You've saved for a down payment. Your income is steady. You may even know which neighborhoods fit your budget. Then you apply for a mortgage pre-approval, and the problem isn't your job or your savings. It's your credit file.

For many first-time buyers, the issue isn't terrible credit. It's not enough usable credit history, or a file that still shows old mistakes, disputed accounts, collections, charge-offs, or late payments that make an underwriter hesitate. That's where a starter credit card can help, if you use it the right way.

A Starter Credit Card isn't a magic fix. It won't erase negative items overnight, and it won't guarantee mortgage approval. What it can do is help you create a cleaner, more stable pattern of payment history that lenders can review. That matters because mortgage underwriting is built on patterns. Lenders want to see whether you handle credit consistently, whether balances stay controlled, and whether your file looks stable enough for a home loan.

That's one reason these accounts have become more important. The market for starter credit cards is projected to reach $790.3 billion by 2032, according to Allied Market Research's starter credit card market analysis. For future homebuyers, that growth reflects a simple reality. Many people need a safe first step into the credit system before they're ready for a mortgage.

Table of Contents

- Your First Step Toward Homeownership

- What Is a Starter Credit Card

- Comparing Types of First-Time Credit Accounts

- How Starter Cards Build Your Mortgage-Ready Credit

- A Homebuyers Roadmap Using a Starter Card

- Common Pitfalls That Can Delay Homeownership

- Upgrading Your Card and Preparing for a Credit Review

- Frequently Asked Questions

- Can a starter credit card help me qualify for a mortgage

- Is a secured card better than a regular beginner card for first-time homebuyers

- Should I leave a small balance on the card to help my credit

- How long should I keep a starter card open

- What if my credit report has errors while I'm trying to rebuild

Your First Step Toward Homeownership

A lot of future buyers reach the same frustrating point.

They've done the responsible things. They work full time. They pay rent on time. They've started saving. But when a lender looks at the file, the credit history is thin, old negatives still appear, or the current accounts don't show enough stable activity. On paper, the borrower may look unfinished.

A starter card can help fill that gap, but only if you treat it like a mortgage tool, not a shopping tool. Imagine it as laying the first row of bricks for a house. One brick doesn't build the home. It gives the structure something solid to start on.

Why first-time buyers often get confused

Many people assume the goal is just to get any credit card and use it often. That's where trouble starts. Mortgage lenders don't reward random activity. They look for clean, predictable account behavior.

They're asking practical questions:

- Does this person pay on time

- Do balances stay controlled

- Has the account been open long enough to show consistency

- Does the file look stable, or still risky

If you're planning for FHA loan preparation, VA loan preparation, USDA loan preparation, or conventional mortgage preparation, the answer usually isn't more credit. It's better-managed credit.

A starter card works best when it supports your long-term profile, not your short-term spending.

What this means for a homebuyer

For a first-time buyer, a starter card can serve three jobs at once:

- It establishes a record when your file is too thin.

- It shows current responsibility after past credit problems.

- It creates account stability that can help when a lender reviews your history.

That doesn't mean it fixes everything. If your reports contain credit report errors, inaccurate collections, outdated late payments, or misleading account statuses, those issues still need attention. Mortgage credit repair often involves both sides of the equation: building positive history and reviewing negative reporting for accuracy.

The right mindset is simple. Use the card to prove reliability, month after month, while you work on the rest of your credit profile in a structured, documented way.

