A collection letter shows up in the mail. The bill looks medical. The date of service feels distant. You may have changed insurance since then, moved, or forgotten the account entirely. Now you're trying to buy a home, qualify for an auto loan, or keep your credit profile stable, and one old bill suddenly feels much bigger than it did before.

That moment creates two kinds of stress at once. First, you want to know whether the debt is still legally enforceable. Second, you want to know what it can still do to your credit. Those are related questions, but they are not the same question.

That's where the statute of limitations on medical debt in California matters. It can affect whether a collector can sue. Separately, credit reporting rules affect whether the account can appear on your credit report and influence financing decisions. If you're preparing for a mortgage, apartment approval, refinance, or other major application, understanding that difference can help you respond calmly instead of reacting in a way that hurts your position.

Table of Contents

- Introduction A Surprise Bill and Your Financial Future

- What Is the Statute of Limitations on Medical Debt in California

- How California's 2025 Laws Changed Medical Debt on Credit Reports

- What to Do When a Collector Calls About Old Medical Debt

- Using the Statute of Limitations as a Defense If Sued

- Building Your Lender-Ready Credit Profile

- Frequently Asked Questions About California Medical Debt

- Can making a small payment on an old medical debt cause problems

- If a collector bought the debt from someone else, does that reset the timeline

- Does California's medical debt credit reporting law stop lawsuits too

- Should I talk to a mortgage lender before dealing with old medical debt

- What if the medical debt information on my credit report looks wrong

Introduction A Surprise Bill and Your Financial Future

A first-time homebuyer pulls credit before speaking with a lender. An old medical collection appears in conversation with a collector, even though the treatment happened years ago. A renter getting ready to buy a home wonders whether one forgotten emergency room bill can derail everything.

That confusion is common because medical debt sits at the intersection of healthcare billing, collection law, and credit reporting. Patients often do not receive clear instructions when the original bill arrives. Then, much later, they're expected to know what's collectible, what's reportable, and what actions could make things worse.

Why this topic matters so much for borrowers

If you're focused on mortgage readiness, this issue isn't just legal. It's practical. Lenders review the overall condition of your credit profile, including collections, disputed items, payment habits, and file stability. Even when a debt is old, you still need to know how to respond in a way that protects your options.

A medical bill can create stress long after treatment ends, especially when the consumer is trying to move forward financially.

People often make the same mistake. They panic, call the collector, and say too much. They admit the debt is theirs, promise a payment, or send a small amount just to stop the calls. That kind of reaction can change the situation in ways they didn't intend.

The key question behind the fear

The legal time limit is there to place boundaries on when a creditor or collector can use the court system. That doesn't mean the debt vanishes on its own. It means you need to understand where the debt stands, what rights you still have, and what response makes sense now.

This is especially important in California because recent credit reporting protections altered the situation for medical debt. If you're searching for answers about the statute of limitations medical debt California consumers should know, the best next step is to slow down, gather dates, and separate legal enforceability from credit reporting impact.

