A lot of people find out they have a credit report problem at the worst possible moment. They've found the house, talked to the lender, and started imagining the move. Then a mortgage pre-approval slows down because TransUnion is showing a collection account, charge-off, or personal detail that looks wrong. It might be an old balance that should read differently, an account that doesn't belong to them, or a reporting issue that now affects FHA, VA, USDA, or conventional loan preparation.

That kind of surprise feels personal, but it's also common. Credit reports are built from data furnished by many companies, and mistakes happen. When they do, accuracy matters because lenders don't evaluate hopes or explanations. They evaluate the report in front of them. If you're trying to buy a home, refinance, qualify for an apartment, or clean up your file before applying for financing, a dispute has to be handled carefully and documented well.

Many consumers search for the TransUnion mailing address for dispute and assume there's one simple answer. That's where confusion starts. Different addresses are tied to different mailing methods, and using the wrong one can slow down a case that already feels urgent. For a homebuyer, that delay can matter. Mortgage underwriting moves on deadlines, and credit report accuracy often sits right in the middle of those deadlines.

A strong dispute process is less about emotion and more about precision. That includes using the right address, the right mailing method, the right documents, and the right wording. It also helps to understand how lenders look at score ranges and report quality while you're working through corrections. If you want extra context on how score tiers are often viewed during the homebuying process, HomeReadyCalc's guide to credit scores gives a useful broad overview, and Superior Credit Repair on loan credit scores explains which scores often matter in lending decisions.

Table of Contents

- Introduction Why Your Credit Report Accuracy Matters for a Mortgage

- The Strategic Advantage of Disputing by Mail

- The Definitive Guide to TransUnion's Mailing Addresses

- How to Write an Effective TransUnion Dispute Letter

- Assembling Your Complete Dispute Packet Checklist

- What to Expect After You Mail Your Dispute

- Frequently Asked Questions About TransUnion Disputes

Introduction Why Your Credit Report Accuracy Matters for a Mortgage

A family can do almost everything right and still get tripped up by one inaccurate tradeline.

One of the most stressful versions of this shows up during pre-approval. A lender pulls credit and sees an account the borrower doesn't recognize, a balance that appears overstated, or a late payment history that doesn't match the borrower's records. The loan officer doesn't have the authority to fix TransUnion's file. The borrower has to address the reporting issue directly, and timing suddenly matters.

For mortgage credit repair, the goal isn't to chase shortcuts. The goal is to make the report accurate, document the issue well, and avoid procedural mistakes that create more delay. That matters whether someone is preparing for an FHA loan, reviewing old medical collections, dealing with a charge-off dispute, or trying to rebuild credit profile stability after hardship.

Why homebuyers feel this more sharply

A homebuyer usually isn't disputing in a vacuum. They're also managing loan estimate deadlines, earnest money concerns, rate lock discussions, debt-to-income questions, and requests for updated documents. If a credit report error sits in the middle of that, it can affect how the lender views overall file stability.

A clean and accurate report won't guarantee approval, but an inaccurate report can absolutely complicate an approval review.

That's why the mailing address issue matters more than it seems. If a dispute letter goes to the wrong place, the consumer may lose valuable time while the file is sorted internally or treated as a general inquiry instead of a formal dispute.

Accuracy protects more than your score

People often say they want to improve credit score, but lenders look beyond a single number. They also review account status, recent derogatory activity, utilization patterns, collections, and consistency across the report. An incorrect account can raise questions about repayment behavior even when the underlying information is wrong.

That's especially important for:

- First-time homebuyers who need a lender-ready credit profile before underwriting

- VA and FHA applicants who are already working within program guidelines

- Renters preparing to buy who can't afford avoidable delays

- Families rebuilding after hardship who need credit report errors corrected without adding confusion

The practical answer is straightforward. Send the dispute the right way the first time, keep proof, and make every document easy to review.

The Strategic Advantage of Disputing by Mail

A borrower can lose a week just by mailing a solid dispute packet to the wrong TransUnion address.

That happens more often than it should. Consumers see Chester, PA in one place, Chicago, IL in another, and assume either address will work. In practice, mailing method affects routing. If you are trying to correct a report before underwriting moves on your file, that distinction matters.