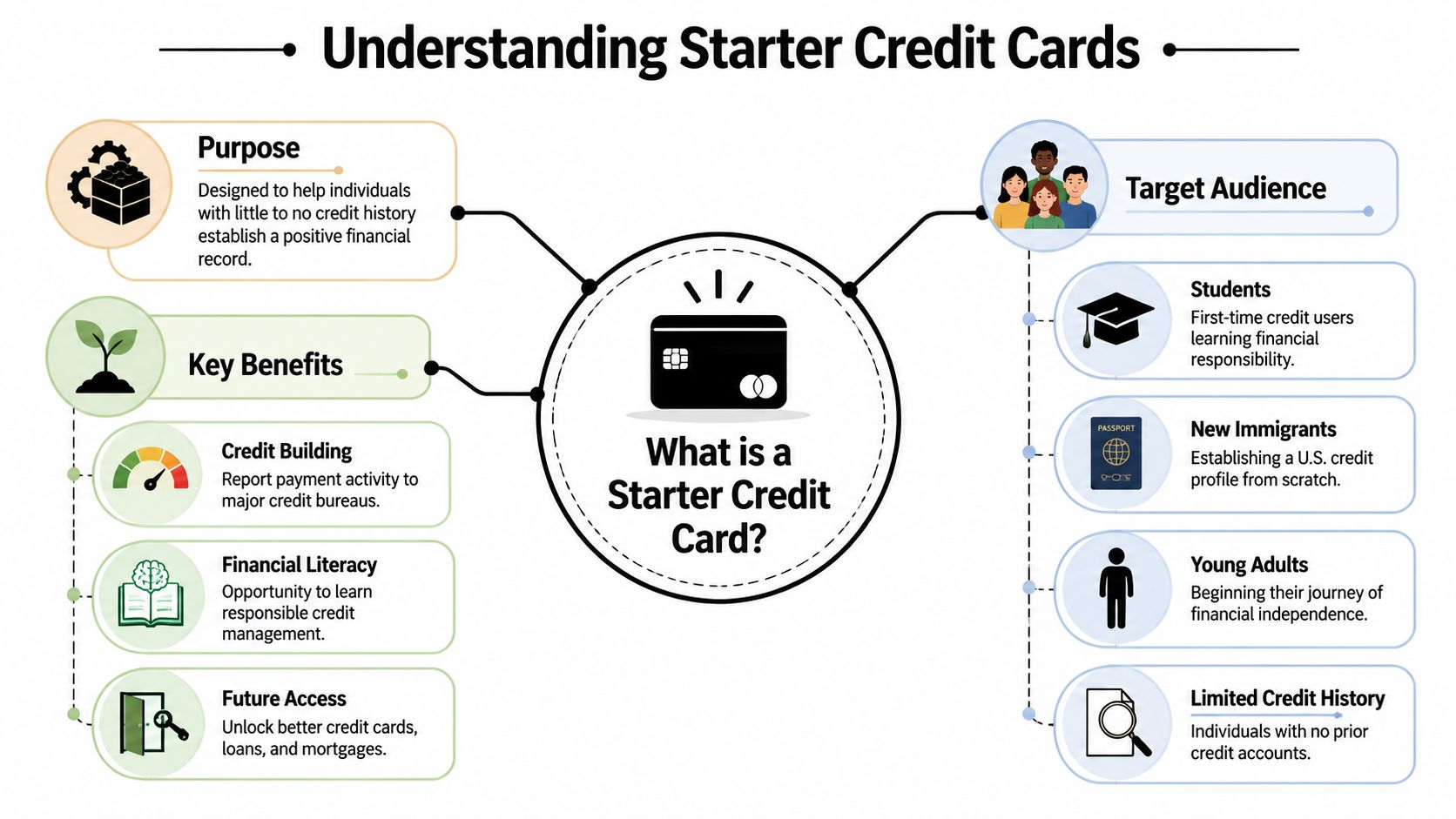

What Is a Starter Credit Card

A starter credit card is a card designed for people who are new to credit or rebuilding credit. That group includes students, young adults, new immigrants, and people recovering from financial hardship, divorce, medical collections, charge-offs, or prior delinquencies.

Who these cards are built for

The easiest way to understand a starter card is to compare it to a learner's permit. You're not getting full financial freedom. You're getting a basic tool that lets you demonstrate that you can follow the rules safely.

That's especially important for people with no score at all. According to the Federal Reserve Bank of Philadelphia's secured card market update, over 50% of all new secured starter cards are opened by consumers who do not have a credit score. That tells you something important. These cards are often the front door into the credit system.

