You may be looking at Tacoma rents, watching home prices stay out of reach, and wondering if rent to own is the one path that finally gets you closer to owning a place of your own. Maybe your income is steady, but your credit report still has old late payments, collections, high balances, or accounts you don't fully understand. That combination is common. It also creates a problem many real estate sites gloss over.

A rent-to-own deal can give you time. It does not guarantee that you'll be able to buy the home at the end.

That's the part people need to understand before they sign anything. In Tacoma, where affordability pressure is real and many renters want a practical bridge into ownership, the lease period has to be treated like a preparation window. If you don't use that time to become mortgage-ready, the contract can turn into an expensive detour instead of a path forward.

Table of Contents

- Is a Rent-to-Own Home in Tacoma Right for You?

- Understanding Rent-to-Own Contracts in Washington State

- The Reality of the Tacoma Housing Market for RTO Buyers

- Weighing the Benefits and Risks of Rent-to-Own

- A Safer Path to Pursuing a Rent-to-Own Opportunity

- Using Your Lease Period to Become Mortgage-Ready

- Frequently Asked Questions About Rent-to-Own Homes

Is a Rent-to-Own Home in Tacoma Right for You?

A common Tacoma story goes like this. A renter has a decent job, pays rent on time, and wants stability for their family. They start browsing homes, then hit a wall. The payment looks higher than expected, the down payment feels far away, and a lender points out credit issues that need work before FHA, VA, USDA, or conventional mortgage approval is realistic.

That's where rent to own homes in Tacoma start to look appealing. Instead of buying today, you move in as a tenant first and work toward buying later. On paper, that sounds like breathing room.

But the right question isn't just, “Can I get into the house?” The better question is, “Can I qualify to buy it before the lease ends?”

For some households, the answer may be yes. A rent-to-own arrangement can make sense if your income is stable, your credit problems are identifiable, and you're willing to use the lease period to clean up your credit report, lower revolving balances, handle collections, and build a lender-ready file. If you need nearby regional support while comparing options, some readers also look at Help with bad credit in Seattle for broader Puget Sound guidance.

Signs the idea may fit your situation

- You're close, but not quite mortgage-ready. Maybe your score isn't where a lender wants it, or old charge-offs and late payments still need attention.

- You need time to document stability. Lenders often look for consistent payment behavior, not just good intentions.

- You want to test the home first. Living in the property can reveal commute issues, repair concerns, or neighborhood realities that don't show up in a listing.

Signs you should slow down

- You can't comfortably handle higher housing costs. Many contracts cost more than a standard lease.

- You haven't reviewed your credit reports yet. Going in blind is risky.

- You're being pushed to sign quickly. Pressure usually benefits the seller, not the buyer.

Practical rule: If a rent-to-own contract doesn't come with a clear plan for mortgage readiness, it's incomplete from the buyer's side.

A rent-to-own home isn't automatically good or bad. It's a tool. Used carefully, it can create a bridge. Used casually, it can lock you into a deadline your credit file can't meet.

