Debt-to-income ratio, or DTI, is the percentage of your gross monthly income that goes toward your monthly debt payments. For many homebuyers, a DTI below 36% is the ideal target, while 43% is a common maximum for many mortgage types.

If you're getting ready to buy a home, you've probably already looked at your credit score, savings, and down payment. Then a lender asks about your DTI, and suddenly it feels like there's another financial rule you were supposed to know all along.

That confusion is common. Many first-time homebuyers assume that if the future mortgage payment looks affordable, they should be fine. But lenders don't just look at the house payment. They also look at the rest of your monthly debt, and that difference is where many approvals and denials are decided.

For families preparing for FHA, VA, USDA, or conventional mortgage approval, DTI often sits right beside credit report accuracy, utilization, collections, and payment history. If you're also working through credit repair, mortgage credit repair, or credit repair before buying a home, understanding DTI helps you make smarter next steps instead of guessing.

Table of Contents

- Your First Step Toward Mortgage Approval Understanding DTI

- How to Calculate Your Debt to Income Ratio

- Front-End vs Back-End DTI A Critical Distinction

- How Mortgage Lenders Analyze Your DTI Ratio

- Actionable Strategies to Lower Your DTI for Mortgage Approval

- Common Questions About Debt to Income Ratio

- Your Next Steps Toward a Lender-Ready Credit Profile

Your First Step Toward Mortgage Approval Understanding DTI

A lot of homebuyers first hear about DTI after they feel fairly prepared. They've saved some money, checked their scores, maybe paid down a card or two, and then a loan officer says, "Let's look at your debt-to-income ratio."

At that moment, many people assume DTI is just another way of measuring credit. It isn't. Your credit score reflects account history and risk patterns. Your DTI shows how much of your pre-tax income is already committed to monthly debt payments. Lenders use it because they want to know whether the new mortgage payment fits into your real monthly budget.

Why this number matters so much

DTI can affect more than a yes or no decision. It can influence the loan options available to you, the level of documentation a lender wants, and how comfortable an underwriter feels with your file.

A first-time buyer might have a reasonable future house payment but still struggle to qualify because of credit card minimums, a car loan, student loans, or installment debt. That's why DTI often becomes a key part of mortgage readiness right alongside dispute negative accounts, collections dispute help, late payment dispute help, and credit utilization planning.

DTI isn't meant to discourage you. It's a snapshot of affordability, and snapshots can change when you take the right steps.

Why many first-time buyers feel blindsided

The biggest surprise is that lenders may see your debt picture differently than you do. You may think, "I pay my cards off most months," while the lender looks at the minimum required payment. You may think a small financing plan or recurring obligation doesn't matter much, but if it shows up as recurring debt, it can affect the file.

If you're working on mortgage preparation, including understanding FHA credit requirements, DTI deserves the same attention as your scores and your reports. Once you understand how it's measured, you can start making decisions that move the file in the right direction.

How to Calculate Your Debt to Income Ratio

DTI math is straightforward. The harder part is knowing which monthly payments a lender counts and which expenses stay outside the formula.

The basic formula

DTI formula: (Total Monthly Debt Payments / Gross Monthly Income) × 100

Start with two numbers:

- Your total monthly debt payments

- Your gross monthly income, which is your income before taxes

Then divide debt by income and multiply by 100 to turn it into a percentage.

What to include and what to leave out

This is the part of the calculation that often causes confusion. As Experian explains in its DTI overview, lenders focus on required monthly debt payments, not the flexible expenses in your day-to-day budget.

A simple way to look at it is this: DTI measures obligations that are already spoken for each month. It does not try to capture every dollar you spend.

Use this checklist:

- Include housing obligations: If you are estimating a mortgage scenario, use the proposed full housing payment. That can include principal, interest, property taxes, homeowners insurance, and HOA dues.

- Include credit card minimums: Use the minimum required payment, even if you plan to pay more.

- Include installment loans: Car loans, personal loans, and student loans count if they require a recurring monthly payment.