Typical users include:

- A renter with no open revolving accounts who wants to prepare for buying a home

- A recent graduate with income but almost no established credit history

- A new immigrant building a U.S. credit profile from scratch

- A borrower rebuilding after hardship who needs to show current positive payment behavior

Why a starter card matters more than spending power

A lot of first-time users focus on the wrong thing. They ask, “How much can I spend?” A mortgage underwriter is asking, “What does this account say about how you manage debt?”

That's why the best use of a Starter Credit Card is often very boring. You open it, place a small planned purchase on it, pay it correctly, and repeat that pattern. The account becomes evidence.

Here's what a starter card is really for:

- Building payment history through steady on-time payments

- Showing restraint by keeping spending limited

- Creating account age so your file doesn't look brand new forever

- Supporting future financing such as auto loans, apartment approval, and eventually a mortgage

Practical rule: If you're using a starter card to impress yourself with available credit, you're using it wrong. If you're using it to impress a future underwriter with consistency, you're using it well.

For many buyers, this is the point where credit repair and credit restoration overlap with rebuilding. You may need to dispute negative accounts, remove inaccurate items where documentation supports a challenge, and also maintain a clean new account that shows current discipline.

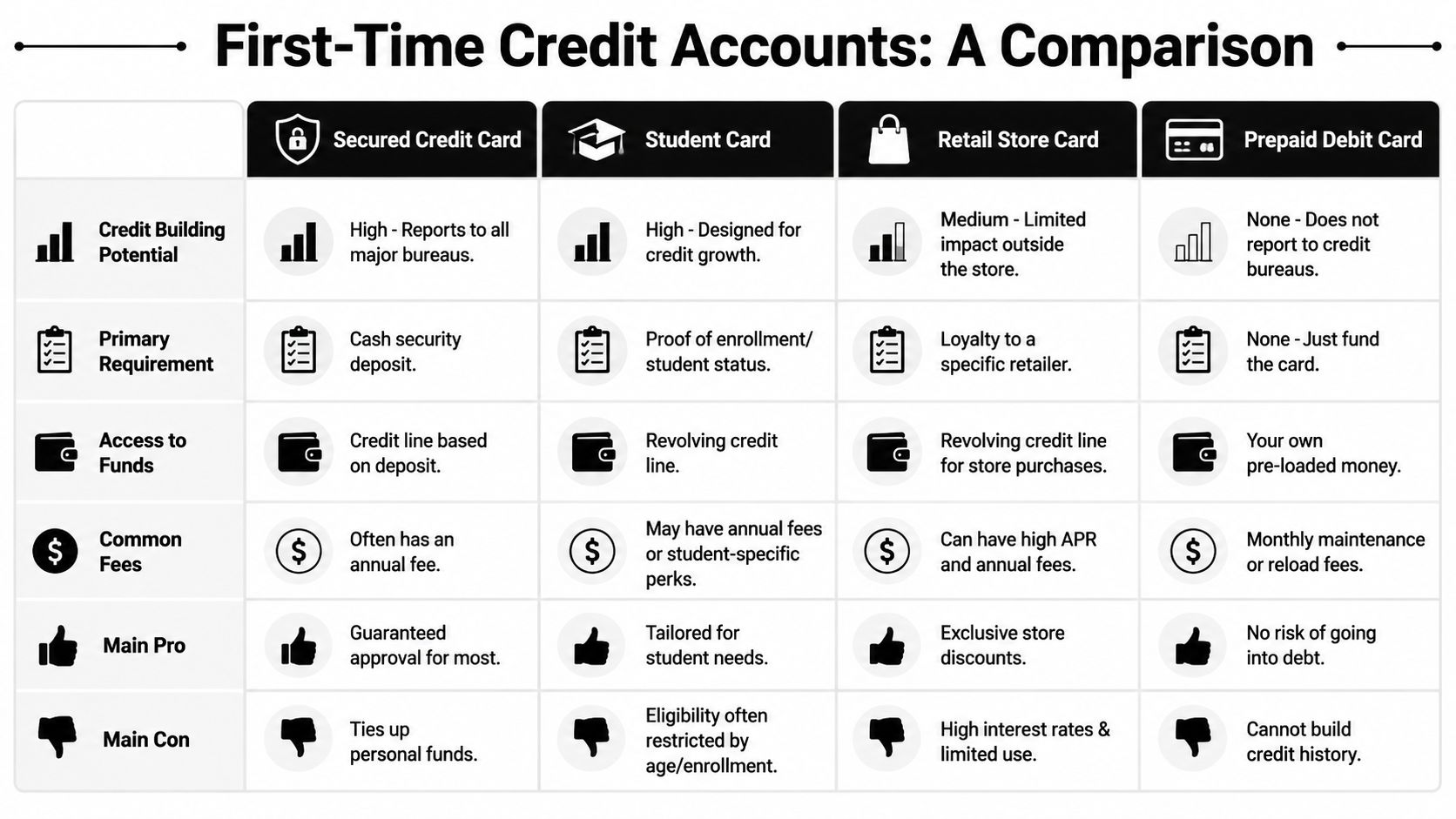

Comparing Types of First-Time Credit Accounts

Not every entry-level account helps a future mortgage applicant in the same way. Some accounts build stronger file quality. Others create activity without helping much. One type doesn't build credit at all.

A mortgage-focused comparison

The account types commonly considered are secured cards, student cards, retail store cards, and prepaid debit cards. Here's how they compare through a homebuyer's lens.

| Account Type | Best Use | Main Limitation for Homebuyers |

|---|---|---|

| Secured credit card | Strong option for thin or damaged files | Requires cash deposit |

| Student card | Useful if you qualify and need a first revolving line | Not available to everyone |

| Retail store card | Can add account activity | Limited usefulness and often less flexible |

| Prepaid debit card | Helps control spending | Does not build a credit profile |

A secured credit card is usually the clearest starting point for someone focused on mortgage readiness. The structure is simple. You put down a refundable deposit, often $200 to $500, and that deposit becomes your credit limit, as explained in Chime's overview of starter credit cards. The issuer reports your on-time activity to all three major bureaus, and consistent reporting over 6 to 12 months can help a thin-file user build a stronger profile.

