fit into a broader credit restoration plan.

Path three purchased seasoned tradelines

This is the path I don't recommend for homebuyers.

A “seasoned tradeline” usually means paying a company to place you as an authorized user on a stranger's old account for reporting purposes. The sales pitch is always the same. Older account, higher limit, quick boost, problem solved. Real mortgage lending doesn't work that way.

The issue isn't only whether it reports. The issue is whether it survives lender review. If the account looks rented, detached from your actual borrowing behavior, or inconsistent with your profile, it can create more problems than it solves.

A tradeline that helps a credit score but fails an underwriting review didn't help you. It delayed the real work.

The Risks and Rewards What Mortgage Lenders Really See

Mortgage underwriters are paid to find weak files. They don't stop at the score. They compare the report to the application, the bank statements, the debts, and the overall story.

What helps

A legitimate authorized user account can help when it looks natural and supports the rest of the file. A common example is an adult child added to a parent's long-standing account, with no suspicious payment arrangement and no signs that the tradeline was rented for a temporary boost.

A healthy authorized user tradeline can strengthen the overall picture when:

- The primary account is clean: No late payments, no erratic usage

- The balance is controlled: Low utilization is easier for an underwriter to accept

- The relationship makes sense: Family-based and consistent with the borrower's profile

- The rest of the file is improving too: Income, savings, and debt management all support the application

Leaders in Law notes that an authorized user tradeline can help or hurt because the account's payment history and balance are reflected on the user's report, as discussed in their explanation of how tradelines affect you.

What gets flagged

Bought tradelines are where borrowers get themselves into trouble. Consultant LM explains that commercial tradeline buying can violate the underwriter's benefit of ownership principle and that lenders have tightened scrutiny on rented tradelines from 2024–2026, which can lead to denial, as described in this discussion of tradelines and credit history.

That tightening makes sense. Underwriters now look for signs that the account history on the report doesn't match the borrower's real financial behavior. If a file suddenly shows an old, high-limit account with no practical connection to the borrower's own spending patterns, it raises questions.

Common red flags include:

- Temporary attachment: The tradeline appears shortly before mortgage shopping

- No ownership benefit: The account history doesn't match how the borrower uses credit

- Profile mismatch: The account looks inconsistent with the age or depth of the rest of the file

- Artificial appearance: High limit, low balance, no organic explanation

Point Predictive also warns that lenders scrutinize suspect tradelines and fake reporting entities because they can distort risk evaluation in ways that don't reflect real borrower behavior.

Underwriters are not looking for creative credit. They're looking for believable credit.

