Alabama mortgage-readiness credit help

Build the plan around the file in front of you

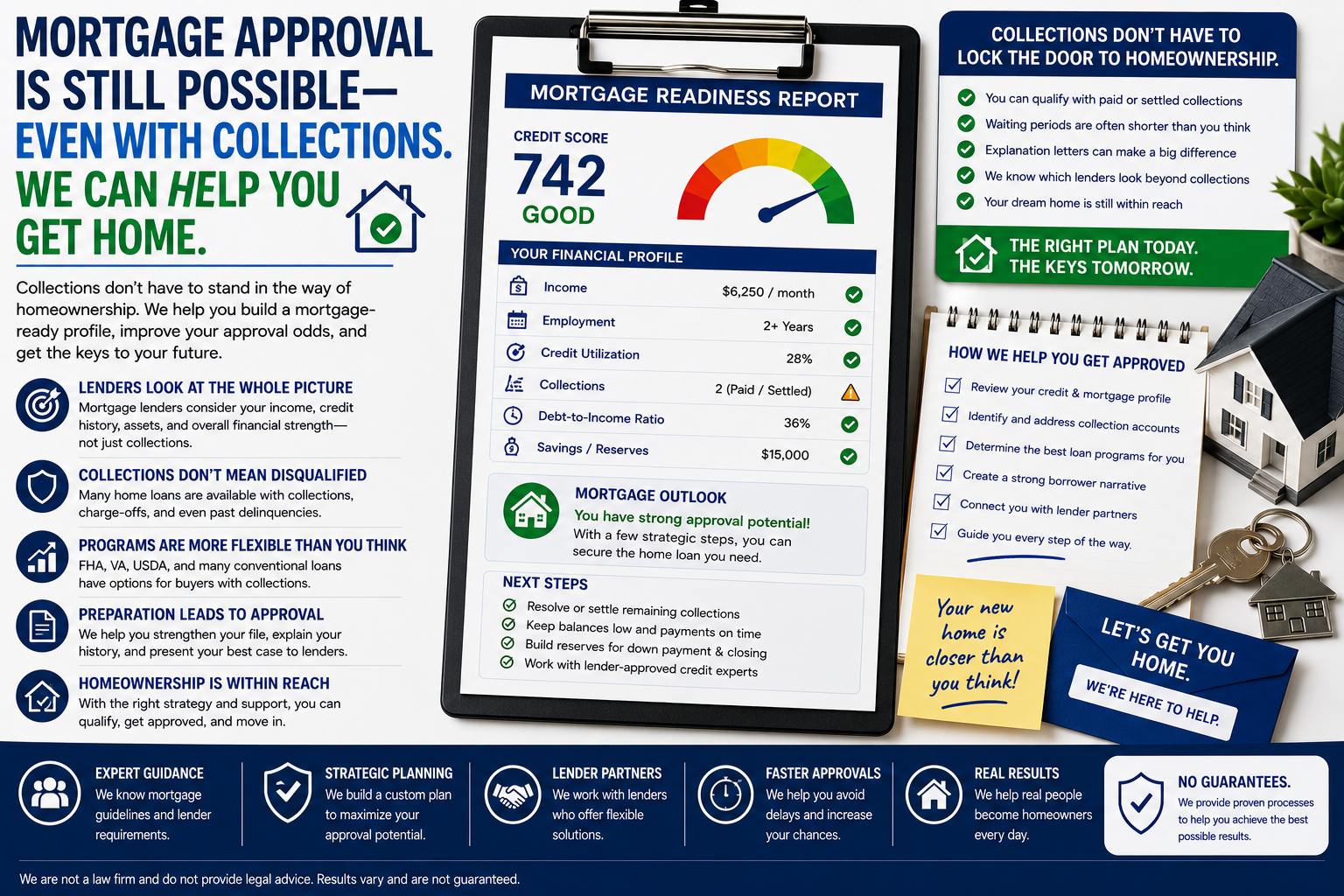

A home loan credit report review is a practical starting point when you want to buy in Athens, Alabama but are not sure what your credit file will show to a lender. Superior Credit Repair Online helps homebuyers review collections, late payments, charge-offs, high credit card balances, medical collections, mixed-file concerns, identity details, and reporting errors that may affect mortgage readiness.

