You pull your credit score on a free app and feel relieved. The number looks solid. Then your bank shows a different score. Later, a mortgage lender mentions another one entirely. At that point, most first-time homebuyers ask the same question: which credit score matters?

The honest answer is more practical than people expect. The score that matters is usually the one the lender uses for your specific application. For a mortgage, that often isn't the same score you see in a free app. It also isn't just about one number. Mortgage lenders look at the scoring model, the bureau data behind it, and the actual credit report details that explain why the score looks the way it does.

That distinction matters if you're preparing for FHA, VA, USDA, or conventional mortgage approval. A person can feel ready based on a consumer-facing score, then run into problems because the lender pulled a different model or found issues like recent late payments, collections, charge-offs, or high utilization. If you're trying to become lender-ready, you need to understand the score and the file behind it.

Table of Contents

- The Credit Score Maze Why You See Different Numbers

- FICO vs VantageScore The Two Main Scoring Systems

- Why Your Credit Score Changes From Place to Place

- Industry-Specific Scores The Numbers Lenders Really Use

- How Mortgage Lenders Use Your Scores The Tri-Merge and Middle Score Rule

- How to Improve the Score That Matters for Your Goal

- Frequently Asked Questions About Credit Scores

The Credit Score Maze Why You See Different Numbers

The confusion usually starts with a simple moment. You check one score on your phone, another through your bank, and another after talking to a lender. None of them match. That doesn't automatically mean one is wrong.

In practice, the credit score that matters for mortgage and most consumer lending decisions is usually the FICO score version the lender pulls, not the number shown in a free app. FICO says its scores are used by 90% of top lenders, as summarized in this explanation of which credit score matters most.

A useful way to think about this is measurement. If one person uses inches and another uses centimeters, both are measuring length. They're just using different rulers. Credit scoring works the same way. Different companies build different scoring models, lenders choose the model that fits their risk process, and the result is that you may have several real scores at the same time.

Why this feels so frustrating to homebuyers

A first-time homebuyer often wants one clean answer. "Tell me the score I need." The problem is that mortgage lending isn't built around one universal number visible everywhere. It's built around a lender's chosen scoring model, the credit bureau data available that day, and the details on the report itself.

That's why many consumers spend time worrying about the wrong number. If you want a simple overview of what a score is and what it measures, this 24hourEDU credit score guide is a helpful primer before you dig into mortgage-specific scoring.

Practical rule: The score you should care about most is the one tied to the financing goal in front of you.

If you're trying to sort through conflicting numbers, start by learning how to DETERMINE YOUR TRUE CREDIT SCORE. That step alone can clear up a lot of unnecessary stress.

FICO vs VantageScore The Two Main Scoring Systems

Two names dominate most consumer conversations about credit scores: FICO and VantageScore. They both evaluate credit risk, but they aren't identical systems.

Two rulers measuring the same idea

Think of FICO and VantageScore as two brands of rulers. Both are trying to measure how risky a borrower may be. Both look at information from your credit reports. But they use different formulas, and those formula differences can produce different numbers.

That explains why a credit monitoring app can show one score while a lender sees another. The app may be showing a VantageScore or a different version of a scoring model than the lender uses. The score isn't fake. It's just built from a different formula for a different audience or purpose.

Here's the part that matters most for everyday borrowing decisions:

- FICO is the scoring system most lenders rely on for major lending decisions.

- VantageScore often appears in consumer apps and educational credit monitoring tools.

- Your goal matters. A score used for general monitoring isn't always the same score used for mortgage underwriting.

Why lenders usually lean toward FICO

For lending decisions, the market still leans heavily toward FICO. That doesn't make VantageScore useless. It means borrowers shouldn't assume the score they see for free is the score a mortgage lender will use.

FICO scoring is also built around five factors with specific weighting. Payment history carries 35%, amounts owed or utilization 30%, length of credit history 15%, new credit 10%, and credit mix 10%, according to the CFPB summary on what a credit score is. Those weightings help explain why recent late payments, collections, charge-offs, or heavy revolving balances can matter so much when you're preparing for a home loan.

If you want a more detailed look at how credit scores are evaluated, it helps to study the ingredients behind the score instead of staring at the final number alone.

Why Your Credit Score Changes From Place to Place

A score can change from one place to another even when nothing dramatic happened in your financial life. That's one of the most misunderstood parts of credit.