A student card can also work well if you qualify. It may offer a normal revolving account without a deposit, but eligibility is narrower.

A retail store card can help some people begin building, but it often sends a weaker message for broad financial stability. It's tied to one store, one shopping environment, and sometimes encourages spending that doesn't help a mortgage plan.

A prepaid debit card isn't a credit-building tool. It's your own money loaded onto a payment card. That can be helpful for budgeting, but it doesn't create the type of revolving credit history mortgage lenders usually want to review.

Which option usually gives the clearest signal to lenders

For most first-time buyers, the secured card is easier to control because the limit starts small and the purpose is obvious. You're not trying to finance a lifestyle. You're building a record.

That's one reason secured cards fit well into a broader plan for rebuilding credit for mortgage readiness. The account gives you something current and measurable while you address other file issues, such as collections dispute help, late payment dispute help, charge-off dispute help, or medical collection credit repair where reporting appears inaccurate, outdated, unverifiable, or misleading.

Use this decision guide:

- Choose a secured card if your file is thin, bruised, or inconsistent.

- Choose a student card if you qualify and can manage it conservatively.

- Be cautious with retail cards if your goal is lender-ready credit profiles.

- Don't mistake prepaid cards for credit tools because they won't help build the record a mortgage lender reviews.

How Starter Cards Build Your Mortgage-Ready Credit

A starter card helps because it creates a repeating pattern that gets reported. Every month, the card issuer sends account information to the major credit bureaus. That information becomes part of the record lenders use when they evaluate your application.

Think of your credit profile as a financial resume. A starter card gives you a place to add fresh entries. Each on-time month says, “This borrower handled credit as agreed.”

Your financial resume starts with reporting

The most useful parts of a starter card for mortgage purposes are simple:

- Payment history shows whether you pay as agreed

- Balance management shows whether you rely too heavily on available credit

- Account stability shows whether the relationship lasts over time

Those points matter because mortgage lending is not just about one score on one day. Lenders study the structure of the file behind the score. A thin file with one clean revolving account often looks more understandable than a file with scattered inquiries, erratic balances, and little history.