This service is educational and document-focused. It does not promise mortgage approval, a specific credit score increase, a deletion, or a certain result. The purpose is to help you understand the credit file before a lender conversation becomes urgent.

What a Athens home loan credit report review should cover

A review is not the same as a promise that a mortgage will be approved. It is a way to slow down, read the file, identify accounts that may deserve a closer look, and decide what questions to ask before you submit a full application.

In Limestone County, buyers may be preparing for a first home, a move-up home, a relocation, or a new construction purchase. Each situation can put pressure on timing, but credit work should still be handled carefully and documented clearly.

The goal is to help you understand the credit report as a mortgage-related document, not just as a score. A lender may review trade lines, dates, balances, payment history, account status, inquiries, public-record style entries, identity details, and explanations for recent activity.

For many families, the confusing part is that the same account can look different across Equifax, Experian, and TransUnion. One bureau may show a balance, another may show a different date, and another may show a status that does not match what the consumer believes happened.

That is why a mortgage-focused review should be organized around documentation, reporting accuracy, and readiness. It should help you see which items are simple education issues, which items may need dispute attention, and which items may be better discussed with a qualified mortgage professional.

For Athens, Alabama, the local service reference for this Alabama page is 7027 Old Madison Pike Ste 108, Huntsville, AL 35806. The page may serve buyers in Athens, surrounding communities in Limestone County, and nearby parts of North Alabama / Tennessee Valley. The office reference should match the visible content and the structured data so visitors and search systems receive the same location information.

A local credit-readiness page should also explain that the work is educational and document-focused. Consumers should feel that the page is written for them, not for an internal checklist. The language should speak to families, first-time buyers, returning buyers, and people trying to recover after credit setbacks.

The most helpful pages do not tell a buyer that approval is guaranteed. They help the buyer understand what may be on the report, why it may matter, what questions should be asked, and how a structured review can make the next conversation more organized.

Credit report issues that may matter before a home loan

A mortgage-related credit review should be more detailed than a quick glance at a score. The goal is to understand the accounts and reporting patterns that may raise questions, slow down preapproval, or create confusion during the homebuying process.

Collections before a mortgage conversation

Collection accounts can create worry for Athens buyers because they may raise questions about unpaid obligations, dates, balances, ownership, and whether the account is reporting consistently. A helpful review looks for duplicate collection entries, medical collections, paid collections that still show confusing statuses, and accounts that may not clearly identify the original creditor. When a collection appears on the report, the first step is understanding what is being reported before deciding whether a dispute, documentation request, or lender conversation makes sense.

Late payments and payment history

Late payments are especially important because mortgage conversations often focus on whether the buyer can manage a new housing payment. A review should look at 30-day, 60-day, 90-day, and more serious late marks, along with dates, account status, and whether the payment history makes sense. If a late payment appears inaccurate, duplicated, or attached to an account that should be reporting differently, that issue may need attention before preapproval.

Charge-offs, repossessions, and old negative accounts

Charge-offs and repossessions can feel discouraging, but they should still be reviewed carefully. The account may have a balance, a transfer history, a collection relationship, or dates that do not appear consistent. Buyers in Athens, Alabama should not assume every old negative item is being reported correctly. The review should separate emotional stress from the reporting details so the next step is based on the file itself.

High credit card balances and utilization

High credit card utilization can affect how a credit profile looks even when every payment has been made on time. A mortgage-readiness review should look at revolving balances, individual card utilization, overall utilization, recently reported balances, authorized user accounts, and whether a card reports a limit correctly. This area is important because utilization problems may be different from derogatory reporting problems.