Online disputes have their place. A mailed dispute is usually the better choice when the issue is tied to mortgage timing, a collection, a reported late payment, mixed file concerns, or any error that needs documents and a clear explanation. Mail gives you control over what TransUnion receives, how the dispute is framed, and what proof you keep for your own records.

Why paper still matters in mortgage preparation

Under the Fair Credit Reporting Act, disputes follow a deadline-driven process. That timeline only helps if the dispute reaches the correct department and includes enough documentation to be reviewed efficiently.

Mail creates a record you can use.

You have a dated letter, copies of supporting documents, proof of mailing, and delivery confirmation if you send it by certified mail. If your loan officer asks what was disputed, when it was sent, or whether you included backup, you can answer with documents instead of a summary from memory.

That matters for another reason. Mortgage files often move between a loan officer, processor, underwriter, and sometimes a credit vendor. Clear records reduce confusion. They also make it easier to show that you disputed a specific reporting error in good faith and on a specific date.

What mail does better than a quick online dispute

Mail works best when the issue needs context.

A portal may be enough for a simple personal-information correction. It is less useful when you need to explain why an account is not yours, why a balance is outdated, why a collection should show paid, or why a reported delinquency conflicts with your records. A written packet lets you organize that explanation in a way an investigator can follow.

Mailed disputes are usually the stronger option for:

- Multiple inaccurate items. One letter can address each account in a clean, numbered format.

- Document-heavy disputes. Statements, payoff letters, court papers, identity theft reports, and creditor correspondence are easier to present as one packet.

- Time-sensitive mortgage files. Certified mail gives you a mailing receipt and delivery trail that can help if your lender asks for evidence.

- Second-round disputes. If a prior dispute did not fix the error, a new packet with added documents often carries more weight than resubmitting a short online form.

The trade-off is simple. Mail takes more effort up front, but it reduces preventable mistakes later.

Practical rule: If the disputed item could affect underwriting, send a written dispute with copies of your evidence and keep proof of delivery.

Mail does not guarantee deletion or correction. No method does. Furnisher records, account history, and the quality of your documents still drive the outcome. But from a compliance and documentation standpoint, mail puts you in a stronger position, especially before a home purchase, where a delay caused by a routing error or an incomplete dispute can cost more than the postage.