- Include court-ordered payments: Child support, alimony, and certain judgments may be part of the lender's calculation.

- Include documentable gross income: Wages, salary, and other qualifying income sources count if the lender can verify them.

- Leave out regular living expenses: Groceries, utilities, gas, streaming services, and cell phone bills are part of your budget, but they are generally not part of DTI.

That difference trips up many first-time buyers. A person may feel financially fine because they manage bills well each month, yet the lender is looking at fixed required payments on the credit report and in the application file.

A simple example

Say a homebuyer earns $9,000 in gross monthly income and has these required monthly payments:

- Credit card minimums: $250

- Auto loan: $450

- Student loan: $300

- Proposed mortgage payment: $2,000

That brings total monthly debt payments to $3,000.

Now divide $3,000 by $9,000. You get 0.33. Multiply by 100, and the DTI is 33%.

Small changes can move this number faster than buyers expect. If credit card minimums rise because balances increase, or if a disputed account is still reporting an active payment, your DTI can climb even before you take on a new mortgage.

That is why DTI reduction often overlaps with credit repair work. Paying down revolving balances can lower minimum payments. Correcting reporting errors can remove debt that should not be counted. Avoiding new financing before applying can keep the ratio from drifting higher. These are practical steps that can improve how your file looks to a lender.

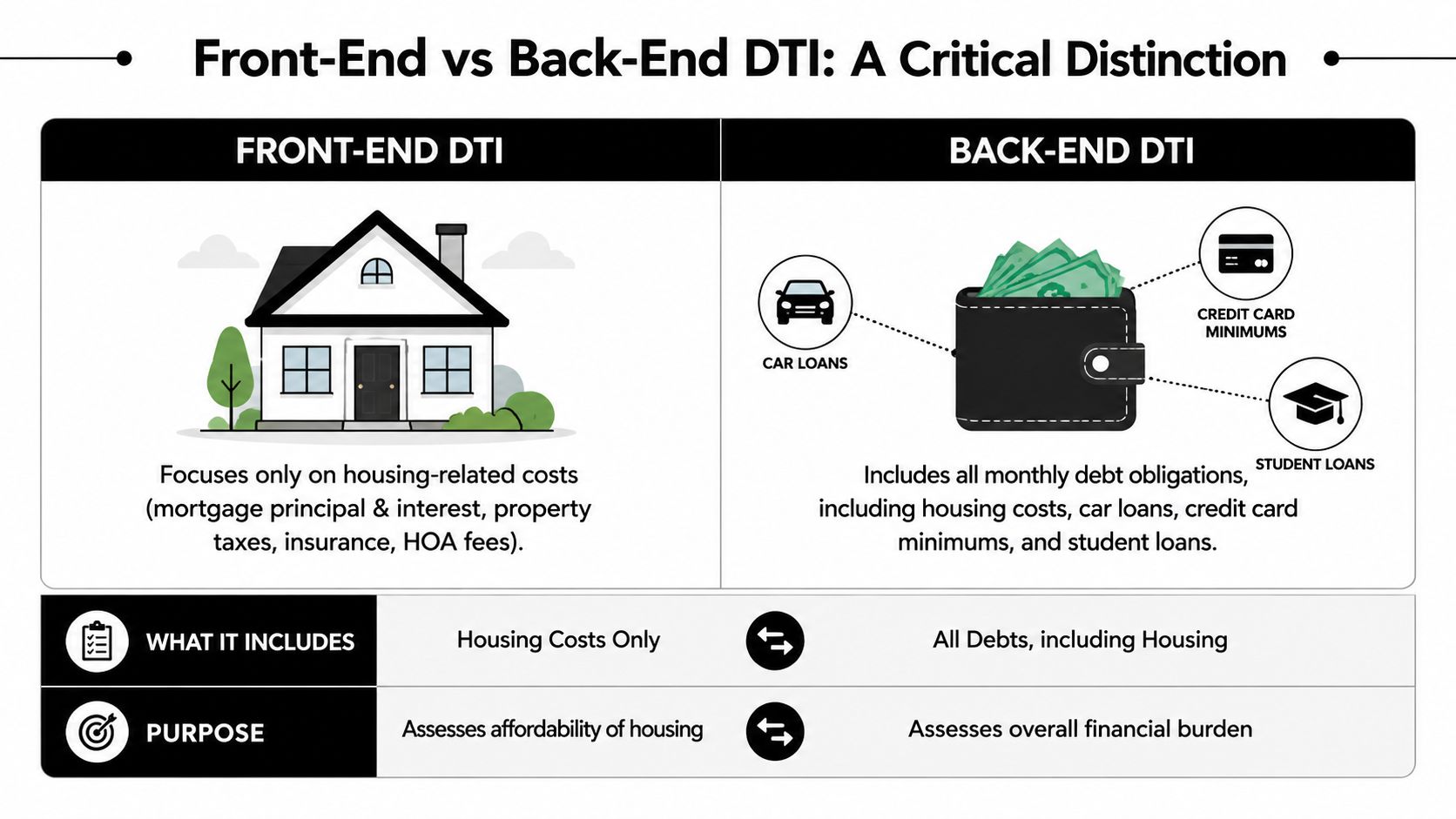

Front-End vs Back-End DTI A Critical Distinction

You find a home that fits your budget on paper. The projected mortgage payment looks reasonable. Then the lender says the debt-to-income ratio is still too high.

