A lot of people first search how to boost a credit score for free when something important is already on the calendar. Maybe you're planning to buy your first home. Maybe a lender told you your scores need work before FHA, VA, USDA, or conventional mortgage approval. Maybe you checked your credit after months of avoiding it and saw old collections, high balances, or account details that don't look right.

That moment can feel heavy. But it doesn't mean you're stuck.

The practical path usually isn't a trick or a shortcut. It's a calm review of your credit reports, a careful correction of anything inaccurate, and a plan for improving the parts of your file that mortgage lenders care about. If you're not sure where to begin, it helps to first understand how your credit score is determined, because that makes every next step easier to judge.

Free credit improvement can be worthwhile. It can also be misunderstood. Some tools help with consumer-facing scores but don't necessarily change what a mortgage lender sees. Other steps, like finding and disputing errors, may matter much more if you're trying to become lender-ready.

This guide takes the mortgage-readiness angle seriously. It looks at the no-cost options people commonly use, explains what they can and can't do, and keeps the focus on realistic progress. If you're trying to prepare for a home loan, lower your risk profile, or rebuild with a clearer plan, that's the right mindset.

Table of Contents

- Introduction A Practical Path to a Stronger Credit Profile

- The Foundation of Credit Improvement Reviewing Your Reports

- Correcting Inaccuracies Through the Legal Dispute Process

- Optimizing Your Existing Credit Without New Debt

- Using Alternative Data Rent and Utility Reporting

- Next Steps Realistic Timelines and Professional Guidance

- Frequently Asked Questions About Improving Your Credit

Introduction A Practical Path to a Stronger Credit Profile

A first-time homebuyer often starts with optimism and ends the day staring at a credit app in silence.

The pattern is familiar. Someone checks their score because they're ready to talk to a lender. They expected a few small issues. Instead, they find high card balances, an old medical collection, or a late payment they thought was resolved months ago. Then the search begins for ways to boost credit score for free, usually with a mix of urgency and confusion.

That urgency is understandable. It just needs direction.

Credit improvement works best when you separate displayed score changes from mortgage-readiness changes. A score shown in an app can be useful, but mortgage lenders often look deeper. They review payment history, account stability, collections, charge-offs, utilization, and whether the file looks consistent and explainable. A stronger credit profile is usually built through accuracy, documentation, and better account management.

Why free strategies can still be powerful

Free steps matter because they help you control the parts of the process that don't require new debt or paid products. If your report contains mistakes, correcting them may help. If your balances are reporting too high, changing when you pay can help. If your file is thin, selective tools may add positive information, though not always in the way borrowers expect.

Practical rule: Start with what is already on your reports before trying to add something new.

Mortgage applicants benefit most from a methodical approach. That means checking all three reports, identifying anything inaccurate or outdated, disputing only what you can explain and document, and tightening current account habits. That process won't promise overnight results, but it gives you something much better: a cleaner and more defensible credit file.

The Foundation of Credit Improvement Reviewing Your Reports

Before you try any tactic meant to improve credit score results, pull your reports and read them carefully. This is the step many people skip, and it's often the step that matters most for mortgage credit repair and lender readiness.

Free access has expanded. AARP notes that consumers can get credit reports weekly, not just annually, through AnnualCreditReport.com according to AARP's credit guidance. That makes regular review much easier if you're preparing for a mortgage and want to catch problems before a lender does.

Start with all three reports

Don't assume one bureau tells the whole story. Mortgage lenders usually review information from Experian, Equifax, and TransUnion, so your job is to compare all three.

Use this simple review order:

Personal information

Check your name, address history, employers, and any variations that don't belong to you. Wrong identifying details can be a sign that accounts were mixed into the wrong file.Account history

Look at open and closed accounts. Make sure balances, payment status, and dates are reported consistently.Negative items

Review collections, charge-offs, repossessions, and late payments. Ask one question for each item: is this accurate, complete, and mine?Credit inquiries

If you see inquiries you don't recognize, flag them for follow-up.

For readers comparing educational tools, this outside guide on how to improve your credit score may help frame common improvement methods, but your own reports still need to be the starting point.

What to review line by line

Many report errors aren't dramatic. They're subtle. And subtle errors can still affect a mortgage application.

Watch for these problems:

- Wrong balances: The balance may be outdated or higher than your latest statement.

- Accounts marked open when they were paid and closed: That can make your file look less stable than it really is.

- Late payments reported incorrectly: If you paid on time or caught up under a documented arrangement, keep the records.

- Accounts that don't belong to you: This deserves immediate attention.

- Duplicate negative entries: Sometimes one debt appears in more than one way.

A short checklist can keep you organized.

| Report area | What to ask |

|---|---|

| Personal details | Is every name, address, and employer accurate? |

| Revolving accounts | Are balances and limits current? |

| Installment loans | Does status match reality? |

| Collections | Is the owner, amount, and status accurate? |

| Late payments | Do the dates match your records? |

When people say they want to boost credit score for free, the first real opportunity is often hidden in the report itself.

If you're buying a home soon, review your file like an underwriter would. Lenders don't just want a better number. They want fewer surprises.