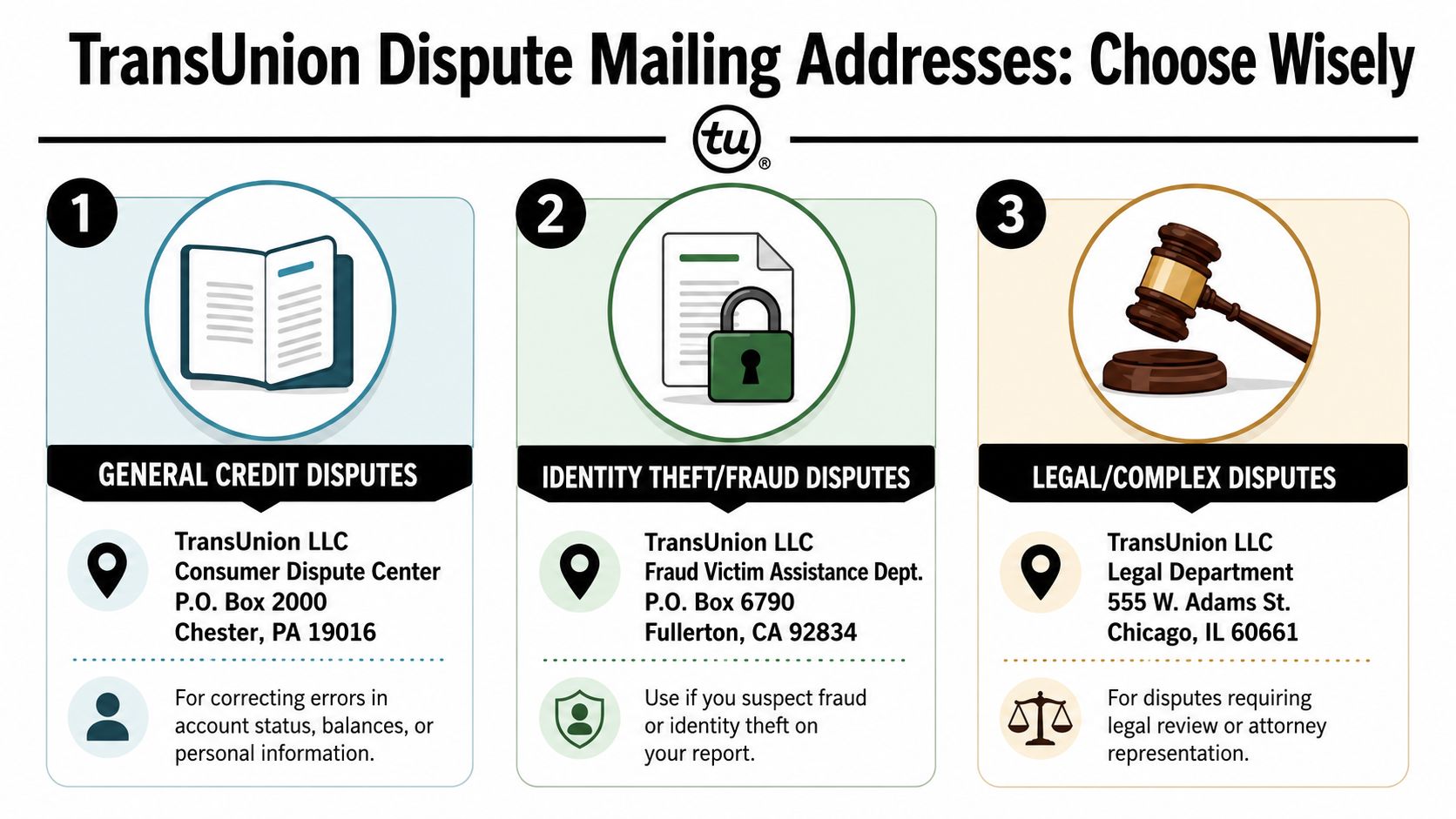

The Definitive Guide to TransUnion's Mailing Addresses

A homebuyer sends a dispute packet by overnight courier to the Chicago P.O. Box, then waits for an update that never comes. A week later, the lender is still waiting too. I see this confusion often because TransUnion's addresses are repeated online without explaining the delivery method behind each one.

The short version is simple. Chicago and Chester are both used for TransUnion disputes, but they are not interchangeable. The address you use should match the way the packet is being delivered. If you mix the method and the address, you increase the chance of delay at the worst possible time, especially during mortgage underwriting.

Use Chicago for certified mail disputes

If you are sending a dispute through the U.S. Postal Service by certified mail, use:

TransUnion LLC

Attn: Consumer Relations

P.O. Box 2000

Chicago, IL 60601

This is the address many consumers should use because certified mail creates a clear paper trail. That matters when a lender, loan officer, or underwriter asks for proof that the dispute was sent and delivered.

The practical benefit is documentation, not speed. Certified mail usually gives you the strongest record if a mortgage file is under review.

Use Chester for overnight courier delivery

If you are sending the packet by overnight courier, use:

TransUnion LLC

Consumer Dispute Department

P.O. Box 2000

Chester, PA 19016

ATTN: Consumer Dispute

Use the department line exactly as shown. That small detail can affect where the package lands internally.

This is the point that gets misreported. Consumers often find the Chicago address first and use it for every shipment, including FedEx or UPS. That is where preventable delay starts. If the package is going by courier, use Chester. If it is going by certified mail through USPS, use Chicago.

The Credit People also distinguishes TransUnion dispute contact details in its overview of TransUnion dispute contact information.

| Mailing method | Department line | Address to use |

|---|---|---|

| Certified mail | Attn: Consumer Relations | P.O. Box 2000, Chicago, IL 60601 |

| Overnight courier | ATTN: Consumer Dispute | P.O. Box 2000, Chester, PA 19016 |

Match the address to the delivery method you are using, not to the version you saw first in a search result.