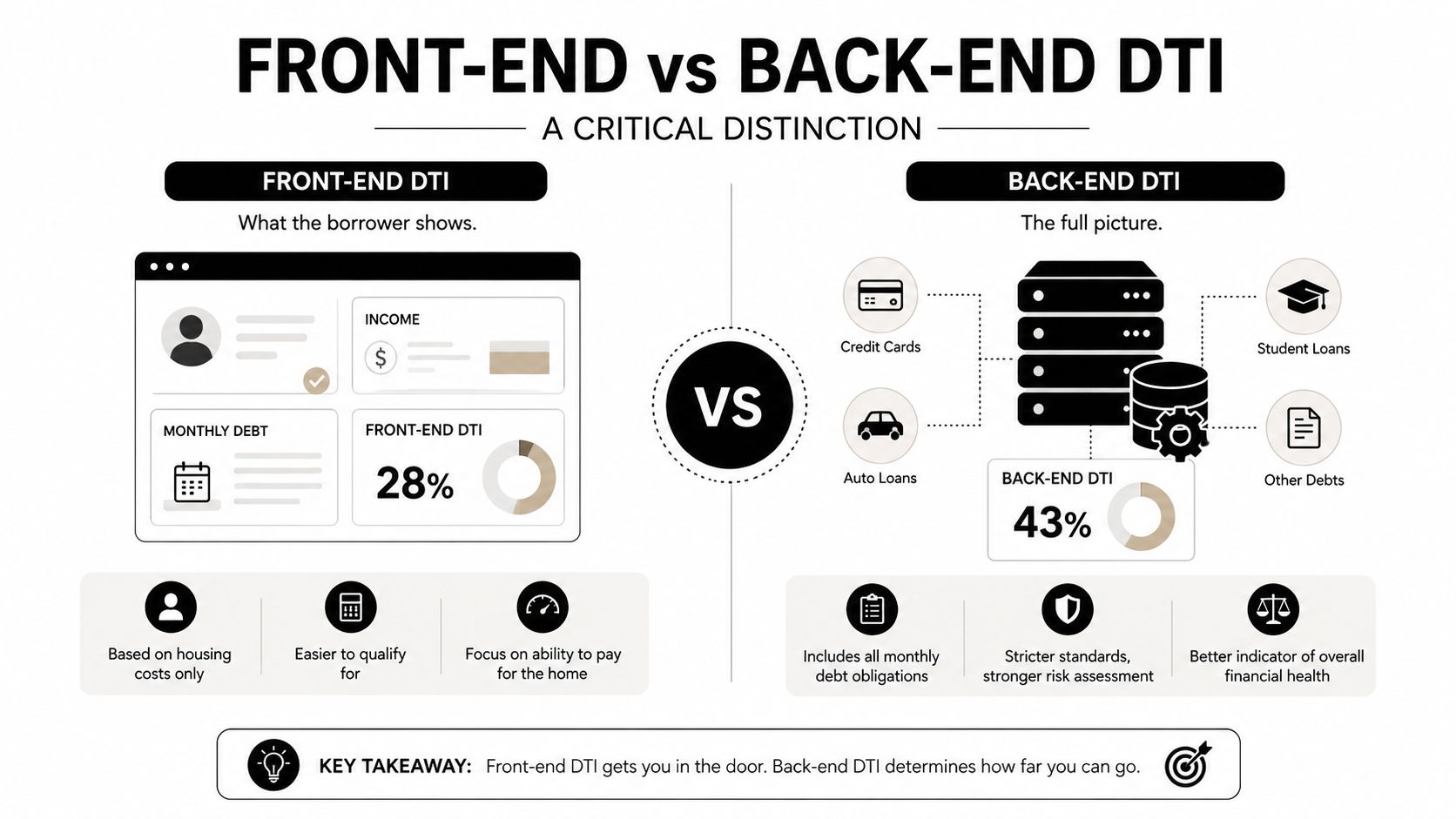

That usually comes down to a mix-up between front-end DTI and back-end DTI. First-time buyers often hear "DTI" as if it were one number, but underwriters often look at two. One measures the house payment by itself. The other measures the house payment plus your other required monthly debts.

Why this distinction causes so much confusion

Front-end DTI is your housing ratio. It looks at the proposed mortgage payment and compares it with your gross monthly income.

Back-end DTI is your total debt ratio. It includes the mortgage payment, plus credit card minimums, auto loans, student loans, personal loans, and other recurring obligations that must be paid each month.

A simple way to picture it is this: front-end asks whether the home payment fits. Back-end asks whether the home payment still fits after the rest of your monthly debt is counted.

That second question is where many approvals get harder.

A buyer may have a house payment that seems well within reach, yet the file still struggles because existing debts are already taking up too much income. That is why a strong front-end ratio does not always protect you from a denial.

What lenders are really comparing

Many lenders have long used the 28/36 Rule as a benchmark. PNC's overview of the 28/36 rule explains the idea clearly: housing is often evaluated separately from total debt, and the total debt number is usually the tighter pressure point for buyers carrying other monthly payments.

Here is where the confusion becomes practical. A borrower might keep the proposed mortgage payment near the housing target, but a car loan, rising credit card minimums, student debt, or a personal loan can push the back-end ratio far higher than expected.

A file can look safe through the front-end lens and still look overextended through the back-end lens.

Why back-end DTI often improves through credit repair work

Back-end DTI is the ratio that tends to change when you reduce or correct debts. That makes it closely tied to credit repair steps before a mortgage application.

For example, paying down revolving balances can lower your required minimum payments. Disputing and removing an account that should not be reporting can eliminate a monthly obligation from the file. Avoiding new financed purchases keeps fresh payments from appearing right before underwriting. Each of those actions can improve the back-end ratio, even if the proposed mortgage payment stays exactly the same.

This is also why borrowers sometimes feel blindsided. They focus on the future house payment, while the lender is also studying the debts already attached to the credit profile. If you want a fuller picture of how those items are reviewed together, this guide to understanding mortgage lender criteria can help.

One practical rule applies here: front-end DTI tells you whether the home looks affordable by itself. Back-end DTI tells the lender whether your full monthly debt load leaves enough room for that home. For many first-time buyers, that is the number that needs the most attention before applying.