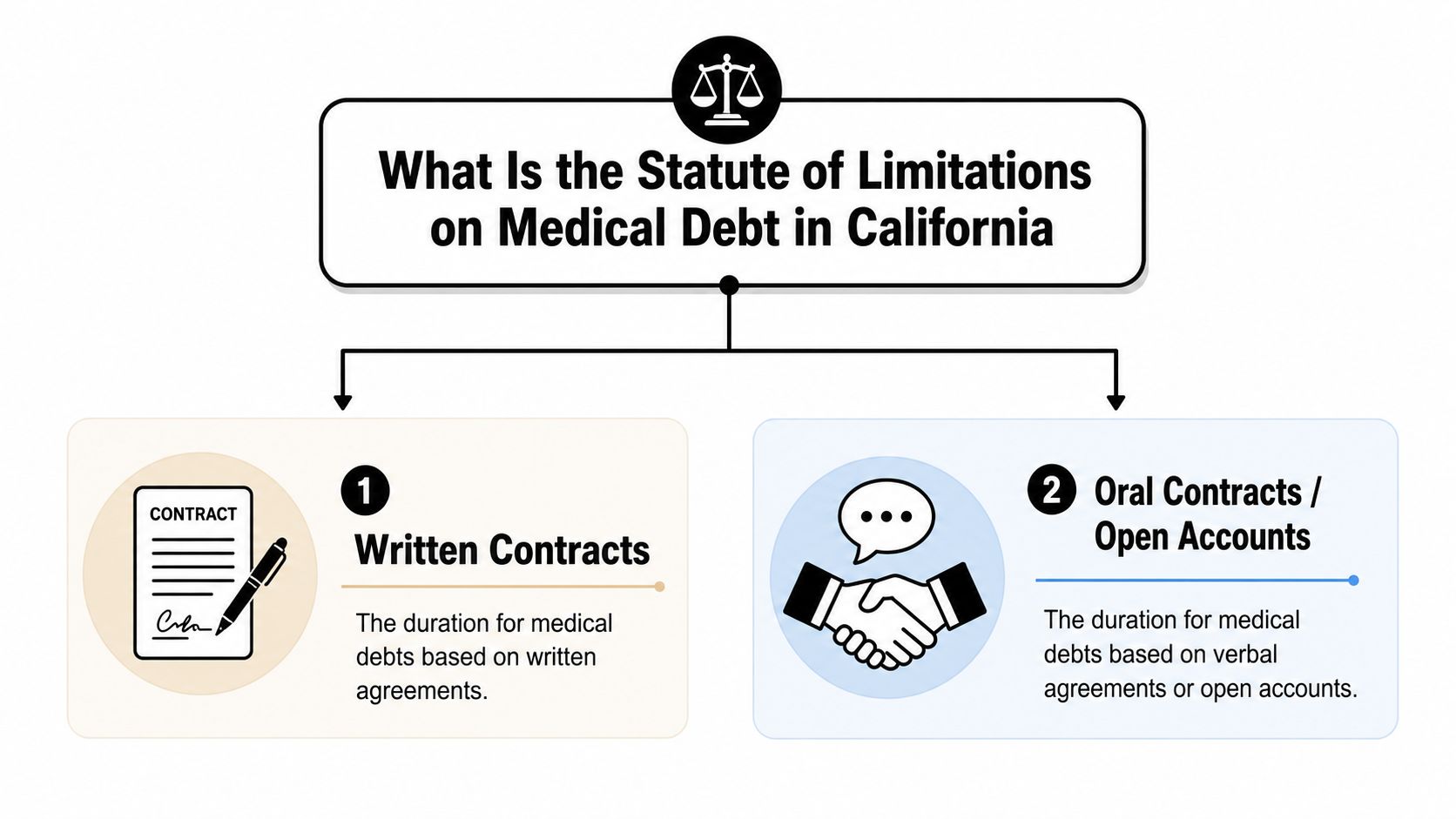

What Is the Statute of Limitations on Medical Debt in California

California generally treats most medical bills as written-contract debts with a 4-year statute of limitations, which means a provider or collector typically has 4 years from the triggering event, often the last payment, default, or breach, to file suit. A partial payment or written acknowledgment can restart that clock, according to this California medical debt limitations overview.

Why most medical debt falls under the contract rule

Most patients sign paperwork when they receive care. That paperwork often creates the written agreement collectors rely on later. For that reason, medical debt in California is usually analyzed under the state's contract framework rather than under a special medical-debt rule.

That matters because people often assume a medical bill has a unique legal deadline that works differently from other debts. In many cases, it doesn't. The account is treated much more like another contract-based obligation.

If you're preparing to repair credit for California homebuyers, this distinction matters because old collections can affect lender conversations even when the legal right to sue may be limited.

What starts the clock and what can restart it

The most important concept is the triggering event. In plain English, that means the event that starts the legal countdown. For many medical accounts, the relevant date may be tied to the last payment, the default, or the breach.

Here's where readers get tripped up. They focus only on the treatment date. That's understandable, but it may not be the date that controls the legal timeline.

A second point causes even more problems: some actions can restart the clock. The source above notes that a partial payment or written acknowledgment can reset the timeline. So if a collector contacts you about a very old account, even a small payment or a written statement confirming the debt may have consequences.

Practical rule: Before you pay, promise to pay, or confirm the account in writing, make sure you understand whether the debt may already be time-barred.

A simple way to think about it

Think of the statute of limitations like a legal timer attached to the right to sue. It doesn't measure whether the bill ever existed. It measures whether the collector can still ask a court to enforce it.