Wilmington applies to non-US disputes

For international disputes or non-US callers, the documented address is:

P.O. Box 2000

Wilmington, DE 19801

This can matter for military families overseas, expatriates, or anyone handling a dispute from outside the United States. A domestic mailing route may not be the right fit for those cases.

If your packet includes several exhibits, account statements, or legal paperwork, organize it carefully before mailing. Clean labeling helps avoid confusion on both sides, and tools focused on streamlining legal document review can help you check that your attachments are readable, complete, and consistent. If you also need help drafting the actual dispute language, this guide on how to dispute inaccurate credit report items pairs well with the address rules above.

For standard consumer disputes, the mailing rule is straightforward. Certified mail goes to Chicago. Overnight courier goes to Chester. International disputes go to Wilmington.

How to Write an Effective TransUnion Dispute Letter

A good dispute letter is calm, specific, and easy to verify. It doesn't need dramatic language. It needs clean facts.

That means you should identify the account, explain what is inaccurate, and attach documents that support your position. If you're trying to dispute inaccurate credit report items, this guide on how to dispute inaccurate credit report items is a helpful companion to the mailing instructions covered here.

What to include in the body of your letter

Keep the structure simple:

Your identifying information

Include your full name, current address, date of birth, and the report details needed to locate your file.A direct statement of purpose

State that you are disputing specific items on your TransUnion credit report and requesting reinvestigation.One paragraph for each disputed item

Name the creditor or furnisher, list the account reference as shown on the report, and explain the issue in plain language.A list of enclosures

Mention the documents you are including, such as your ID, proof of address, statements, or a copy of the report with the item highlighted.A request for written results

Ask for the outcome in writing and keep your tone professional.

Here is a clean example of the kind of wording that works:

I am writing to dispute the accuracy of certain information on my TransUnion credit report. Please reinvestigate the items identified below. I have enclosed copies of supporting documents and a copy of my credit report with the disputed entries marked.

For each item, be specific:

Account name: ABC Collections

Reason for dispute: This account is not mine. Please investigate and remove or correct this item if it cannot be verified as accurate.

Or:

Account name: XYZ Bank

Reason for dispute: The balance reported appears inaccurate based on the enclosed account records. Please review and update the reported balance as appropriate.

If you want help polishing wording before mailing, some consumers find value in tools that assist with document clarity. For example, resources focused on streamlining legal document review can help you spot confusing phrasing before you send anything.

What not to write

Don't turn the letter into a life story. TransUnion doesn't need the full background of your hardship to evaluate a factual reporting issue.

Avoid these common mistakes:

- Emotional appeals. “This ruined my life” may be true to your experience, but it doesn't help establish inaccuracy.

- Mixed admissions. Don't say “This might be mine, but I'm not sure, and I also don't owe it.” That weakens the dispute.

- Vague complaints. “Please fix my credit” is not a dispute reason.

- Irrelevant attachments. If a document doesn't prove identity, address, or the specific reporting issue, leave it out.

A useful standard is this. If a lender, underwriter, or compliance reviewer read your letter, would they understand the exact error and the exact evidence supporting your position within a few minutes? If the answer is yes, you're on the right track.