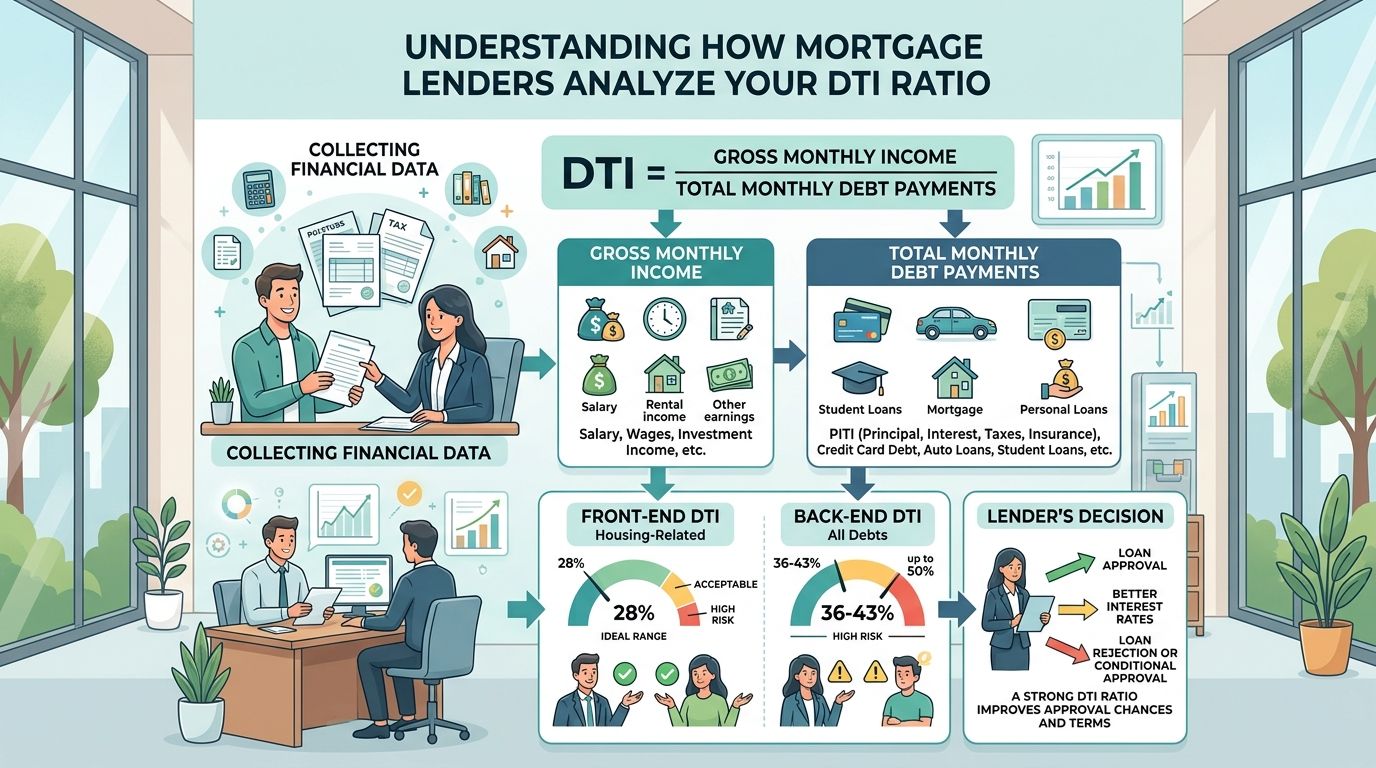

How Mortgage Lenders Analyze Your DTI Ratio

Lenders don't review DTI in isolation. They use it as part of a broader risk review that also includes credit history, reserves, documentation, loan type, and overall file stability.

What lenders usually consider healthy

A useful place to start is the standard mortgage benchmark many buyers hear about first. The 28/36 Rule has influenced underwriting for decades. According to the verified guidance above, that means keeping housing at no more than 28% of gross income and total debt at no more than 36%.