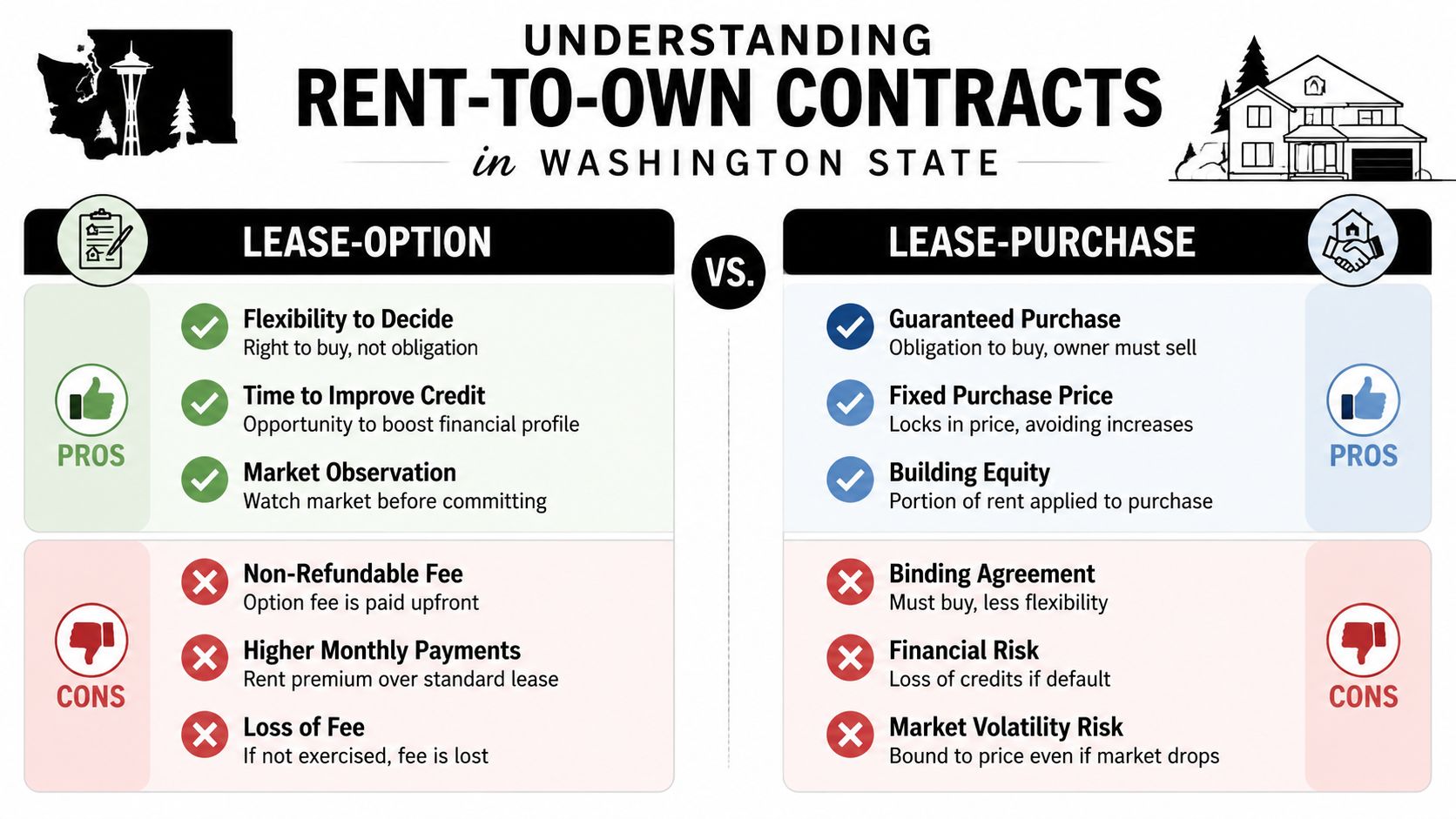

Understanding Rent-to-Own Contracts in Washington State

A Tacoma renter signs what looks like a simple path to ownership. Two years later, the lease ends, the mortgage application is denied, and the deal falls apart over credit issues that were never addressed clearly at the start. That outcome is common enough to shape how you should read the contract.

Washington buyers need to know what kind of agreement they are signing, what deadlines control the deal, and what credit standards they will still need to meet later. A rent-to-own contract is not just a housing agreement. It is also a financing deadline with paperwork attached.

The contract type changes your risk

A lease-option agreement gives you the right to buy the home later. You can usually choose not to buy if the financing does not work out or the property no longer fits your needs. That flexibility matters when your credit profile still needs work.

A lease-purchase agreement usually commits both sides to a future sale. In plain English, you are agreeing ahead of time that you will buy the house at the end of the lease. If your mortgage is denied, the contract can leave you in a much harder position.

That difference sounds small on paper. It is not small in practice.

A lease-option gives you time to prepare. A lease-purchase can put legal pressure on you before a lender has approved anything. If your credit file has late payments, high card balances, old collections, or reporting errors, that distinction deserves close attention.

A good starting point is learning your consumer rights in credit repair before you sign. If future mortgage approval depends on the accuracy of your credit reports, dispute history, and payment behavior during the lease, those rights matter on day one.

The terms that deserve the closest reading

Rent-to-own agreements often use familiar words in unfamiliar ways. Sellers, agents, and buyers may all say “rent credit” or “purchase price,” but the contract language controls what those terms mean.