If you're not sure which credit score matters for mortgages, that question matters too, because the score you see in an app may not be the same score a mortgage lender uses. That's why behavior matters more than chasing a number on a screen.

What underwriters notice in a thin credit file

Underwriters tend to notice what your file suggests about habits.

A well-managed starter card can suggest:

- Routine and control

- Predictable payment behavior

- Low dependence on revolving debt

- A willingness to build slowly instead of borrowing aggressively

A poorly managed starter card can suggest the opposite. If the balance is high, the payment is late, or the account is brand new and already stressed, the account can weaken your mortgage timing rather than help it.

The card itself doesn't build trust. Your repeated behavior on the card builds trust.

This is also where credit repair for homebuyers becomes more practical than promotional. If the rest of your report contains credit report errors, inaccurate derogatory accounts, or questionable statuses, positive card history can help, but it doesn't replace the need to review and challenge problems through a legal, documentation-based process.

For people preparing for FHA approval, VA loans, or conventional mortgage approval, a starter card is often one part of a broader lender-readiness strategy. The card creates positive data. Your report review addresses the negative or inaccurate data. Together, those steps can improve the quality of the file, though results always vary based on the account history, documentation, creditor responses, and your current behavior.

A Homebuyers Roadmap Using a Starter Card

The most common advice says to keep utilization below a certain threshold. That advice isn't completely wrong, but it can miss an important mortgage detail. For future homebuyers, what gets reported may matter more than what you think you're “keeping low.”

According to NerdWallet's discussion of first credit card strategy, mortgage lenders often view any reported balance on a starter card negatively, even though many general credit tips focus on staying under a utilization guideline. For FHA and VA readiness, borrowers who consistently report a $0 balance can look stronger.