For broader mortgage eligibility, the verified data also shows an important split:

| DTI range | How lenders often view it |

|---|---|

| Below 36% | Often viewed as the strongest range for healthy debt management |

| 36% to 43% | Often considered acceptable, though the file may face more scrutiny |

| 44% or higher | Often considered higher risk and may require stronger compensating factors |

According to Chase's overview of debt-to-income ratio and mortgage risk, 43% is a common maximum threshold for a Qualified Mortgage, while below 36% is often viewed as the healthier target. The same source notes that borrowers at 44% or higher are often seen as higher risk and may need compensating factors such as a FICO score of 720+.

Why loan type and overall file strength matter

Many online guides oversimplify the process. Different lenders use different comfort zones, and mortgage programs handle risk differently.

Verified underwriting guidance in the material above shows that for manually underwritten Fannie Mae loans, total DTI is traditionally capped at 36%, but it can go up to 45% with specific credit score and reserve requirements, and up to 50% through Fannie Mae's automated underwriting system. FHA and other government-backed programs may also allow higher ratios when the rest of the file is stronger.

That doesn't mean a high DTI is harmless. It means underwriters may balance the whole file. Stronger reserves, better payment history, lower utilization, and cleaner reporting can matter.

Practical rule: DTI tells lenders how stretched your budget looks today. Credit history helps them judge how you've handled obligations over time.

If you're comparing your own situation against lender expectations, this guide to understanding mortgage lender criteria can help connect DTI with the other issues underwriters review, including collections, late payments, charge-offs, and overall account stability.