Here are the clauses to read slowly:

| Contract term | Plain-English meaning | Why it matters |

|---|---|---|

| Option fee | Money paid for the right to buy later | The agreement should say whether any of it is refundable and under what conditions |

| Rent credit | A portion of rent may count toward the purchase | The contract should explain the amount, when it accrues, and whether you lose it if the deal fails |

| Purchase price | The future sale price or pricing formula | You need to know whether the price is fixed now or determined later |

| Lease term | The period before you must buy, renew, or walk away | Your credit repair and mortgage timeline have to fit inside this window |

| Default | What counts as breaking the agreement | Late rent, missed deadlines, or other violations may cancel your buying rights |

Rent credits work like a coupon with fine print. They only have value if the agreement clearly explains how they are earned, tracked, and applied.

Credit terms matter as much as housing terms

This is the part many real estate articles skip. The contract may describe the home in detail while saying very little about the buyer's path to mortgage approval. That gap causes trouble later.

Look for answers to questions such as:

- What credit score range are you likely to need by the end of the lease?

- How much time do you have to fix reporting errors or lower revolving debt?

- Does the contract give you enough time to show a full pattern of on-time payments?

- What happens if financing is denied because of credit, debt-to-income ratio, or underwriting issues?

If the agreement is silent on those risks, you still carry them.

Before signing, read every clause covering maintenance, repairs, tax responsibility, insurance, default, notices, extension options, and financing deadlines. Ask for the full agreement early. If possible, have a Washington real estate attorney review it. A rent-to-own contract can be useful, but only if the legal terms and your mortgage readiness plan point to the same finish line.