Identity, address, and mixed-file concerns

Identity details matter because credit reports are built from personal information, account data, and creditor reporting. Names, addresses, Social Security number variations, date-of-birth issues, and accounts that may belong to someone else can cause confusion. If the file contains mixed information, a simple score goal will not solve the deeper problem. The review needs to look at the report structure itself.

Medical collections and family credit pressure

Medical collections can surprise buyers who thought insurance handled the bill or who never received clear notice. In a homebuying situation, the key is to understand what appears, which bureau reports it, whether the amount is accurate, and whether the item is connected to other collection activity. Families in North Alabama / Tennessee Valley may need a calm review of these accounts before making decisions.

A careful review process for Athens, Alabama buyers

Superior Credit Repair Online uses a structured review approach so buyers can understand what is on the file before they feel pressured by a deadline. This kind of preparation is helpful for first-time buyers, returning buyers, families relocating within Alabama, and people rebuilding after a denial or difficult financial season.

Read the full report, not only the score

A score is a snapshot, but the report explains what is driving the concern. The review should read each bureau file line by line, including open accounts, closed accounts, collection accounts, inquiries, personal information, balances, limits, and dates. This helps the buyer avoid making decisions based only on fear or a single number.

Mark accounts that may affect mortgage readiness

Not every account deserves the same attention. The review should mark items that may create questions before preapproval: recent late payments, unpaid collections, charge-offs, repossessions, high balances, duplicate entries, inconsistent dates, and accounts that do not belong to the consumer.

Separate accuracy issues from strategy issues

Some items may be inaccurate or incomplete. Other items may be accurate but still require planning. A strong process separates those categories so the buyer does not dispute everything blindly or ignore items that deserve documentation. The purpose is an organized review, not a rushed reaction.

Build a document list

Helpful documents may include payment confirmations, settlement letters, identity records, account statements, insurance explanations, correspondence from collectors, or proof that an account should be updated. Having records in one place can make the next steps easier if a dispute or verification request is appropriate.

Create a timing plan before applying

Mortgage timing matters. Buyers should understand that credit report updates, lender pulls, documentation, and preapproval conversations may not all happen on the same schedule. A cleanup plan should avoid last-minute surprises by organizing action steps before the buyer is under contract.

Keep communication realistic

The review should never promise a specific approval, score increase, deletion, or result. The safer approach is to explain what can be reviewed, what may be challenged when appropriate, and what habits may support a stronger file over time. Honest expectations protect the buyer from making decisions based on pressure.

Buyer-readiness notes for Athens households

Athens buyers may be comparing homes near Huntsville, Madison, Decatur, and the I-65 corridor while trying to understand whether credit report issues could affect a mortgage conversation.

One buyer may need help with medical collections, another may need to understand late payments, and another may simply need a clearer picture of credit card utilization before applying. The review should meet the buyer where they are instead of treating every credit file the same way.

For Athens, Alabama, this is especially important because buyers may be comparing different neighborhoods, price points, property taxes, insurance costs, and commute decisions. Credit report uncertainty adds another layer of stress. A clear review helps the buyer slow down and focus on what the report actually says.

The most useful plan is written in plain English. It explains what appears on the report, why it may matter, what documentation could help, and which items may require professional review. It should not bury the buyer in technical terms or make promises that nobody can honestly guarantee.

Common situations this page can help organize

A first-time buyer in Athens may have never reviewed all three reports before. They may only know a score from a banking app, but that score may not show the full reporting history. A page like this should encourage them to gather the actual reports and understand the details before assuming they are ready or not ready.

A buyer relocating into North Alabama / Tennessee Valley may have a good income but older credit damage from a prior job loss, divorce, medical situation, or vehicle repossession. The review should help them understand what is still appearing, how it is being reported, and which items may need attention before a mortgage conversation moves forward.

A family trying to move because they need more space may be dealing with high credit card balances from childcare costs, repairs, or medical expenses. In that case, the review should not shame the buyer. It should explain utilization, balances, limits, and reporting dates in plain English.