Different bureaus can hold different data

Your credit file doesn't live in one single master database. It exists across the major credit bureaus, and the information can vary from bureau to bureau. A creditor may report to one bureau, two bureaus, or all three. That means one report can show an account update that another report doesn't yet show.

Timing also matters. Credit scores are snapshots. If a card issuer reports a new balance today, your score tomorrow may look different than it did last week. If a late payment, collection, or charge-off appears on one bureau first, the scores based on that bureau can move before the others catch up.

Here are common reasons numbers don't match:

- Reporting differences. One bureau may have slightly different account history or balances.

- Score version differences. One company may use one version of a model while another uses a different version.

- Update timing. The report data may have changed between pulls.

A score is a ranking, not a life report card

The broader lending framework also helps explain score differences. The dominant benchmark in major U.S. lending remains the FICO score range of 300 to 850, and Equifax describes its score bands as 300 to 579 poor, 580 to 669 fair, 670 to 739 good, 740 to 799 very good, and 800 to 850 excellent in its guide to what a credit score is. That same source also notes that a credit score is more of a ranking than an absolute measure.

That idea matters. A score isn't a full judgment about your financial character. It's a sorting tool lenders use to place applicants into risk tiers.

Your score doesn't tell the whole story. It tells a lender where you rank within a scoring model built for a specific lending purpose.

So if one score says "good" and another is a bit lower or higher, that doesn't mean your credit identity changed overnight. It usually means the model, bureau data, or timing changed.