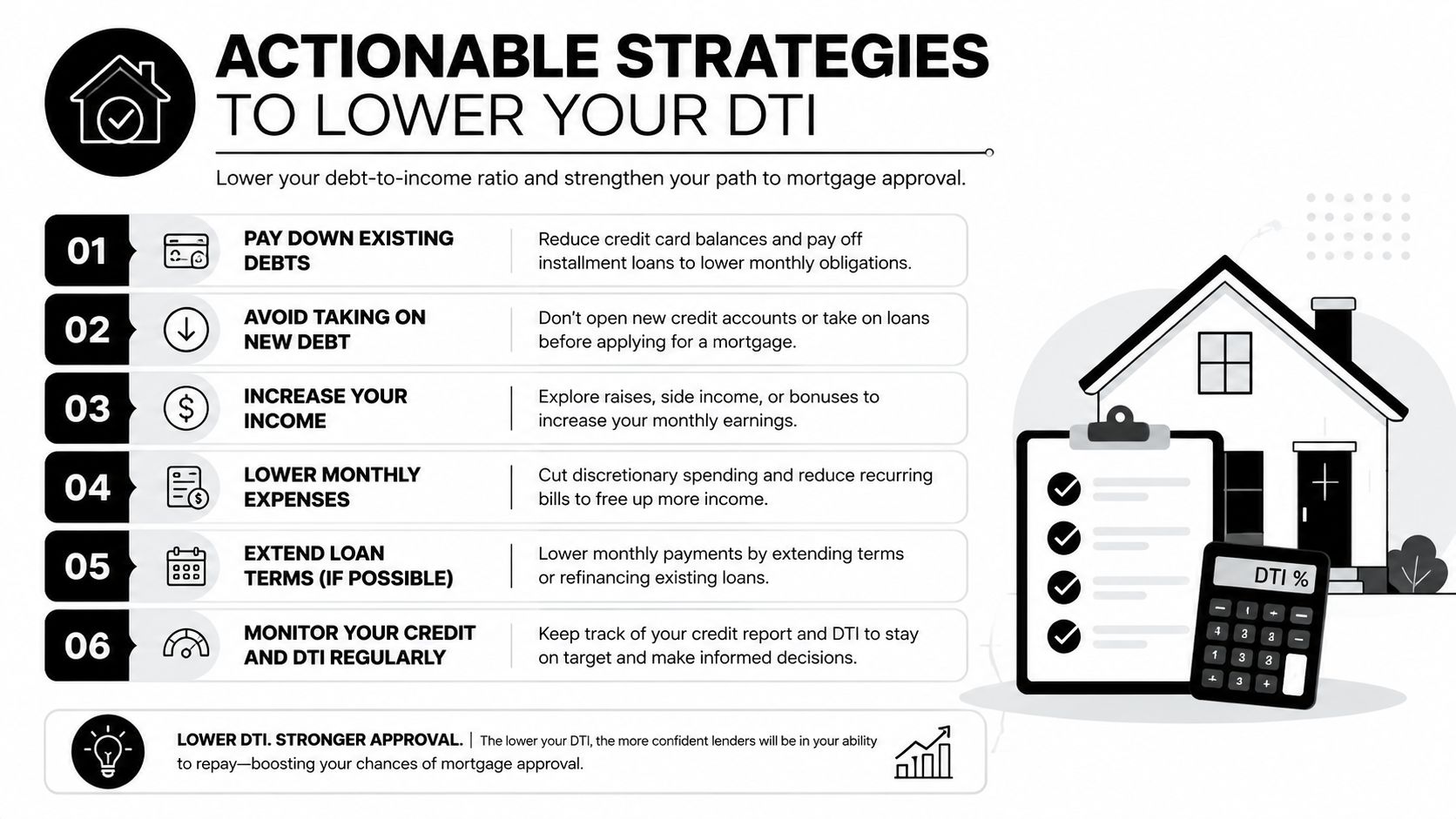

Actionable Strategies to Lower Your DTI for Mortgage Approval

The good news is that DTI isn't fixed. It's one of the few mortgage readiness factors you can often improve by changing either side of the formula. You can reduce counted monthly debt, increase documentable income, or both.

Reduce the payments that count against you

The fastest DTI improvements usually come from lowering monthly obligations that appear in underwriting.

- Pay down revolving balances: Lower credit card balances can reduce the minimum monthly payment that counts in your back-end ratio. This can also support utilization, which may help your broader credit profile.

- Eliminate smaller installment loans when possible: Paying off a personal loan or another fixed monthly obligation can remove that payment from the debt side of the formula.

- Avoid adding new debt before applying: A new auto loan, financing plan, or card balance can change the numbers quickly and may also affect your lender-ready credit profile.

- Document all qualifying income carefully: Gross income includes pre-tax income, and lenders may count multiple sources when properly documented. Missing paperwork can make DTI look worse than it really is.

- Review recurring obligations line by line: Many borrowers underestimate how much small monthly payments affect the back-end ratio.

According to the verified data tied to the Consumer Financial Protection Bureau, a DTI above 43% is a critical threshold for Qualified Mortgages, and reducing DTI from 40% to 32% can increase approval odds for FHA and conventional loans by over 25%. That doesn't guarantee an approval, but it shows why lowering DTI can be one of the most productive pre-application steps.

Use credit repair as part of a larger mortgage readiness plan