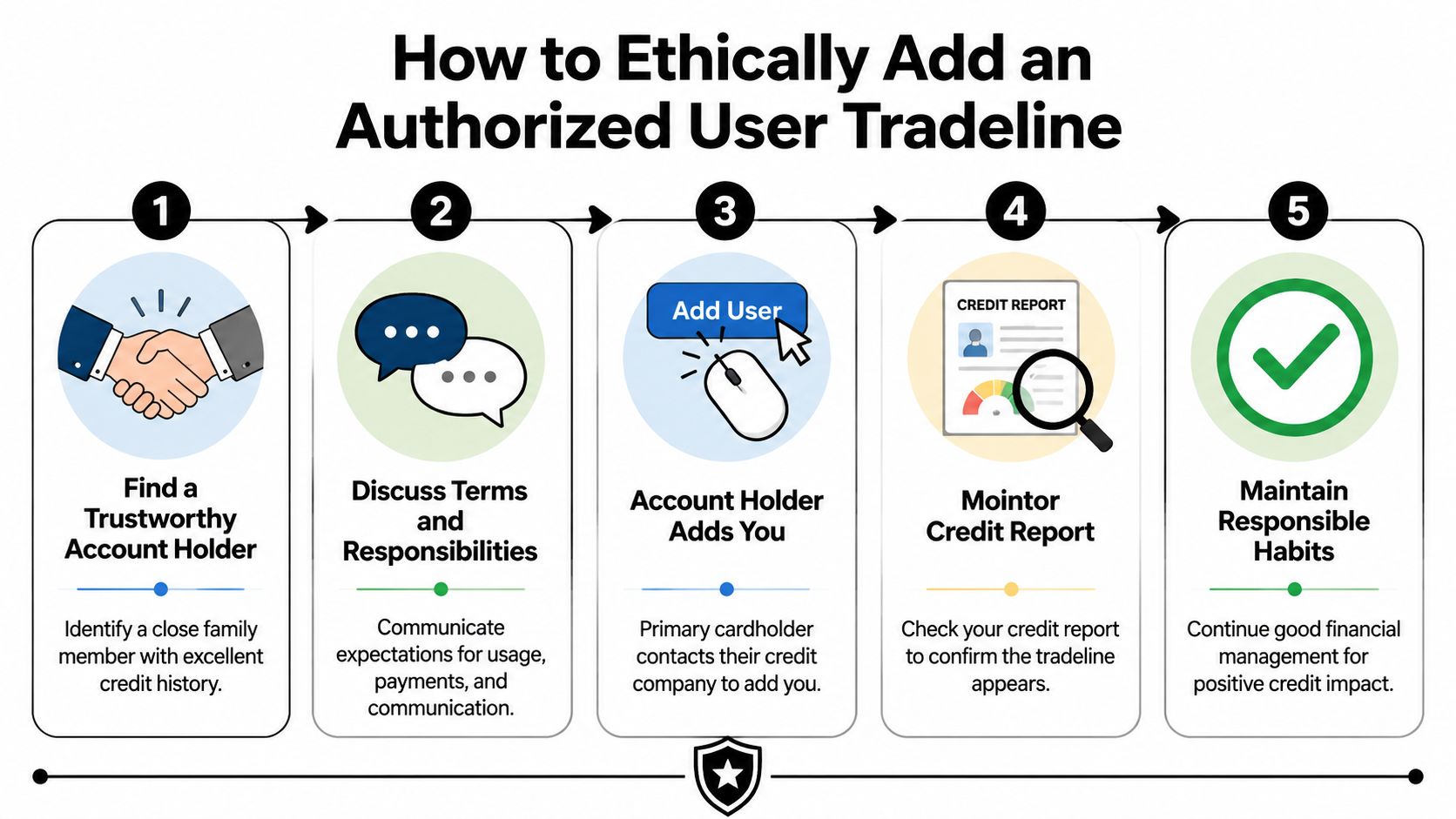

How to Ethically Add an Authorized User Tradeline

If you're going to use an authorized user tradeline, do it in a way that can survive scrutiny. This is not the place for shortcuts.

Choose the account before you choose the person

Starting by asking, “Who can add me?” is backwards. Begin with the account itself.

The YouTube source provided in the verified data explains that adding a tradeline through authorized user status works by placing the account's age, credit limit, and payment history into your file, and it adds an important warning: the user should be added for reporting purposes only, not for actual use, because spending activity can create new risks, as covered in this tradeline explanation.

Run a basic health check:

- Account age matters: Older is generally more stable than brand new

- Payment history must be clean: Don't attach yourself to sloppy management

- Utilization should stay low: A maxed-out card can do damage fast

- Reporting must be confirmed: Not every issuer handles authorized users the same way

Handle the setup like a mortgage strategy

Once the right account is identified, keep the process simple and documented. The primary account holder contacts the issuer and adds you as an authorized user. Then you wait for reporting to update. The verified data states this update is typically reflected within 30–45 days through the bureau reporting cycle in the cited source.

What I recommend:

- Use family or a trusted household relationship. That's easier to explain and easier for a lender to understand.

- Do not use the card. If the goal is reporting support, keep it that way.

- Monitor all three reports. Confirm the account appears and is reporting accurately.

- Avoid timing this too close to underwriting. Any change made late in the process can create review issues.

- Have an exit plan. If the account turns negative, you need to act quickly.

The short-term dip is real in some files. The verified data notes that adding a new tradeline can reduce average age of accounts and may cause a temporary drop before any longer-term benefit shows up. That's one reason not to experiment right before you apply for a mortgage.