A self-employed buyer or commission-based worker may already have extra documentation requirements for the loan process. If credit report issues are also present, the buyer benefits from a clean written plan that separates income documentation from credit-report accuracy questions.

A buyer who was already denied or told to come back later may feel embarrassed. The better approach is to review the reason carefully, compare it with the reports, and build a plan around what can be verified, corrected, documented, or improved before another conversation.

When the review shows items that need attention, the next step is usually a clear preapproval credit cleanup plan that organizes what can be disputed, what may need documentation, and what habits may help reduce risk before preapproval.

Documents and details to gather before the review

Before you request help, gather anything that explains the accounts you are worried about. The review can move more smoothly when the information is organized from the beginning.

- Recent credit reports from all three major bureaus, if available.

- Collection notices, medical billing letters, settlement letters, or payment confirmations.

- Statements showing account numbers, balances, limits, or payment history.

- Identity information if the file shows names, addresses, or accounts that do not look familiar.

- Any lender notes explaining why preapproval was delayed, denied, or paused.

- A short written summary of your homebuying goal, including approximate timing and the type of credit issues causing concern.

Having these details ready does not guarantee a result, but it does help create a more organized conversation. It also helps separate account accuracy questions from broader budgeting, lending, and homebuying questions that should be handled with the right professionals.

Helpful public credit and mortgage resources

These public resources can help you understand credit reports, dispute rights, and mortgage-credit questions while you review your own file.

Alabama location reference for this page

Superior Credit Repair Online serves Alabama consumers preparing for mortgage-readiness credit review. Local office reference for this page: 7027 Old Madison Pike Ste 108, Huntsville, AL 35806.

This page is written for buyers in Athens, Alabama, Limestone County, and nearby parts of North Alabama / Tennessee Valley who want a clearer credit report review before speaking with a mortgage professional or returning for another preapproval attempt.

Questions Athens buyers ask before mortgage preapproval

Can I buy a house in Athens if I have bad credit?

Some buyers with credit problems may still have options, but it depends on the full mortgage file, lender requirements, income, debts, down payment, recent history, and what appears on the credit reports. A credit review helps identify reporting issues that may need attention before you speak with a lender or return for another preapproval attempt.

Should I dispute credit report errors before mortgage preapproval?

If an account is inaccurate, incomplete, outdated, duplicated, unverifiable, or belongs to someone else, it may deserve review. However, timing matters when a mortgage is involved. The safest approach is to understand the account, gather documentation, and avoid making rushed changes without knowing how they may affect the loan conversation.

Do collections always stop a mortgage?

Collections do not affect every buyer the same way. The type of collection, balance, date, payment status, bureau reporting, lender guidelines, and overall credit file all matter. A review helps you see whether collections are reporting accurately and whether they may create questions during preapproval.

Can late payments affect a home loan conversation?

Yes, late payments can matter because they speak to payment history. The review should look at how recent the late payments are, whether the account is still open, whether the dates look correct, and whether documentation supports a different reporting status.

Will paying down credit cards help before applying?

Lower balances may help some buyers, especially when utilization is high, but the impact depends on the full credit profile and when the card issuer reports updates. A mortgage-readiness review should look at balances, limits, minimum payments, and reporting dates before deciding on a plan.

Is this the same as mortgage lending advice?

No. Credit repair and credit report review are not the same as mortgage lending, underwriting, tax advice, or legal advice. A credit review helps you understand credit report issues. You should still speak with a qualified mortgage professional about loan programs and approval requirements.

What should I have ready for a Athens credit review?

Helpful items may include recent credit reports, collection letters, account statements, payment confirmations, identity documents, correspondence from creditors or collectors, and any lender notes explaining why the file needs work before preapproval.

Request a home loan credit report review

If credit report problems are making your homebuying plans feel uncertain, start with a careful review. Superior Credit Repair Online can help you look at collections, late payments, charge-offs, high balances, medical collections, identity concerns, and inaccurate reporting before the next mortgage conversation.

Request a credit report review with Superior Credit Repair Online