DTI reduction isn't only about paying debts. Sometimes it's also about confirming that the debts being counted are accurate.

If your reports contain inaccurate, outdated, unverifiable, or misleading information, a structured credit repair and credit restoration process may help you identify items that should be disputed through proper legal and documentation-based channels. That matters for mortgage credit repair because lenders are reviewing the obligations shown in your file. If a collection account, charge-off balance, or other tradeline is being reported incorrectly, that can affect both the lender's risk view and your planning decisions.

A careful review may also help with:

- Credit report errors: accounts that don't belong to you, duplicate entries, or outdated reporting

- Collections dispute help: especially when a collection is inaccurate or lacks reliable verification

- Late payment dispute help: when reporting details are inconsistent or misleading

- Charge-off dispute help: when balances, dates, or account ownership are being reported incorrectly

- Medical collection credit repair: when medical items create confusion around current obligations

If you want to improve both DTI awareness and overall financing readiness, these top 2026 credit score strategies offer practical credit-building ideas that pair well with debt reduction. Results always vary based on your file, your documentation, creditor responses, and your current credit behavior.

Common Questions About Debt to Income Ratio

A lot of first-time buyers get tripped up here. They hear one DTI number from an online calculator, then a lender uses a different one because the lender is looking closely at back-end DTI, not just the housing payment. That confusion shows up often in underwriting, especially when student loans, spouse debt, or small recurring credit payments were overlooked.