If the relationship sours or the account starts reporting poorly, focus on solving authorized user credit issues. Don't leave a bad tradeline sitting on your report just because it once looked helpful.

Mortgage timing matters: A good credit move made at the wrong time can still create a lending problem.

Building a Lender-Ready Profile Beyond One Tradeline

One authorized user account is not a mortgage strategy by itself. It's one part of a credible file.

What a stable file looks like

USDA guidance in the verified data highlights a point most tradeline marketers skip. For mortgage purposes, there's a major gap between a temporary authorized-user boost and the kind of file FHA and USDA underwriting can accept. That source states an eligible tradeline must be open for a full 12 months, and that purchased tradelines often detach after 30–90 days, which can cause applicants to fail final underwriting, as explained in the USDA Rural Development credit training document.

That's why rented tradelines are such a bad fit for homebuyers. They may help you look better in the earliest stage of the process, then disappear when the lender asks for updated documentation.

A lender-ready profile usually has:

- Consistency: Accounts remain open and active long enough to matter

- Depth: More than one type of positive account history

- Clean behavior: On-time payments and controlled balances

- Real borrower participation: The file reflects your habits, not someone else's résumé

Safer ways to build depth

If your file is thin, build your own history in parallel with any legitimate authorized user help.

Good options include:

- Secured credit cards: These can help establish revolving history in your own name. If you're comparing options, review how secured cards help credit scores.

- Credit-builder loans: These can add installment history and show payment discipline.

- Eligible alternative tradelines: The verified USDA guidance notes that monthly subscription services and self-reported tradelines may be eligible if third-party verification exists.

- Disputing inaccurate accounts: A cleaner report is often more important than a temporary score bump.

Borrowers need discipline. Don't chase optics. Build substance. A mortgage underwriter wants to see a file that still makes sense after they strip away anything temporary, questionable, or unsupported.

How Superior Credit Repair Guides Your Next Steps

A lot of borrowers don't need a gimmick. They need a full review of the report, a reality check on what lenders will question, and a plan that addresses both errors and weak spots.

That may mean identifying inaccurate, outdated, unverifiable, or misleading items and using a structured dispute process to address them. It may also mean reviewing utilization, collections, late payments, charge-offs, and thin-file issues in the context of FHA, VA, USDA, or conventional mortgage preparation. If collections are part of the problem, a practical outside resource is Fintrack's guide on how to remove collection items from a credit report, which helps explain how documentation and account status matter.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation to better understand your options.

If you want to understand the credit repair process, start there before making changes that could affect a mortgage timeline. Results vary because every file is different, every creditor responds differently, and lasting improvement depends on both documentation and current credit behavior.

Frequently Asked Questions About Adding Tradelines

Can I be denied a mortgage for adding a tradeline

Yes. If an underwriter believes the tradeline was purchased or rented to inflate your score, they may ignore it or escalate the file for review. That doesn't guarantee denial, but it absolutely creates risk.

How much does it cost to add a tradeline

If a family member adds you as an authorized user, it generally shouldn't cost you anything. The verified USDA-related data states that purchased tradelines are commonly marketed in the $200–$2,500 range and often disappear quickly, which is exactly why I don't recommend paying for them.

How long should an authorized user tradeline stay on my report

For mortgage purposes, stability matters more than speed. A tradeline that shows up and then disappears during the application process can hurt credibility. The safer approach is to make sure any legitimate tradeline remains consistent throughout the mortgage timeline.

Will adding tradelines fix a bad credit report

No. It can help support a thin file, but it won't erase charge-offs, collections, late payments, or inaccurate reporting. If your report has errors, those need to be reviewed and disputed through a documentation-based process.

Is adding tradelines to credit enough for FHA or VA approval

No single tactic is enough. Lenders still review payment history, utilization, debt obligations, file stability, and overall borrower readiness.

Superior Credit Repair provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges. If you're dealing with a thin file, collections, late payments, charge-offs, high utilization, or credit report errors, the smartest next step is to get a professional review before you apply. You can learn more at Superior Credit Repair.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile. Share your feedback on Google