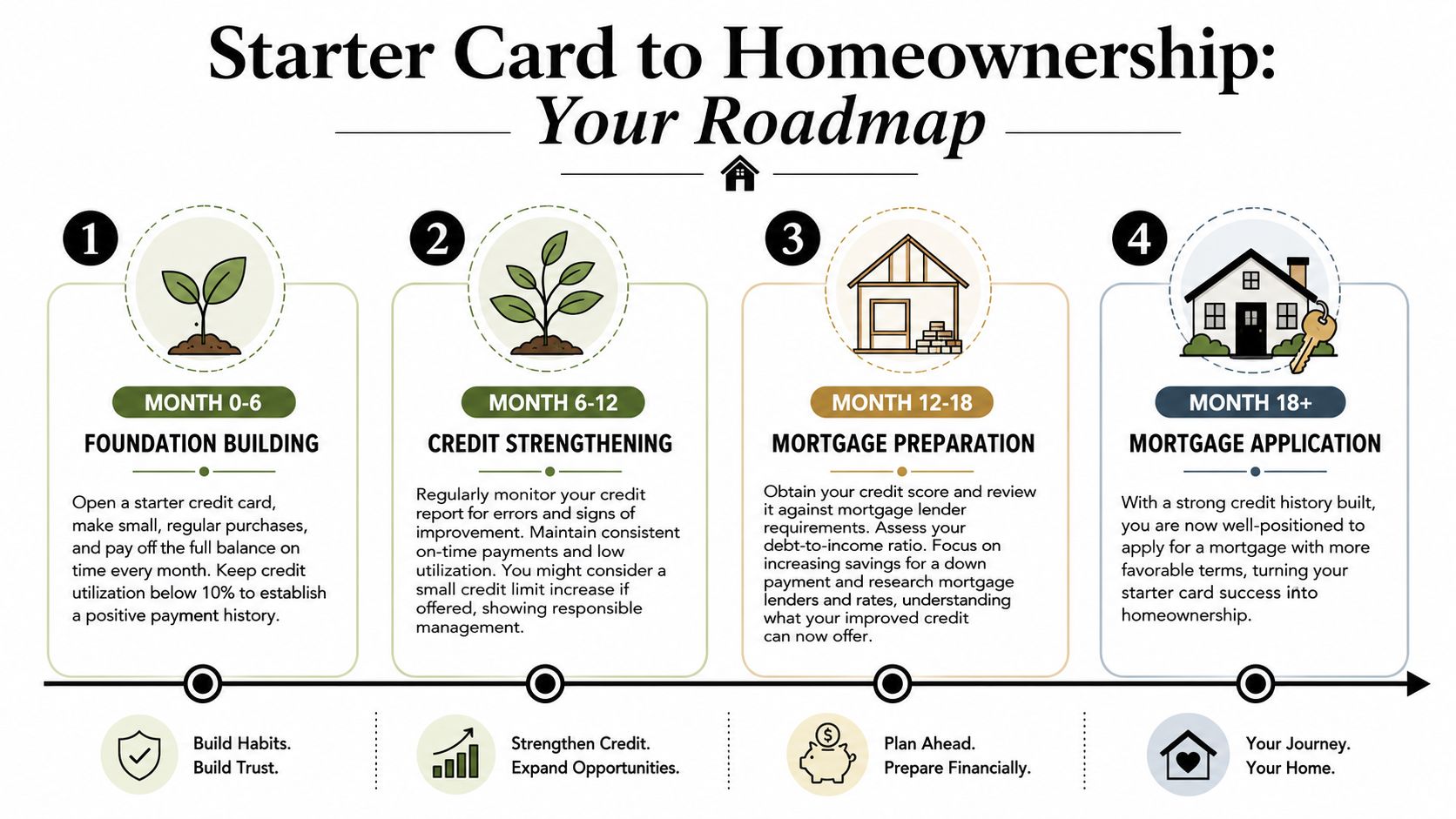

First phase building clean history

Many buyers make a useful adjustment. They use the card, but they don't let a balance remain on the statement if the mortgage goal is approaching.

A practical roadmap looks like this:

Open one starter card and keep activity small

Use it for one planned bill, such as a streaming service, gas purchase, or phone accessory you could pay for with cash anyway.Pay before the statement closing date when possible

That increases the chances the issuer reports a zero balance instead of a live balance.Never miss the due date

A starter card is too small an account to create a major positive effect quickly, but a late payment can create an outsized negative effect.Monitor your reports for accuracy

If the account reports incorrectly, fix that early.

Mortgage mindset: Use the card enough to create history, but not in a way that makes you look dependent on it.

Second phase preparing for lender review

As the account matures, you're no longer just building a score. You're preparing for underwriting.

Here are the milestones that matter most:

At 6 months

You want a clean pattern of on-time payments and no reporting surprises.At 12 months

You want the account to look stable and boring in the best possible way. Stable accounts often help far more than flashy rewards accounts with messy usage.At 18 months

You want your file to look seasoned enough that a lender sees consistency, not recent scrambling.

For homebuyers, score targets matter too. Conventional loans typically require a minimum credit score of 620, while FHA loans may approve applicants with scores as low as 580 with 3.5% down or 500 with 10% down, according to Total Mortgage's first-time homebuyer qualifications guide. A starter card alone won't guarantee those outcomes, but it can support the credit habits that help you move toward them.

That's also why it helps to understand broader mortgage lender requirements. Your score matters, but so do payment history, collections before mortgage approval, debt-to-income concerns, and overall file stability.

Common Pitfalls That Can Delay Homeownership

Small accounts can create big problems when they're handled carelessly. A starter card is supposed to strengthen your file. Used poorly, it can make an underwriter ask harder questions.

Mistakes that look bigger to mortgage lenders

Some errors are common because people think the account is “just a starter card,” so the consequences must be small. Underwriters don't see it that way.

Watch for these problems:

Late payments

One missed due date can damage the clean pattern you were trying to establish. If you want a clearer sense of the impact of late payments on credit, it helps to understand that mortgage lenders often care about recency, frequency, and whether the issue suggests current instability.High reported balances

A small card with a high balance can make a thin file look strained.Opening too many new accounts

Multiple applications can make it look like you're chasing credit instead of managing it.Closing the card too early

If the account is your main source of positive revolving history, shutting it down can reduce file stability.