Does a non-borrowing spouse's debt count

Sometimes it does. The answer depends on the loan program, state property laws, and the lender's underwriting rules.

While homebuyers often focus on the borrower who will sign the note, the lender may still review certain obligations connected to a non-borrowing spouse. That comes up more often in community property states and with some government-backed loans. If you are applying without your spouse, ask the lender one direct question early: which spouse-related debts will be counted in back-end DTI for this file?

That one question can prevent a late surprise after you've already budgeted around the wrong number.

What about student loans in deferment or income-driven repayment

Student loans cause confusion because the payment you feel each month is not always the payment the lender uses on paper.

A lender may still count a student loan obligation even if the loan is deferred or your payment is reduced under an income-driven plan. Front-end DTI looks only at the housing payment. Back-end DTI includes obligations like student loans, auto loans, credit cards, and personal loans. If your back-end number is the one creating pressure, ask the lender which documented student loan payment they will use before you shop at the top of your budget.

Can a strong credit profile offset a higher DTI

Sometimes, but only to a point.

A stronger credit file can help your overall application look more stable. It does not make monthly debt disappear. That is why buyers get confused when they hear they have "good credit" but still run into a DTI problem. The lender may like the credit history and still decline the file because the back-end ratio is too tight.

This is also where credit repair work connects directly to DTI planning. If your reports show inaccurate late payments, duplicate collections, wrong balances, or revolving accounts that should have been updated, fixing those issues may improve how your file is viewed and may reduce the monthly obligations a lender counts. If small fintech payments are part of the problem, this guide on buy now pay later and credit scores can help you spot accounts that feel minor but can still affect underwriting. If revolving debt is a major piece of your back-end ratio, this resource on credit card impact and liability adds useful context.

Which household bills are usually excluded

Regular living expenses are usually not part of DTI. Groceries, utilities, gas, and phone service generally are not counted the way a credit obligation is counted.

A simple way to separate them is this. If the bill is a loan or required debt payment, lenders are much more likely to include it in back-end DTI. If it is a normal monthly living expense without a credit agreement, it usually stays outside the calculation.

That distinction helps explain why two bills that both arrive every month are treated differently. A utility payment is usually just a household expense. A credit card minimum payment is debt. For mortgage approval, that difference matters.

Your Next Steps Toward a Lender-Ready Credit Profile

A lot of first-time buyers get tripped up here. They hear that their income looks strong, assume they are ready, then learn a lender is focused on the wrong side of their DTI from the buyer's point of view. The housing payment may look manageable, but the back-end ratio still gets stretched by credit cards, installment loans, or small monthly accounts that seemed harmless.

That is why your next step is not just "improve credit." It is to line up your credit profile with the DTI formula a lender will use. Front-end DTI asks whether the house payment fits. Back-end DTI asks whether your full debt load leaves enough room for that payment. If those two numbers tell different stories, confusion and delays follow.

A practical plan usually starts with three checks. First, review your credit reports for errors that could inflate the monthly obligations in underwriting. Second, target debts that hurt back-end DTI the most, especially revolving accounts with required minimum payments. Third, avoid adding new financed purchases while you are getting mortgage-ready. If you need more context on how revolving debt affects what lenders see, this resource on credit card impact and liability is useful.

Credit repair fits into this process in a very specific way. Correcting inaccurate balances, duplicate accounts, or outdated derogatory items can change how your file is evaluated. Paying down credit card balances can lower minimum payments and reduce pressure on your back-end ratio. Together, those steps can make your application cleaner, easier to explain, and better aligned with lender guidelines.

DTI is one part of approval, not the whole picture. Your scores, payment history, and account stability still matter, so it helps to review them alongside your debt ratios. For that broader view, this guide to credit scores for homebuyers can help you connect the dots.

If you're preparing for a mortgage and want to make sure your credit is ready, Superior Credit Repair offers a free credit analysis to identify issues, review possible inaccuracies, and outline a step-by-step plan based on your file.