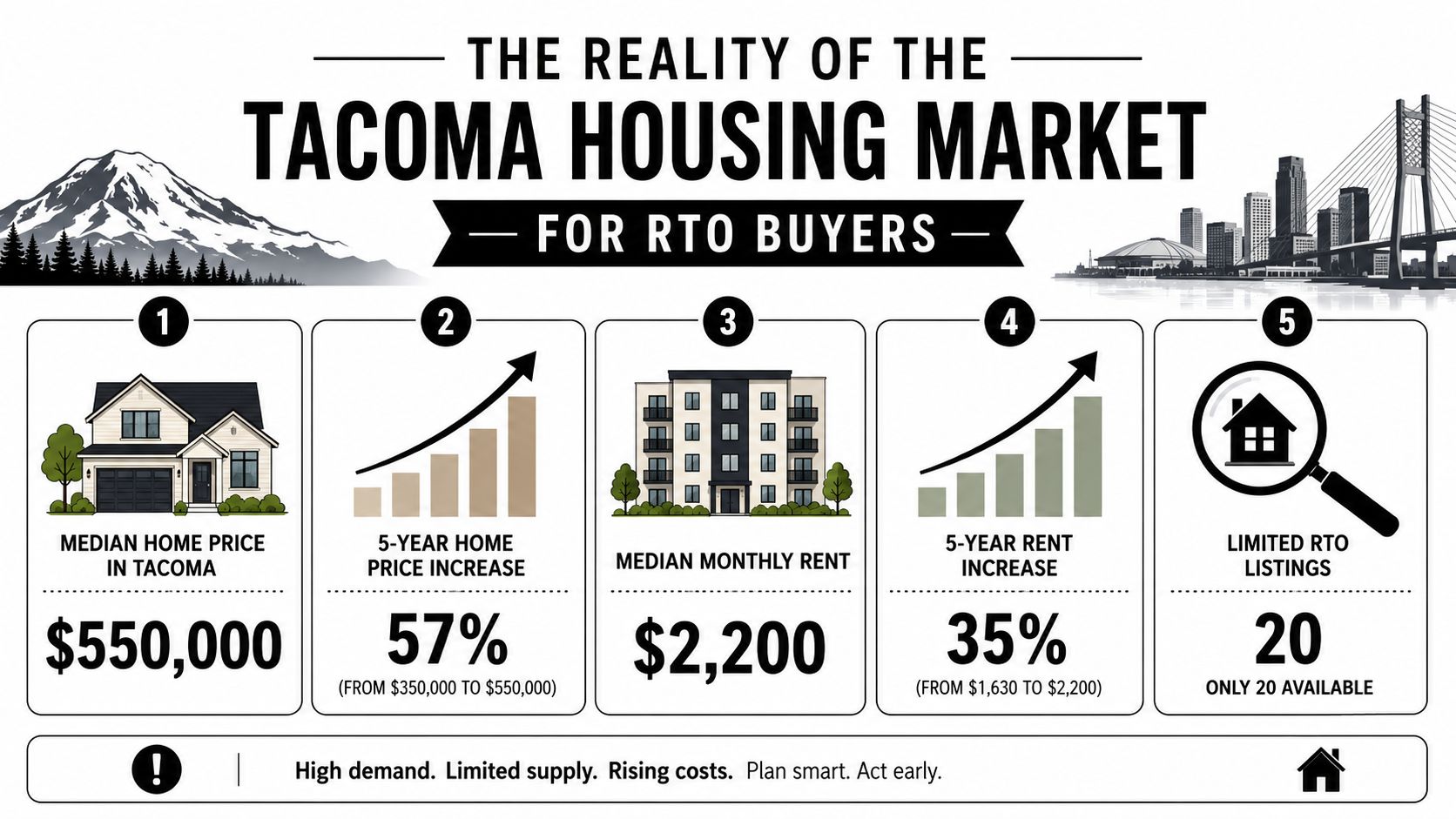

The Reality of the Tacoma Housing Market for RTO Buyers

Rent to own gets more attention when regular homebuying feels harder. Tacoma fits that pattern. Buyers aren't just comparing lease options with homeownership in theory. They're comparing them against a local market that has become harder to enter.

Why Tacoma renters look at rent to own

The City of Tacoma's housing baseline shows that in 2023, the average home price in Tacoma was $460,000, and 50% of Tacoma households were renters. The same report states that since 2015, housing costs rose 135% while median incomes rose 59%, which has created a severe affordability problem for renters trying to become owners (Tacoma housing baseline report).

That helps explain why rent-to-own homes in Tacoma attract attention. A household may not be ready to buy today, but they don't want to keep waiting without a plan. Rent to own looks like a middle lane between renting forever and buying before you're prepared.

Why sellers still screen hard

Some people think rent to own means “no credit standards.” In practice, that's often wrong. Tacoma-area listings frequently market to buyers with credit challenges, but many still ask for a minimum credit score, stable gross income relative to rent, clean rental history, and no eviction or bankruptcy history. The same local information also notes that contract terms vary widely, especially around maintenance duties, how rent credits work, and whether the deal is optional or mandatory to complete (local Tacoma RTO market examples).

That matters because a seller is still taking risk. Even if they're flexible, they usually want signs that the tenant-buyer has a realistic chance of qualifying later.

Here's the practical takeaway for self-assessment:

- Income stability matters. A seller may tolerate imperfect credit more than unstable income.

- Rental history matters. Repeated late housing payments can weaken trust quickly.

- The contract type matters. A lease-purchase deal can be dangerous if your financing outlook is uncertain.

- Mortgage readiness still matters. Rent to own delays the mortgage decision. It doesn't erase it.

If you're trying to judge whether your file is close to lender standards, this guide for first-time homebuyers can help you understand what mortgage lenders usually review before approval.

A seller may let you move in with credit issues. A mortgage lender at the end of the lease may not.

That's why local market pressure and credit preparation have to be looked at together. In Tacoma, affordability is the reason many people explore rent to own. Mortgage qualification is the reason many deals still fail.

Weighing the Benefits and Risks of Rent-to-Own

A Tacoma renter signs a rent-to-own deal believing the hard part is getting into the house. Two years later, the harder test arrives. A mortgage lender reviews the credit file, debt, income, and the home appraisal. If those pieces do not line up, the lease can end without a closing.

That is the central tradeoff.

Rent to own can give you time. Time is valuable only if you use it with a plan. The lease period works like a practice season before the championship game. The final game is mortgage approval, and many rent-to-own deals fail there, not because the home was unavailable, but because the buyer never became finance-ready.

Where rent to own can help

The benefit is breathing room. You may have time to clean up credit errors, lower card balances, build on-time payment history, save cash, and learn whether the property fits your life.

That testing period matters more than many buyers expect.

Living in the home first can reveal issues that photos and a quick showing miss. You learn the commute, traffic pattern, noise level, school route, and day-to-day upkeep. Before taking on any repair duties, review essential home inspection tips for buyers so you know what problems can turn a hopeful deal into a costly one.

A rent-to-own term can also help buyers whose credit is bruised but improving. Late payments, collections, charge-offs, and high utilization do not always block homeownership forever. They do mean you need a clear schedule for fixing what a lender will review later. Good credit advice for mortgage approval can help you judge whether your lease period is long enough for the work ahead.

Where people get hurt

The biggest risk is losing time and money while still ending up unapproved for a mortgage.