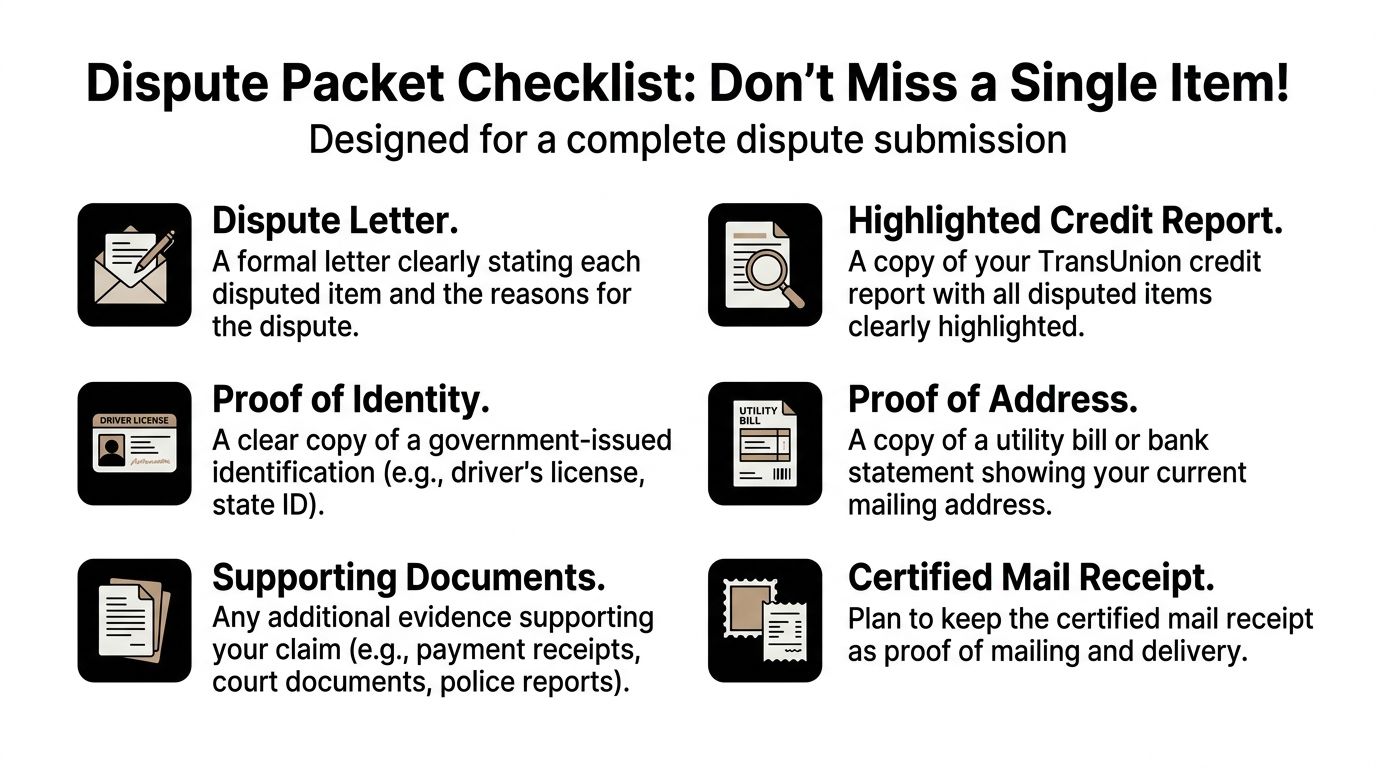

Assembling Your Complete Dispute Packet Checklist

A strong letter helps, but the packet is what makes the dispute reviewable.

Missing documents create avoidable problems. The bureau has to confirm identity, connect the dispute to the right file, and understand exactly what item is being challenged. If any of that is unclear, the dispute can slow down or come back asking for more information.

The documents that belong in the envelope

Before you seal the envelope, make sure these items are included:

- Signed dispute letter. This is the core of the packet. It identifies the disputed items and states why they are inaccurate, outdated, unverifiable, or misleading.

- Copy of your TransUnion credit report. Highlight or circle each item you are disputing so there's no confusion about what needs to be reviewed.

- Proof of identity. A copy of a government-issued ID helps confirm that the dispute is tied to the correct consumer file.

- Proof of current address. A recent utility bill or bank statement supports the mailing address you list in the letter.

- Supporting records. Include only the documents that help prove your position, such as account statements, payoff records, police reports, court papers, or creditor correspondence.

- Mailing receipt record. Keep this for your own file once the packet is sent.

If the issue involves collections, especially accounts you believe should be validated or challenged carefully before mortgage review, it also helps to understand how to dispute collection letters effectively.

How to package and mail it correctly

Don't send originals. Send legible copies.

Use a clean stack order so the reviewer sees your letter first, then the report, then your ID and proof of address, then the supporting records. That order makes the packet easier to process.

A practical mailing routine looks like this:

- Make a full copy first. Keep an exact copy of everything you send.