This table can help:

| Situation | What it usually means |

|---|---|

| Debt is within the limitations period | A lawsuit may still be legally possible |

| Debt may be outside the limitations period | The debt may still exist, but a lawsuit may be barred if you properly raise that defense |

| You make a partial payment or acknowledge it in writing | The legal timeline may restart |

One more note. People sometimes hear about oral agreements and assume that applies to their hospital bill. In practice, signed intake forms and treatment paperwork often make the written-contract analysis the more relevant one. If the paperwork is unclear, it's wise to review the records closely before you respond.

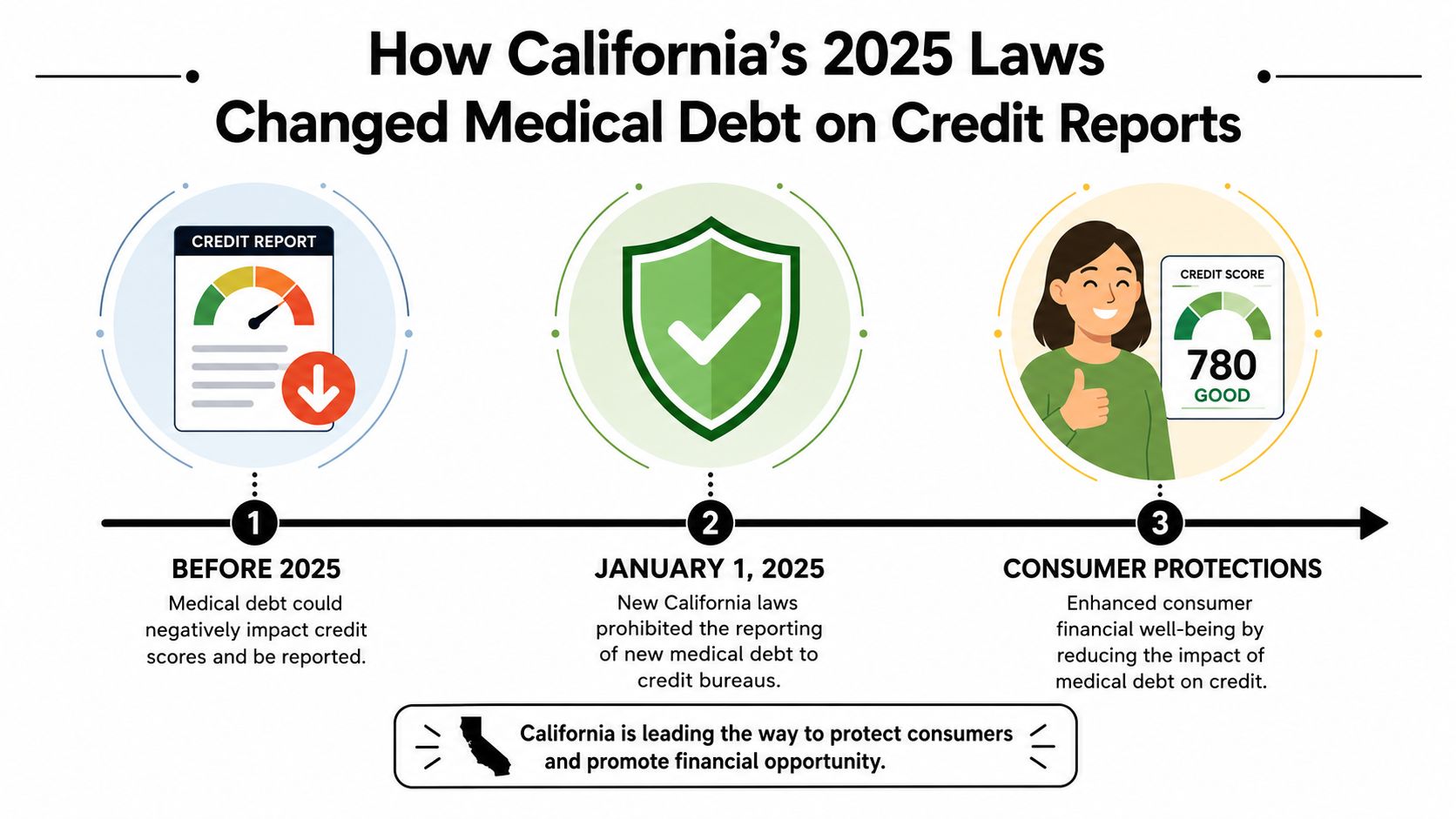

How California's 2025 Laws Changed Medical Debt on Credit Reports

California added major consumer protections in 2025. Effective January 1, 2025, the state prohibited medical debt from being reported to credit agencies, and effective July 1, 2025, new medical-debt contracts had to include a disclosure stating the debt cannot be furnished to a credit reporting agency. California law also requires hospitals and debt collectors to wait 180 days after the initial billing before reporting negative information or filing a civil complaint, as explained in this summary of California's medical debt disclosure law.