As noted earlier, many rent-to-own agreements require upfront option money that may not be refundable. If your credit, debt, income, or the property appraisal creates a problem at the end of the lease, that money may be gone even if you made every rent payment on time.

Several risks are easy to miss at the start:

- Repair duties can shift early. Some contracts make the tenant-buyer pay for maintenance or larger repairs before ownership transfers.

- The future price can work against you. If the agreed price is higher than the home appraises for later, your lender may finance less than you expected.

- Deadlines matter. Missing a notice date, payment rule, or financing deadline can cancel your purchase rights.

- Credit problems stay active until you address them. A lease does not cause scores to rise on its own.

- Income changes can derail the plan. A job loss, reduced hours, or new debt can hurt mortgage qualification even if your credit improves.

One common point of confusion is this: rent payment history and mortgage readiness are not the same thing. Paying rent on time helps show housing stability. A lender will still examine your debt-to-income ratio, recent late payments, account balances, reserves, and whether the home supports the loan amount.

Here is the practical balance:

| Potential benefit | Matching risk |

|---|---|

| More time before applying for a mortgage | Time can pass without enough credit progress |

| A chance to live in the home before buying | You may take on repair costs without ownership |

| Some predictability if the purchase terms are set | The later appraisal or loan approval may not support the deal |

| Room to save and organize finances | Upfront option money may be lost if you cannot close |

A safe way to judge a rent-to-own offer is to ask one question first. By the end of the lease, will your file look stronger to a mortgage lender than it does today? If the answer is unclear, the contract may be giving you hope without giving you enough runway.

A Safer Path to Pursuing a Rent-to-Own Opportunity

The safest way to approach rent to own is to act like you're preparing for two transactions at once. First, you're entering a lease. Second, you're preparing for a future mortgage and purchase. Both need protection.

The protective steps that come first

Start with your credit file before you fall in love with a house. Pull your reports, identify collections, charge-offs, late payments, disputed balances, and high utilization. If mortgage approval is your end goal, early credit advice for mortgage approval can help you see whether the lease period is long enough for your situation.

Then examine the property itself. An inspection matters even if you aren't closing right away, because some rent-to-own contracts shift repair responsibility to the tenant. A practical checklist of essential home inspection tips for buyers can help you spot issues that turn an appealing house into an expensive obligation.

A careful process usually includes:

- Review your full credit picture. Don't rely on a score alone.

- Read the contract type closely. Know whether it's optional or mandatory.

- Vet the property condition. Deferred maintenance can become your problem.

- Verify ownership and seller authority. You need confidence that the person signing can legally sell.

- Have a Washington real estate attorney review the agreement. This step protects you from vague or one-sided terms.

Why paperwork and recording matter

One of the most overlooked risks is what happens after signing. According to Century 21 Northwest's discussion of the process, Washington Law Help requires filing the rent-to-own agreement with the County Auditor's office to protect the buyer, and failed transactions can stem from unrecorded agreements that leave tenant-buyers exposed to eviction and loss of equity expectations (Washington rent-to-own process guidance).

That's not a technical detail. It's buyer protection.

If an agreement isn't properly handled, the tenant may believe they're steadily moving toward ownership while the legal paperwork doesn't protect that belief in a meaningful way. That's why informal deals, handshake promises, and “we'll sort it out later” language are dangerous.

If a rent-to-own agreement isn't reviewed, clarified, and properly recorded, you may be taking on homebuyer risk without homebuyer protection.

A safer path is slower. That's a good thing. Fast deals often hide weak paperwork, unclear repair duties, missing disclosures, or unrealistic assumptions about future financing.

Using Your Lease Period to Become Mortgage-Ready

The lease period is the most important part of the entire strategy. It isn't dead time. It's your chance to turn a shaky application into a stronger mortgage file.

Many local rent-to-own discussions skip that point. Yet local guidance notes that many applicants still fail to get a mortgage because unresolved credit issues remain on their reports, and many low-income borrowers have negative items that can block standard loan approval if those problems aren't addressed during the lease term (mortgage-readiness gap in Tacoma RTO guidance).

Treat the lease like a mortgage preparation plan

If your goal is to buy the home at the end, treat every month of the lease as a step toward that closing. That means your financial behavior during the lease should look more like a future homeowner than a regular renter.

Start with your reports. Look for inaccurate, outdated, unverifiable, or misleading information. If an account balance is wrong, a collection doesn't belong to you, dates are inconsistent, or account status reporting appears questionable, that needs attention early. A structured credit repair and credit restoration process can help identify items that may be challenged through documentation-based disputes.