- Label the envelope carefully. Match the address and department line to the mailing method you chose.

- Use certified mail with return receipt when mailing through USPS. That gives you better proof of mailing and delivery.

- File the receipts together. Keep the dispute letter copy, mailing receipt, and delivery confirmation in one folder.

A dispute packet should read like a clean file, not a pile of papers.

That discipline helps with homebuyer timelines because if a lender asks what has been done, you'll have an organized record instead of trying to recreate the process from memory.

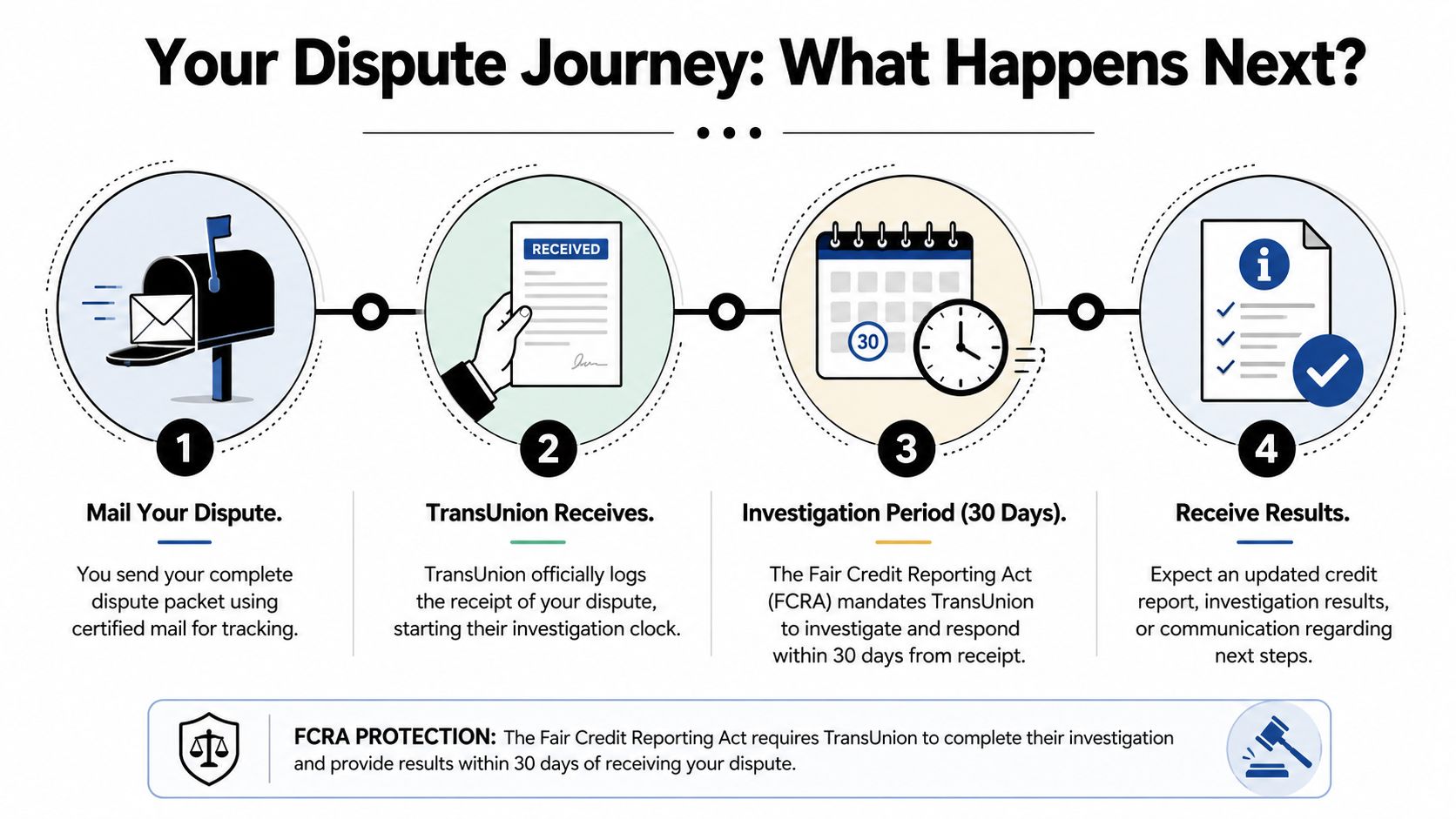

What to Expect After You Mail Your Dispute

A common mortgage problem starts here. You mailed the dispute, tracking shows it was delivered, and now your lender wants an update before the next underwriting review. At that point, the best move is usually simple: confirm delivery, keep your file organized, and wait for the written result instead of sending duplicate letters that can slow the process.