What changed in California

For consumers, this is one of the most important updates in recent years. Many older articles still talk about medical collections as if nothing has changed. California changed the credit reporting side of the conversation.

That means a medical debt issue can no longer be understood by asking only one question. You now need to ask at least two:

- Can this debt still be reported to a credit bureau?

- Can the creditor or collector still sue on it?

Those are separate legal tracks. A debt may fall into one category for reporting and another for lawsuits.

For a broader industry explanation of how changing collection rules affect collector behavior and compliance, this overview of Intelligent Contacts on debt collection laws is a useful background resource.

Why credit reporting and lawsuits are different issues

A lot of consumers assume that if something can't appear on a credit report, it also can't lead to legal action. That assumption can create real problems. Credit reporting restrictions deal with what can be furnished to the credit agencies. The statute of limitations deals with the ability to sue.

Those are not interchangeable protections.

The waiting period matters too. California requires a 180-day buffer after the initial billing before reporting negative information or filing a civil complaint under the source cited above. That gives patients time to sort out insurance issues, billing errors, charity care questions, or payment arrangements before the situation escalates.

If you're evaluating an old medical account, always separate these issues: reporting, collection contact, and the right to sue.

If you're buying a home soon, it also helps to understand how medical collections fit into the rest of the underwriting picture. This HRRG guide for homebuyers can help you think about how lenders may review your broader credit file.

What this means for mortgage readiness

From a mortgage-readiness perspective, California's 2025 protections are helpful, but they don't eliminate the need to review your reports carefully. Credit files can still contain errors, outdated information, or items that require documentation to challenge.

That's why consumers preparing for FHA, VA, USDA, or conventional financing should review all three reports and compare account dates, account ownership, and account status. The main goal isn't to panic over every collection reference. The goal is to identify what is accurate, what is obsolete, and what may need formal dispute follow-up.