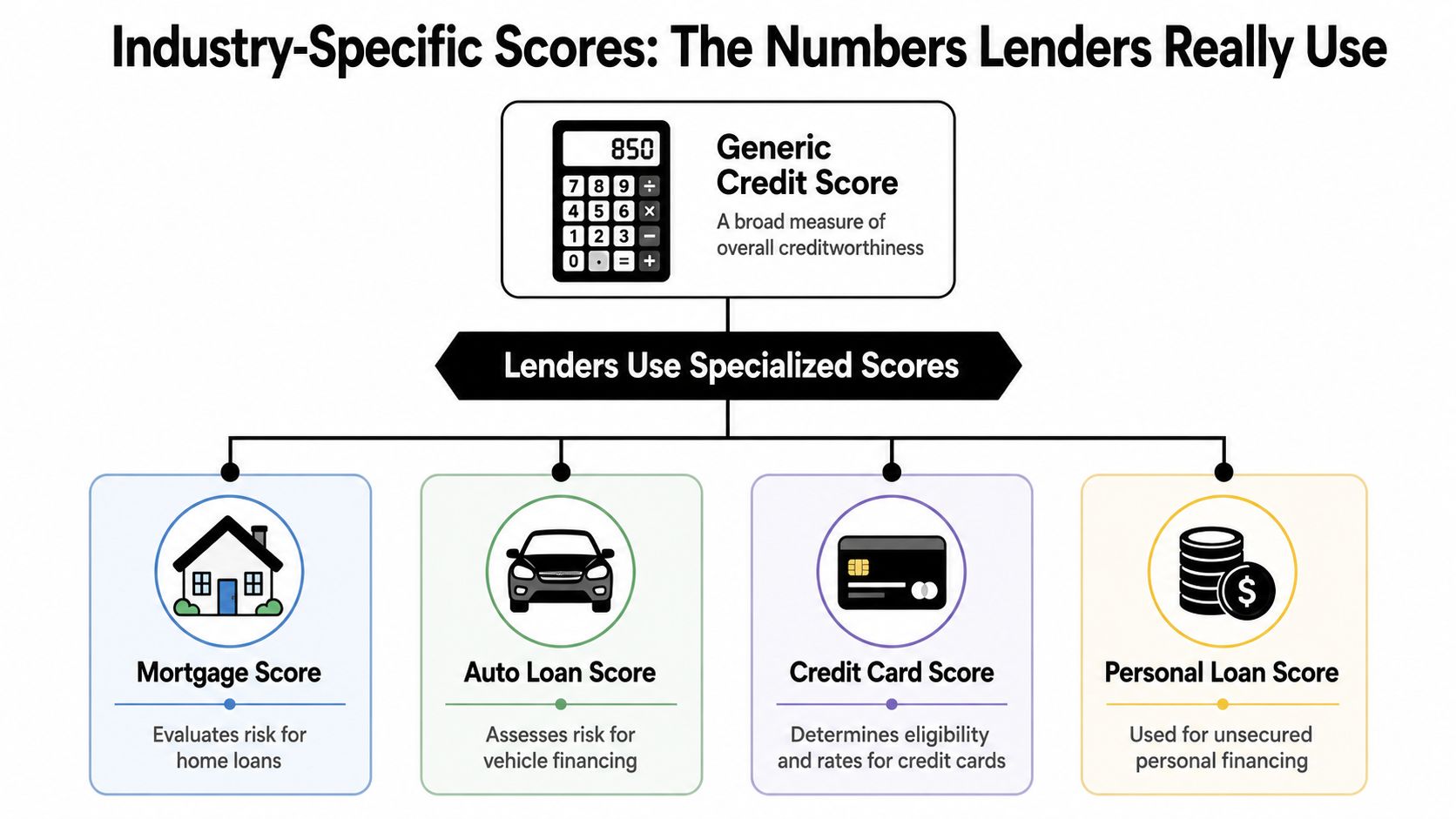

Industry-Specific Scores The Numbers Lenders Really Use

Most borrowers think in terms of a single credit score. Lenders usually don't.

A mortgage lender is not using a generic ruler

A lender isn't just asking, "Is this person generally creditworthy?" The lender is asking a more specific question. "How risky is this borrower for this exact product?"

That distinction is why mortgage lending, auto lending, credit cards, and personal loans can each rely on different scoring approaches. The practical question for a homebuyer isn't only which credit score matters. It's which scoring model and version the lender uses for the mortgage decision.

Experian highlights this point clearly in its discussion of which credit score is most important. Mortgage guidance often gets reduced to one target number, but both the score and the report details affect approval and pricing.

A simple comparison helps:

| Lending goal | What the lender cares about |

|---|---|

| Mortgage | Mortgage-specific score model and full report details |

| Auto loan | Auto-focused lending risk for vehicle financing |

| Credit card | Revolving credit behavior and card risk |

| Personal loan | Unsecured borrowing risk and overall file strength |

Why the report details still matter

A borrower can obsess over the score and miss the issue. The lender may be more concerned with what sits behind the score, such as recent late payments, a collection account, a charge-off, high revolving balances, or instability in the file.

That's why mortgage-readiness is different from score-watching. A consumer score on an app may look encouraging, but the lender may still pause because the report shows unresolved negative items or utilization that's too high for comfort.

For homebuyers trying to understand those risk points in plain English, this FICO score guidance for homebuyers can help connect score education with mortgage preparation.

How Mortgage Lenders Use Your Scores The Tri-Merge and Middle Score Rule

Mortgage underwriting is more methodical than most consumers realize. Lenders don't usually glance at one number and move on.

What tri-merge means in plain English

When you apply for a mortgage, the lender typically pulls credit information from all three major bureaus together. People often call this a tri-merge pull. The purpose is simple. The lender wants a broader view of your credit profile instead of relying on only one bureau's file.

That matters because bureau data can differ. One bureau may show a collection account that another doesn't. One may reflect a more recent balance update. Mortgage lenders want a fuller picture before making a lending decision.

How the middle score rule works

For a single borrower, lenders often focus on the middle of the three scores rather than the highest or lowest one. This helps avoid putting too much weight on an outlier.

For joint applications, the process becomes more personal and more important. Each borrower has a middle score identified, and underwriting generally focuses on the lower of those middle scores. That means one applicant's weaker credit profile can shape the qualification path for the household.

A few practical lessons come out of this:

- Consistency across bureaus matters because mortgage lenders review all three.

- Report accuracy matters because one incorrect negative item can affect one bureau more than the others.

- Preparation matters early because mortgage issues usually take time to review, document, and address.

Don't prepare for a mortgage by looking at one app score. Prepare by reviewing all bureau data and the mortgage-readiness issues behind it.

If you're comparing your profile against common FHA financing credit requirements, it helps to think beyond the headline score and look closely at collections, payment history, and revolving balances.

How to Improve the Score That Matters for Your Goal

Once you understand which score matters for your goal, your strategy gets clearer. You stop chasing every number you see and start working on the credit behaviors and report issues that lenders weigh.

Focus on the factors that carry the most weight

Because FICO is widely used in lending, it makes sense to focus on the factors that drive FICO scoring. The factor weightings listed earlier point to a practical order of operations.