Then focus on current behavior. Mortgage lenders often care about recent payment history, revolving utilization, unresolved collections, and overall file stability. If your cards are close to their limits, reducing balances may help your profile look less stressed. If you've had recent late payments, stopping the pattern matters more than chasing shortcuts.

What future lenders will usually care about

Different loan programs can review risk differently, but some themes are common across FHA, VA, USDA, and conventional mortgage preparation.

- Payment history: Recent on-time payments show control and consistency.

- Collections and charge-offs: These can raise questions about unresolved debt and file cleanliness.

- Credit utilization: High balances can signal strain even when payments are current.

- Debt-to-income pressure: Your monthly obligations affect how much mortgage payment you can realistically carry.

- Stability: Lenders often want a file that looks settled, not chaotic.

If debt obligations are part of the problem, learning how to improve your debt to income ratio can make the lease period more productive. Stronger debt management won't guarantee mortgage approval, but it can improve how affordable a future loan appears on paper.

Here's a practical lease-period checklist:

| During the lease | Why it matters later |

|---|---|

| Review all three credit reports | You need to catch errors and problem accounts early |

| Dispute inaccurate negative items | Mortgage decisions rely on report accuracy |

| Pay every account on time | Recent history carries weight |

| Lower revolving balances where possible | High utilization can weaken approval readiness |

| Avoid unnecessary new debt | New obligations can hurt affordability |

| Check in with a lender before the lease ends | You need time to correct issues before the deadline |

Another smart move is studying avoiding common homebuyer pitfalls so you don't spend the lease period improving one part of your file while accidentally creating a new lending problem somewhere else.

A rent-to-own contract doesn't replace mortgage preparation. It gives you a deadline for it.

People often ask whether credit repair before buying a home is really necessary if they're already in the property. The answer is often yes. Occupancy doesn't equal approval. You still need a lender-ready credit profile, documented income, manageable debt, and a file that supports the loan program you plan to use.

Results vary, of course. Some borrowers mainly need to remove inaccurate items and lower utilization. Others need a longer rebuilding plan because of charge-offs, medical collections, repossessions, thin credit, or recent hardship. The key is honest timing. If your lease is short and your file is severely damaged, you need to know that early, not in the final month.

Frequently Asked Questions About Rent-to-Own Homes

Who pays for repairs and property taxes in a rent-to-own home

It depends on the contract. Some rent-to-own agreements place more repair responsibility on the tenant-buyer than a standard lease would. Others keep more duties with the owner until closing. Don't assume the seller handles maintenance just because you're still renting. The contract should clearly state who pays for repairs, taxes, insurance, and routine upkeep.

What if the home is worth less than the contract price later

That can create financing problems. If the agreed purchase price is higher than the home's later appraised value, a lender may not approve the loan structure you expected. In plain terms, the numbers may stop working even if you want the house. That's one reason independent review, inspection, and legal guidance matter before signing.

Can you use a first-time homebuyer program with rent to own

Sometimes, but it depends on the program rules and your full mortgage profile at the time you apply. A rent-to-own agreement doesn't automatically block first-time homebuyer assistance, but it also doesn't guarantee eligibility. Ask a lender and housing counselor early so you understand whether your future purchase plan aligns with program requirements.

Should you check your credit during the lease period

Yes. This is one of the most important parts of the process. Consumer Reports notes that approximately 13% of consumers have credit report errors that directly impact their credit scores, and those errors can prevent mortgage approval or lead to higher interest rates (Consumer Reports on credit report errors).

That means credit review shouldn't happen once and then disappear. It should happen before signing, during the lease, and well before your mortgage application window opens.

What if I have collections, late payments, or charge-offs

That doesn't automatically mean a rent-to-own plan is impossible. It does mean you should be realistic. Negative items can affect FHA loan preparation, VA loan preparation, conventional mortgage preparation, apartment approval, and refinance options. The goal is to identify inaccurate or questionable reporting, address what can be disputed through proper documentation, and build stronger recent credit habits going forward.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. If you're considering a rent-to-own home in Tacoma or preparing for FHA, VA, USDA, or conventional mortgage approval, you can request a free credit analysis or consultation through Superior Credit Repair to better understand your options. Results vary based on your credit file, documentation, creditor responses, account history, and current credit behavior.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile. https://share.google/ePRpFvtCXwCjiJwOK