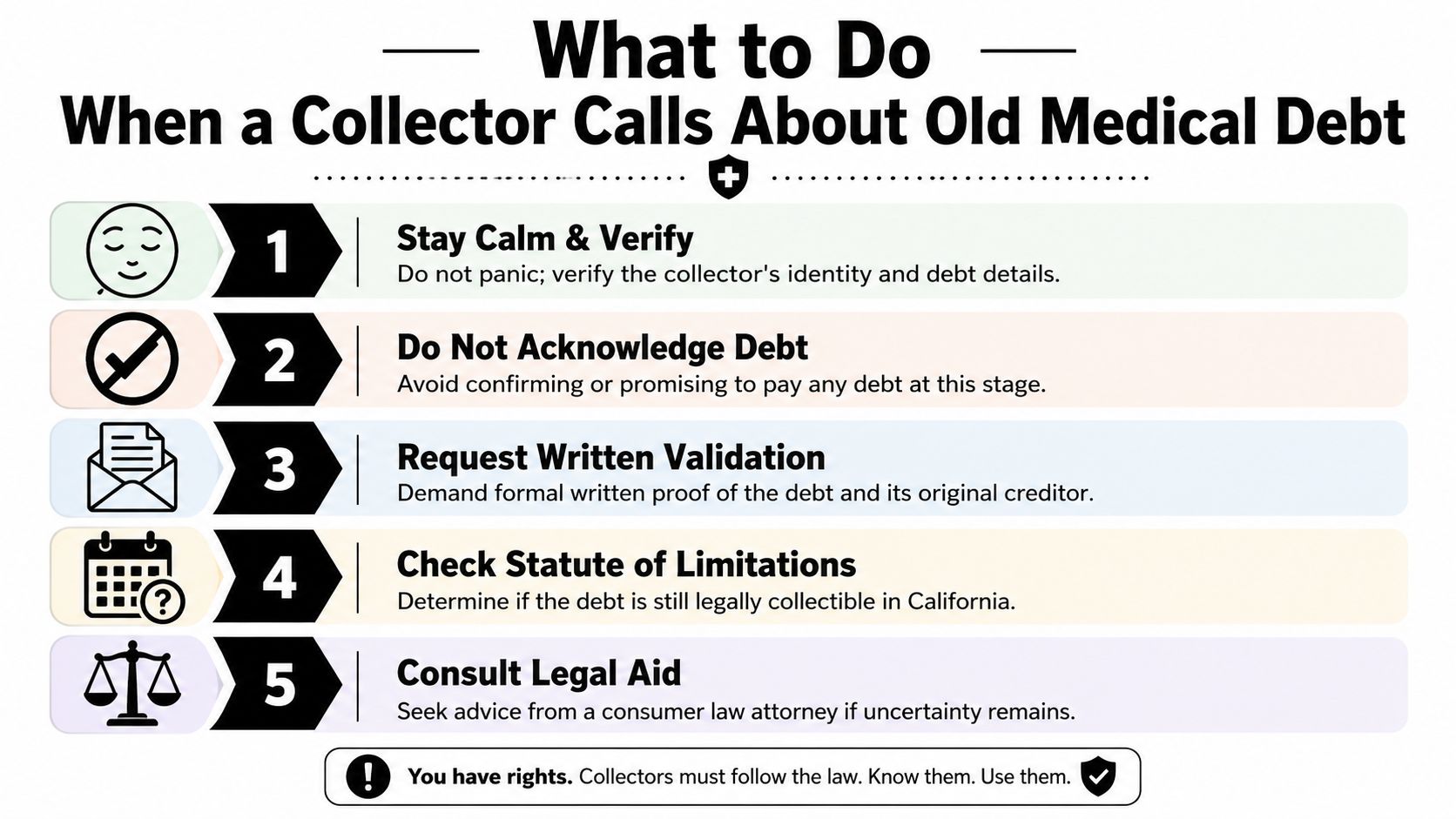

What to Do When a Collector Calls About Old Medical Debt

When a collector calls about an older medical bill, your first job is simple. Don't make the call longer than it needs to be.

You don't need to debate the debt. You don't need to explain your medical history. You also don't want to casually say, “Yes, that sounds familiar,” if you haven't reviewed the records.

What to say on the phone

A calm response works best. You can say that you won't discuss the matter by phone and that you want all communication in writing. That keeps the interaction controlled and gives you time to review dates and documents.

A short script could sound like this:

“Please send me the details in writing. I'm not admitting responsibility for the debt, and I won't discuss payment by phone.”

That approach helps for two reasons. It limits off-the-cuff statements, and it moves the conversation into a format you can document.

What to request in writing

Once you receive written contact, ask for validation of the debt. You want the collector to provide enough information to identify the account and support the claim that they have the right to collect.

Your written request can ask for:

- The original provider name so you know where the bill started

- The amount claimed so you can compare it with any records you still have

- The date of service or account history to help you evaluate age and timing

- Proof of collection authority showing why this company is contacting you

- A copy of the agreement or billing basis if available

If you want a starting point for format and language, this legal debt dispute form is a practical template.

Consumers who need help organizing collection disputes can also review Superior Credit Repair solutions for general education on collection-related credit issues.

Mistakes that can make an old debt riskier

Some mistakes happen because people want to be cooperative. Others happen because they're tired of collection calls. Either way, the result can be the same.

Avoid these common errors:

- Don't admit the debt is yours immediately. You may not have enough records yet.

- Don't promise payment on the first call. A rushed promise can box you in before you know the legal status.

- Don't send a token payment just to stop the contact. With older accounts, that can create new problems.

- Don't rely on the collector's timeline alone. Check your own records and compare dates.

A good working mindset is this: slow the process down, get documents, and respond based on facts.

Using the Statute of Limitations as a Defense If Sued

Receiving a court summons is different from receiving a collection letter. At that point, the issue is no longer just whether the debt feels old. The issue is whether you respond properly and on time.

An expired statute of limitations can be a defense, but the court usually won't raise it for you automatically. You generally must assert it.

Why ignoring the lawsuit is the worst option

Many consumers freeze when legal papers arrive. They assume that because the debt is old, the case will collapse on its own. That's a dangerous assumption.

If you ignore the lawsuit, the plaintiff may seek a default judgment. Once that happens, you lose the chance to raise defenses in the ordinary way. Even a debt that might have been challenged can become much harder to fight after default.