Start with the areas that tend to move the needle most:

- Pay every bill on time. Payment history carries the largest weight in FICO scoring, so late payments can be especially damaging.

- Lower revolving balances. Amounts owed, often discussed as utilization, are also a major factor.

- Protect older accounts. Length of credit history can help support the file.

- Be careful with new applications. Too many new accounts or inquiries can work against mortgage timing.

- Use a healthy mix responsibly. Credit mix matters, but only when handled carefully and naturally.

Mortgage-readiness actions that usually matter most

For homebuyers, the score itself is only part of the file-strength conversation. The report has to be accurate, stable, and explainable.

A practical mortgage-readiness checklist looks like this:

- Review all three credit reports carefully for inaccurate, outdated, unverifiable, or misleading information.

- Address questionable negative items such as collections, charge-offs, or late payments through proper documentation and dispute processes where appropriate.

- Reduce credit card balances before applying so your reported utilization looks healthier.

- Avoid opening unnecessary new accounts close to a mortgage application.

- Watch emerging account types such as buy now pay later activity.

That last point deserves special attention. Fannie Mae said in 2024 it would consider BNPL obligations in automated underwriting only if they appear in the credit file, and FICO announced it would include buy-now-pay-later data in FICO Score 10 BNPL versions, as outlined in this FICO discussion of BNPL reporting changes. For borrowers with thin files or recent fintech usage, that means new credit behaviors may affect lending conversations more directly over time.

If you're building toward a stronger general profile, this Toya's guide to a 700 score offers practical consumer-level habits that complement mortgage preparation.

For people dealing with credit report errors, high utilization, collections, or late payment issues before buying a home, repair bad credit for home loans often starts with a documented file review and a realistic action plan. Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation to better understand your options. Results vary based on your credit file, documentation, creditor responses, account history, and current credit behavior.

Frequently Asked Questions About Credit Scores

If my free app shows a high score, am I guaranteed mortgage approval

No. Mortgage approval is never guaranteed.

A free app may show a score that isn't the same model a mortgage lender uses. Even if the number is strong, the lender still reviews the full credit report and other parts of the application. A file with high utilization, unresolved collections, recent late payments, or other underwriting concerns can still create problems.

Does closing an old credit card help my score

Often, it doesn't help. In many cases, it can make things harder.

Older accounts can support the age of your credit history. Closing a credit card can also reduce your available revolving credit, which may make your utilization look higher if balances remain on your other cards. If the card has no annual fee and doesn't create a management problem, many borrowers choose to keep it open and use it lightly.

A card you don't use much can still help your profile if it supports account age and available credit.

Do landlords use the same scores as mortgage lenders

Usually, no. Rental screening often uses a landlord's preferred screening system or a model designed for tenant review rather than mortgage underwriting.

That said, the report details still matter. A landlord may care about unpaid collections, eviction-related records, or signs that monthly obligations aren't being managed consistently. If you're preparing for apartment approval now and homeownership later, the same habits still help. Keep balances under control, pay on time, and review reports for errors.

Can buy now pay later accounts affect mortgage readiness

They can, depending on how they appear in the file and how the lender evaluates them.

BNPL activity confuses many borrowers because it doesn't always show up the same way across systems. But it has become more relevant in mainstream credit discussions. If you've used services like Affirm, Klarna, Afterpay, Sezzle, or similar products, don't assume they are invisible. Review your reports and ask how a lender will view those obligations in context.

What should I do before applying for a mortgage

Keep it simple and disciplined. Most borrowers benefit from the same core process:

- Pull and review your reports early so you have time to address inaccuracies or incomplete information.

- Bring late accounts current if possible and avoid adding new negative activity.

- Pay down revolving balances so your file looks more stable.

- Avoid unnecessary credit applications before underwriting.

- Ask the lender which scoring model they use instead of guessing from a free app.

If you've been denied before, don't assume the problem was only your score. Sometimes the barrier is a collection account, a charge-off, a reporting error, or unstable recent activity. A strong mortgage-readiness plan looks at the whole file.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

Superior Credit Repair provides educational support for consumers who want to understand their credit reports, dispute inaccurate or questionable reporting, and build a stronger credit profile before applying for financing. If you're preparing for a home loan, auto loan, apartment approval, or other major credit decision, you can explore Superior Credit Repair to learn more about the credit review and rebuilding process.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile. Leave feedback for Superior Credit Repair