When one small account creates a bigger problem

A starter card should never operate in isolation from your mortgage plan. If you're about to apply for a home loan, every account decision should support lender confidence.

That includes avoiding behavior that creates last-minute underwriting concerns, such as new debt, unexplained spending changes, or payment issues. For a broader legal and transaction-level perspective, Greiner Law Corp's mortgage insights offer useful reminders about mistakes buyers make during the mortgage process that can affect approval timing.

Here's the larger lesson. A home loan file is judged as a whole. Your starter card can help show control, or it can become one more sign that your finances are still unsettled. Keep the account quiet, current, and predictable.

Upgrading Your Card and Preparing for a Credit Review

A starter card isn't supposed to be your final destination. For many borrowers, it's a bridge account. You use it to establish control, then move into a more mature credit profile without losing the history you worked to build.

When to move from secured to unsecured

The ideal upgrade window is typically 12 to 18 months, according to Bankrate's guide to building credit with starter cards. If the issuer allows you to convert from a secured card to an unsecured one without a new application, that can help preserve the account's age.

That matters because age supports stability. A long-running account can make your file look more established than a brand-new replacement account.

This step is also becoming more relevant as other reporting factors enter lender conversations, including BNPL activity. If you're using installment-style payment apps alongside a starter card, your file can become harder to read unless everything is managed carefully. Mortgage underwriters usually prefer a profile that looks steady and easy to interpret.

Why a final review matters before you apply

Once you've built positive history, the next question is simple. Does the rest of your report still contain problems that could hold you back?

A structured credit review can help identify:

- Inaccurate collections

- Outdated derogatory items

- Unverifiable negative accounts

- Misleading payment histories

- Identity theft issues or mixed-file problems

- Open balances and account statuses that need clarification before underwriting

Credit repair, mortgage credit repair, and long-term rebuilding converge. Positive habits matter. So does report accuracy. If a file still contains questionable negative items, dispute negative accounts only where facts, records, and legal dispute rights support the challenge. Results vary, and no ethical company should promise guaranteed deletions or guaranteed approval.

If identity theft has affected your file, you may also need a specialized process such as Superior Credit Repair for identity theft victims, because fraud-related reporting often requires separate documentation and careful follow-up.

Frequently Asked Questions

Can a starter credit card help me qualify for a mortgage

It can help support your mortgage readiness, but it doesn't guarantee approval. A starter card can add positive payment history and account stability. Lenders still review the full file, including collections, late payments, charge-offs, debt-to-income concerns, and overall report accuracy.

Is a secured card better than a regular beginner card for first-time homebuyers

For many homebuyers, yes. A secured card is often easier to obtain when your file is thin or damaged, and it can provide a clearer, more controlled way to build positive revolving history. The best option depends on your current report, budget, and ability to manage the account carefully.

Should I leave a small balance on the card to help my credit

Not if your main goal is mortgage readiness. General credit advice often focuses on keeping balances low, but a mortgage-focused approach is often stricter. Reporting a $0 balance can be more favorable for a thin file when a home purchase is the goal.

How long should I keep a starter card open

In many cases, long enough to build stable history and possibly transition to an unsecured account without losing the age of the account. If you close it too soon, you may weaken one of the very patterns you were trying to establish.

What if my credit report has errors while I'm trying to rebuild

Then the rebuilding plan should include a report review. Positive account history helps, but inaccurate, outdated, unverifiable, or misleading items can still interfere with financing. That's where a documentation-based credit repair process may be appropriate.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. If you're preparing for FHA, VA, USDA, or conventional mortgage financing, the team can help you understand how credit report accuracy, utilization, collections, charge-offs, late payments, and account stability may affect lender readiness. You can request a free credit analysis or consultation through Superior Credit Repair to better understand your options. Results vary based on your credit file, documentation, creditor responses, account history, and current credit behavior.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile. Leave feedback for Superior Credit Repair