A time-barred debt defense only helps if the defendant actually raises it in the case.

What an affirmative defense means

An affirmative defense is a legal argument you include in your written response to the complaint. In debt cases, the written response is commonly called an Answer.

In plain English, your Answer tells the court which allegations you deny, which you don't have enough information to admit, and what defenses apply. If the debt is outside the applicable limitations period, that defense needs to appear in the Answer.

This simple comparison helps:

| Court paper | What it does |

|---|---|

| Complaint | The plaintiff's claim against you |

| Summons | Notice that you've been sued and must respond |

| Answer | Your formal response and defenses |

If you need a plain-language resource before drafting correspondence or reviewing your documents, you can Download debt validation letter samples.

Sample language you can discuss with counsel

A consumer or attorney may use language along these lines in an Answer, adapted to the facts of the case:

“Defendant alleges that Plaintiff's claim is barred by the applicable statute of limitations under California law.”

That sample is not a substitute for legal advice, and the right wording depends on your records, dates, and procedural posture. But it shows the basic idea. You are telling the court that even if the plaintiff alleges a debt exists, the claim may be legally too old to enforce through a lawsuit.

If you've been sued, gather every document you can find. Look for prior billing statements, proof of any payments, letters from prior collectors, insurance explanations of benefits, and your credit reports. Dates matter. So does the exact identity of the plaintiff.

Building Your Lender-Ready Credit Profile

Homebuyers often assume that once a medical debt becomes less threatening legally, the problem is over. In real lending, it's more nuanced than that. Mortgage underwriting looks at the full condition of your file, including whether reported information appears accurate, current, and explainable.

What lenders usually care about

Lenders tend to look for a credit profile that is stable and well documented. They want to see whether collections, late payments, balances, and disputes create uncertainty. For many borrowers, the issue isn't a single account by itself. It's whether the file as a whole looks clean enough to support approval review.

That's why old medical debt still matters in practice. Even when California's newer reporting rules offer protection, consumers should still review reports carefully for outdated, inaccurate, misleading, or unverifiable information. A problem doesn't always disappear just because the law changed. Sometimes the file still needs correction.

How to handle outdated or questionable reporting

A practical credit-restoration approach usually includes these steps:

- Review all credit reports carefully and compare names, dates, balances, and account status

- Flag any item that appears inaccurate or outdated and gather supporting records before disputing

- Document medical billing confusion clearly if insurance processing or account transfers created inconsistencies

- Keep positive credit behavior steady while disputes are pending, especially payment history and revolving balances

For borrowers aiming at FHA, VA, USDA, or conventional financing, this work supports a more lender-ready file. It doesn't guarantee approval, deletion, or a specific score result. Results vary based on the contents of the file, available documentation, creditor responses, and current credit behavior.

If you want structured help evaluating questionable accounts and organizing next steps, Superior Credit Repair guidance can help you understand the documentation-based process.

Frequently Asked Questions About California Medical Debt

Can making a small payment on an old medical debt cause problems

Yes, it can. As discussed earlier, a partial payment can restart the legal clock on some accounts. That's why it's wise to review the account history before sending money on an older debt.

If a collector bought the debt from someone else, does that reset the timeline

A transfer to a new collection agency does not usually change the original age of the debt by itself. What matters is the account history and the legally relevant dates, not just the fact that a different company is contacting you now.

Does California's medical debt credit reporting law stop lawsuits too

Not automatically. Credit reporting restrictions and lawsuit rights are separate issues. A debt may be non-reportable while still raising legal questions that depend on the account's timeline and the facts of the case.

Should I talk to a mortgage lender before dealing with old medical debt

If you plan to buy soon, that can be helpful. A lender or mortgage professional can tell you how your full file may be viewed. Then you can decide which items need documentation, correction, or dispute attention before application.

What if the medical debt information on my credit report looks wrong

Start by gathering records and comparing the account across all reports. If information appears inaccurate, outdated, unverifiable, or misleading, a formal dispute process may be appropriate. Keep copies of everything you send and receive.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. If you're preparing for a home purchase, refinance, auto financing, or general credit rebuilding, you can request a free credit analysis or consultation through Superior Credit Repair to better understand your options. Credit repair and credit restoration are documentation-based processes, and results vary based on each person's credit file, account history, creditor responses, and current credit behavior.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile.