Separate what can be challenged from what must be rebuilt

Buying a home in Roswell, Georgia can feel exciting, but credit questions can make the process feel uncertain. Many buyers are not sure whether collections, late payments, charge-offs, medical bills, high credit card balances, old accounts, or reporting errors will affect a mortgage conversation. A home loan credit report review gives you a structured way to look at the information before a lender is reviewing it under pressure.

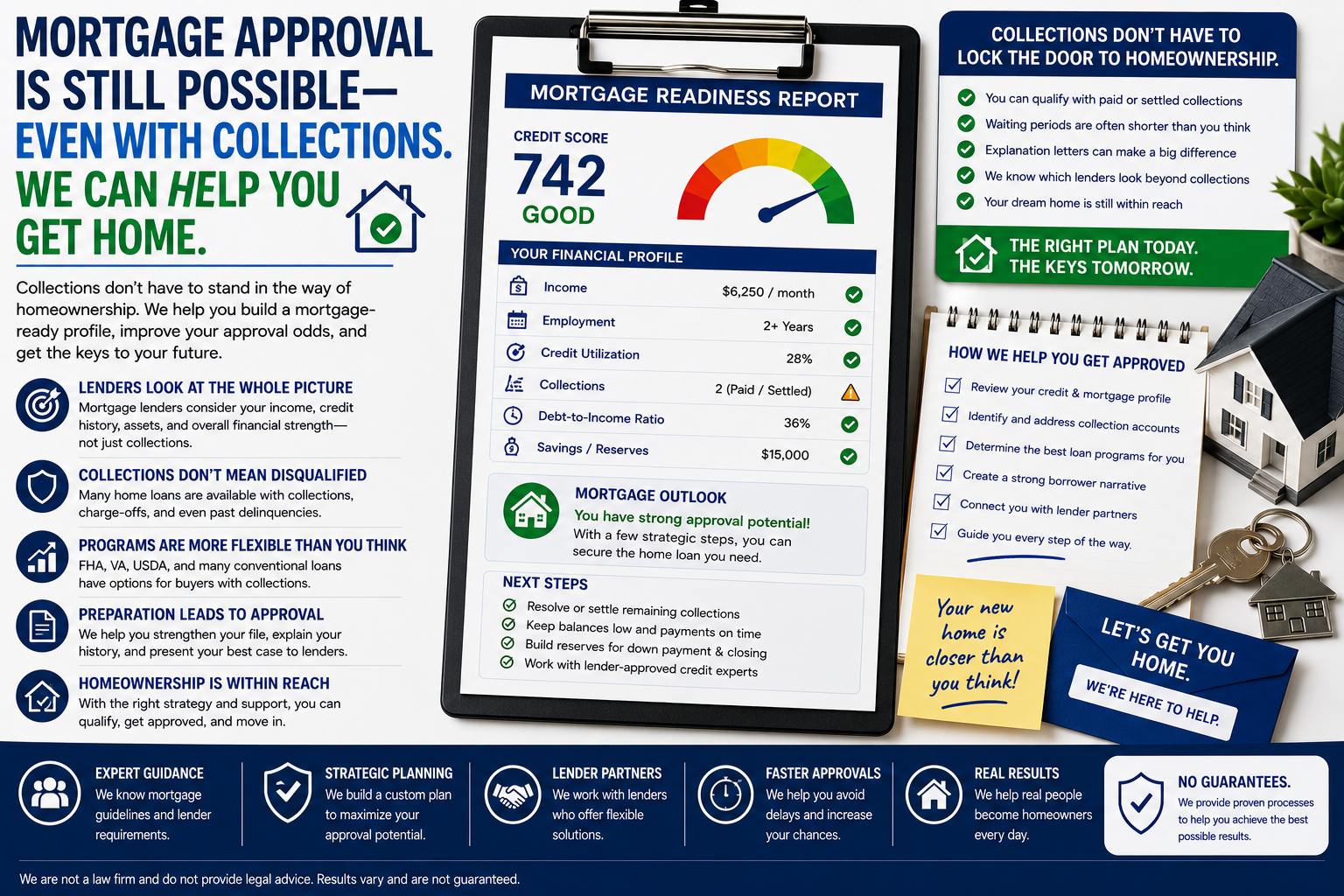

This page is written for homebuyers in Roswell, Fulton County, and nearby communities who want to understand their credit report before applying for a mortgage. Superior Credit Repair Online does not promise approval, a specific score, or overnight changes. The purpose is to help you review the credit report, identify possible inaccuracies, document what needs attention, and build a realistic mortgage-readiness plan.

Credit report preparation matters because credit reports and credit scores can affect a mortgage conversation. The Consumer Financial Protection Bureau explains that credit score and credit report information can influence mortgage eligibility and the rate a consumer may pay. That is why a careful review before applying can be more useful than waiting until a lender has already identified a problem.

Why a mortgage-focused credit report review matters in Roswell

A mortgage-focused review is more detailed than looking at a score app. A score can help you see a general direction, but the account information behind the score is what often creates questions. A buyer may have a score that looks close to a target range but still have collection accounts, recent late payments, high utilization, or inconsistent bureau reporting that needs attention before preapproval.

Roswell buyers may be looking at established neighborhoods, move-up homes, and first-time buyer options where credit readiness can affect confidence before making an offer. In that kind of situation, the review should not be random. It should start with the full report, compare the bureaus, and organize the accounts by issue type. The goal is to understand what is reporting, who is reporting it, whether balances and dates appear correct, and what documentation may help if something is wrong.

For many buyers, the benefit is clarity. Instead of guessing whether a collection will matter, whether a late payment can be explained, or whether a high balance should be paid down first, the review creates a written understanding of what should be addressed and what questions should be taken to a mortgage professional.

Credit report issues that should be reviewed before a home loan conversation

Payment history is one of the first areas to review. Late payments can affect confidence before preapproval, especially when they are recent, repeated, or reported differently across the bureaus. The review should identify the account, the month reported late, whether the account is still open, and whether there is documentation that supports a correction request if the reporting is wrong.

Collections are another major concern for homebuyers. A collection can come from a medical bill, utility account, apartment balance, credit card, personal loan, auto deficiency, or other past obligation. Before making a decision, a buyer should know who is reporting the collection, whether the balance appears accurate, whether the original creditor is also reporting, and whether the item appears duplicated.

Charge-offs require careful review because they can appear with confusing balances, collection accounts, transfer notes, or inconsistent dates. Some buyers assume a charge-off is simply old and cannot matter. Others panic and make a payment without understanding how the account is being reported. A mortgage-readiness review helps the buyer slow down and identify the facts.

Credit card utilization is also important. High balances can affect a score even when payments are current. A buyer preparing for a home loan should know each card limit, current balance, due date, statement date, and whether the reported balance reflects the actual balance. Lowering utilization can be part of a plan, but it should be done with clear timing and without creating new confusion.

Identity information and mixed-file concerns should also be reviewed. Incorrect addresses, name variations, accounts that do not belong to the buyer, or information that appears connected to another person can create stress before preapproval. If the information is wrong, the buyer may need documentation and a clear dispute explanation.

How Superior Credit Repair Online structures the Roswell review

The process begins with a full credit report review, not a quick score glance. The report is organized by account type and issue type so the buyer can see what may be affecting mortgage readiness. The review looks for inaccurate, incomplete, outdated, duplicated, or unverifiable information and separates those concerns from accurate information that may need longer-term rebuilding.

Review all three bureaus when available

One bureau may show a collection that another bureau does not show. A balance may appear differently from one report to another. A late payment may be present on only one bureau. Reviewing all three helps create a more complete picture.

Document the issue before choosing an action

Documentation may include statements, payment records, collection letters, settlement letters, identity documents, address records, medical billing documents, or correspondence from a lender or creditor. The right records depend on the issue being reviewed.

Prioritize mortgage-readiness concerns

A buyer preparing to apply soon may need to prioritize differently from someone planning a purchase next year. The plan should focus on the issues most likely to create questions during preapproval while also supporting healthier long-term credit habits.

Use realistic expectations

No credit repair company should promise a specific score, approval, or deletion of accurate negative information. A realistic review focuses on accuracy, documentation, dispute rights, and rebuilding habits.

Local planning notes for Roswell and North Metro Atlanta homebuyers

Roswell buyers may be comparing homes in areas such as Alpharetta, Milton, Sandy Springs, Johns Creek, East Cobb, and communities throughout north metro Atlanta. The credit report itself is not local, but the pressure to make decisions can be local. A buyer who wants to make an offer soon may need to understand the credit report quickly. A buyer planning several months ahead may have time to lower balances, gather documents, and address errors more carefully.

A buyer with older collections

A buyer in Roswell may see a collection from a medical provider, old apartment balance, utility account, or charged-off credit account. The review should look at the collector name, original creditor, balance, dates, and whether the same account appears more than once.

A buyer with high card balances

A buyer can pay every account on time and still have a weaker score because card balances are too close to the limits. A plan should review balances, limits, due dates, and statement timing so the buyer understands the utilization picture.

A buyer after a previous denial

A previous denial can feel discouraging, but it can also provide useful clues. Denial reasons, credit report details, and lender notes can help shape the next credit-readiness plan.

These examples are educational. They are not promises and they are not legal, lending, or tax advice. They show why a written credit-readiness plan can be more useful than guessing or reacting emotionally.

How FHA, conventional, VA, and USDA mortgage conversations may involve credit

Many buyers ask about FHA first because FHA is often discussed when credit scores are lower. HUD’s FHA guidance explains that the minimum decision credit score can affect the maximum loan-to-value level. That does not mean every buyer with a certain score is automatically approved. Lenders may consider additional factors, including income, debt, reserves, payment history, and documentation.

Conventional, VA, and USDA mortgage conversations can also involve credit history, collections, charge-offs, payment patterns, and current balances. A credit review does not replace lender guidance. Instead, it helps the buyer understand the report before speaking with a lender so the conversation can be more focused.

For a buyer in Roswell, the smartest approach is to treat credit preparation as one part of the larger homebuying process. Income, employment, savings, debt-to-income ratio, property type, and loan program requirements can all matter. Credit is not the only factor, but it is one of the areas a consumer can review before the process becomes urgent.

Documents and details to gather before the review

A more complete review starts with better information. If you have not checked your reports recently, the CFPB explains that consumers can request free credit reports through the legally authorized source. Bring all three bureau reports when possible and save any documents connected to the items that concern you.

- Recent Equifax, Experian, and TransUnion credit reports if available.

- Mortgage denial letters, lender notes, or preapproval feedback if you have them.

- Collection letters, settlement letters, receipts, or payment confirmations.

- Medical billing documents or insurance records for medical collections.

- Credit card statements showing balances, limits, and payment dates.

- Identification and address documents if an account may not belong to you.

- A target timeline for applying, shopping, or speaking with a lender.

This list helps the review stay organized. It also helps you separate facts from assumptions before you choose next steps.

How to avoid common credit mistakes before preapproval

One common mistake is applying for new credit without understanding how the inquiry, new account, and possible balance may affect the report. Another mistake is closing an older card without thinking about utilization and credit history. A third mistake is paying a collection without saving documentation or understanding how the account is currently reporting. None of these decisions should be made out of fear.

A better approach is to review the report first, decide which items need documentation, and understand the likely timeline. If an item is inaccurate, the dispute should clearly explain what is wrong and include supporting information. If an item is accurate but affecting readiness, the buyer may need a rebuilding plan or lender guidance instead of a dispute.

Why visible accuracy matters for Georgia buyers

Accuracy matters because a mortgage conversation can involve more than a score. A lender may ask about payment history, balances, unresolved debts, or explanations for specific accounts. If the report contains information that is wrong, duplicated, incomplete, or outdated, the buyer should know that before applying. If the information is accurate, the buyer should understand how it fits into the broader readiness plan.

For buyers in Roswell, this kind of preparation can reduce stress. It gives you a clearer list of issues, a documentation checklist, and a more practical way to talk with a lender or housing professional. It also helps you avoid trying to fix everything at once without knowing what matters most.

What success should look like

Success should look like clarity and progress, not unrealistic promises. A strong review should help you understand the accounts on your report, identify possible inaccuracies, know which documents to gather, and follow better credit habits while preparing for a mortgage. Even when every issue cannot be fixed quickly, knowing the facts can help you make better decisions.

Questions to answer before a lender reviews the file

Before a mortgage professional reviews the file, a Roswell buyer should be able to answer several practical questions. Which accounts are currently open? Which accounts show balances? Which accounts are closed, charged off, transferred, or placed for collection? Are there any accounts that appear on one bureau but not another? Are there balances that look wrong? Are there old addresses, unfamiliar names, or accounts that may not belong to the buyer? These questions help turn a stressful credit report into a list that can be reviewed one issue at a time.

Another important question is whether the buyer has a clear timeline. A person hoping to apply in thirty days may need a different approach than someone planning to apply in six months. Short timelines usually require more caution because new disputes, new accounts, or sudden credit moves can create follow-up questions. Longer timelines may allow more room to lower balances, build positive payment history, gather documents, and correct inaccurate reporting before a full mortgage review.

The goal is not to make the report perfect overnight. The goal is to understand the file well enough to make better choices. If a collection balance looks wrong, the buyer should know what documents may support a correction. If a late payment appears incorrectly, the buyer should know which statement, payment confirmation, or creditor letter may be useful. If utilization is high, the buyer should understand how balances and statement dates may affect the reported information.

A practical credit-readiness path for Roswell homebuyers

A practical path starts with a full report review, then moves into issue organization. The buyer should group items into categories: active accounts, collections, charge-offs, late payments, high balances, medical debt, inquiries, closed accounts, and information that appears unfamiliar. This makes the file easier to understand and helps avoid jumping from one problem to another without a clear plan.

After the issues are grouped, the next step is documentation. Documentation is what separates a serious review from a guess. A buyer in Roswell may need billing records, payment confirmations, insurance explanations of benefits, settlement letters, creditor correspondence, address records, identity documents, or old statements. Not every account requires the same proof, but every questionable account should be reviewed with enough detail to decide what kind of proof may be helpful.

The third step is action planning. Some items may be appropriate for a dispute or verification request if the information is inaccurate, incomplete, outdated, duplicated, or not connected to the buyer. Other items may be accurate but still need a rebuilding strategy. That may include consistent on-time payments, lower revolving balances, fewer unnecessary applications, and a more careful plan for using credit while preparing for a mortgage.

The fourth step is communication. A buyer should know what questions to ask a lender and what information to share. Credit repair is not the same as lending advice, and a lender may have program-specific requirements. A clean, organized credit review can help the buyer ask better questions about FHA, conventional, VA, USDA, down payment planning, debt-to-income ratio, reserves, and documentation.

Building confidence before shopping in Fulton County

When buyers shop for homes around Roswell, Fulton County, and the surrounding North Metro Atlanta communities, they often want to know whether they are financially ready before falling in love with a property. Credit readiness is one piece of that confidence. It does not replace savings, income, employment, or lender review, but it can help the buyer understand the credit report before the home search becomes emotional.

Confidence comes from facts. If the buyer knows which accounts need review, which balances are high, which items may be inaccurate, and which documents are missing, the next step becomes clearer. That does not mean every issue will be solved quickly. It means the buyer is no longer making decisions in the dark. For many people, that alone is an important improvement before the mortgage process begins.

Superior Credit Repair Online helps consumers approach this process with realistic expectations. The focus is accuracy, documentation, organization, and long-term credit improvement habits. For a Roswell homebuyer, that can mean replacing fear with a written review and a plan that supports the next mortgage conversation.

Public resources for credit report and mortgage-readiness questions

These public resources can help consumers understand credit reports, dispute rights, free credit reports, and FHA score guidance. They are provided for education and do not replace personal advice from a lender, attorney, housing counselor, or financial professional.

Georgia office reference

Superior Credit Repair Online serves consumers in Roswell, Fulton County, and across Georgia. Local office reference for Georgia pages: 1372 Peachtree St NE, Atlanta, GA 30309.

Prepare your credit before the mortgage conversation

If you are trying to buy a home in Roswell and your credit report includes collections, late payments, charge-offs, high credit card balances, medical collections, or accounts that do not look right, a structured review can help you understand what needs attention. Start with a clear look at the report, a realistic plan, and documentation that supports the next steps.

Frequently asked questions

Can a Roswell buyer review credit before applying for a mortgage?

Yes. Many buyers review their reports early so they can understand collections, late payments, high balances, charge-offs, or possible reporting errors before a full lender review.

Does credit repair guarantee mortgage approval?

No. Credit repair does not guarantee approval, a specific score, or a certain loan term. It can help consumers review and address inaccurate, unverifiable, or incomplete credit report information.

What credit issues should be reviewed before preapproval?

Common issues include collections, charge-offs, late payments, high utilization, duplicate accounts, medical collections, incorrect balances, mixed-file information, and accounts that do not belong to the consumer.

Should I dispute every negative item before a mortgage?

Not necessarily. A mortgage-focused review should be careful and organized. Some items may need documentation, some may need lender guidance, and some may not be appropriate to dispute if they are accurate.

Does Superior Credit Repair Online serve buyers in Roswell and Georgia?

Yes. Superior Credit Repair Online helps consumers in Roswell, Fulton County, and across Georgia review credit report issues connected to mortgage-readiness planning.