The timeline and the response

Once TransUnion receives a properly routed dispute, the investigation usually follows a defined review window under federal law. If you send more information during the investigation, that review period can extend. For a broader sense of how these timelines tend to play out, see understanding credit repair results.

Delivery matters more than many consumers realize.

If you used the right address and mailing method earlier in the process, you have already reduced one of the most common causes of delay. I regularly see confusion between the Chester, PA mailing address and the Chicago, IL street address. That mix-up can cost time, especially for borrowers working against an appraisal, rate-lock, or underwriting deadline. After mailing, the goal is to verify that the packet reached the correct intake channel and then let the investigation run its course.

TransUnion generally responds by mail. The response may explain what was investigated, whether any item was changed, deleted, or left as reported, and whether an updated report was issued.

While you wait, keep your actions tight and documented:

- Confirm delivery status with your mailing receipt or tracking record.

- Watch your mail closely for a written investigation result.

- Keep your lender updated with documents such as proof of mailing, delivery confirmation, and any written response.

- Avoid filing the same dispute again immediately unless TransUnion clearly did not receive or process the first one.

If the result doesn't resolve the issue

A completed investigation is not always a favorable one. An account can come back as verified even when you still believe the reporting is wrong.

Read the response carefully. Compare it to the exact issue you raised and the documents you sent. In practice, I look for three things first: whether TransUnion addressed the correct tradeline, whether the result answers the actual dispute reason, and whether the furnisher appears to have reviewed the supporting records.

If the response misses the point, a follow-up dispute may still be appropriate, but it should be better, not just louder. Add missing evidence, tighten the explanation, and correct any ambiguity in the first letter. Repeating the same argument with the same packet usually does not improve the result.

For homebuyers under contract, calm documentation helps. Tell your lender what was sent, when it was delivered, what came back, and what the next step is. Clear records tend to help more than verbal summaries or optimistic guesses.

Frequently Asked Questions About TransUnion Disputes

Is it better to dispute online, by phone, or by mail

For high-stakes issues, mail is usually the most defensible option because it creates a stronger paper trail and lets you control the supporting documents. Online disputes can be useful for very simple errors. Phone disputes are usually the weakest choice when the issue may affect a mortgage, apartment approval, or a major financing decision.

What if TransUnion says the account is accurate and I still disagree

Read the response carefully and compare it to what you originally submitted. If you have new documents or a clearer explanation, a follow-up dispute may be appropriate. If the issue still isn't resolved, you may also consider adding a consumer statement to your file, depending on the situation.

Will mailing a dispute delay my mortgage application

It can affect timing, but unresolved inaccuracies can affect a mortgage application too. For many homebuyers, especially those preparing for FHA, VA, USDA, or conventional loan review, a documented correction process is better than leaving a disputed item unaddressed. Keep your lender informed and give them documentation, not verbal summaries.

Should I dispute every negative account on my report at once

Not always. A stronger strategy is usually to dispute items that are clearly inaccurate, outdated, unverifiable, or misleading, and to support each one with documents. Flooding the file with weak or poorly documented disputes can create confusion instead of progress.

Can I get help understanding what to dispute first

Yes. Many consumers need help deciding whether the underlying issue is a collection, a late payment, a charge-off, utilization, mixed personal information, or overall file stability before applying for financing. If you want more practical guidance beyond this article, these answers for your credit questions can help you sort through common situations.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation through Superior Credit Repair to better understand your options. Results vary based on your credit file, supporting documentation, creditor responses, account history, and current credit behavior.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile. Share your experience on Google