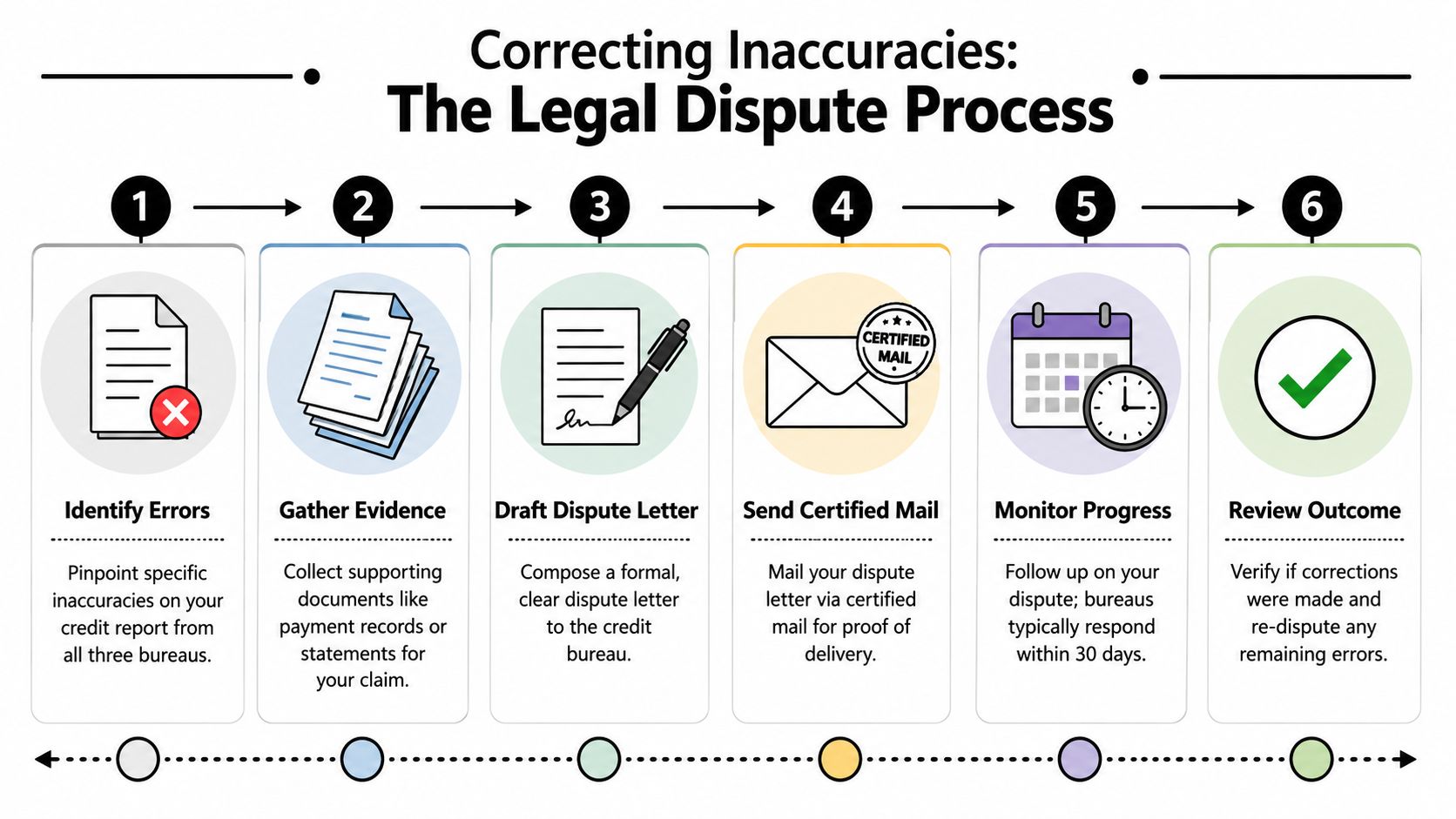

Correcting Inaccuracies Through the Legal Dispute Process

When you find an error, the next step isn't guessing. It's documentation.

The legal dispute process exists so consumers can challenge inaccurate, outdated, unverifiable, or misleading information. That's why credit restoration should be handled as a records-based process, not a volume game. The stronger your proof, the stronger your position.

The issue is common enough to take seriously. The Consumer Financial Protection Bureau states that about 20% of consumers have at least one error on their credit report, and correcting those errors can lead to score increases ranging from 20 to 50+ points, depending on the seriousness of the item, as explained in the CFPB report on credit report errors.

Which errors deserve immediate action

Not every negative account is inaccurate. Some are painful but valid. Focus first on items you can specifically challenge.

Examples include:

- A paid account still showing open

- A balance that doesn't match your records

- A late payment that has been resolved

- An account tied to identity theft

- A medical or collection account reported with incomplete or conflicting details

If a collector is involved, it also helps to understand how to use debt validation letters, especially when the issue is whether the debt can be properly substantiated.

How to file a dispute the right way

The strongest disputes are precise. They identify one issue at a time, explain what's wrong, and attach relevant proof.

A practical process looks like this:

List the account exactly as shown

Use the creditor name, account number fragment, and bureau reference details.Describe the inaccuracy clearly

Don't write, "This is hurting my score." Write, "This account is marked late for a month that my bank records show was paid on time."Attach supporting records

Bank statements, settlement letters, account closure confirmations, identity theft documents, and billing statements are useful when they directly support the dispute.Submit through the bureau's portal or in writing

Keep copies of everything you send.Track the response window

Bureaus generally investigate within 30 to 45 days, based on the verified data provided for the dispute process.

A vague dispute asks the bureau to guess. A documented dispute gives the bureau something to verify.

There are also common failure points. If you dispute too many items at once without evidence, a bureau may treat the dispute as frivolous and reject it without meaningful investigation. Medical debt disputes can be especially vulnerable if the explanation is incomplete. The better approach is narrower, cleaner, and supported.

For mortgage credit repair, that discipline matters. Underwriters care about whether issues were corrected, not whether a consumer sent a stack of generic letters.

If an investigation comes back and the error remains, review the result carefully. Sometimes the bureau misunderstood the issue. Sometimes the furnisher responded with incomplete data. If your records still support your position, follow up with a more targeted dispute rather than resending the same statement.

Optimizing Your Existing Credit Without New Debt

Some of the best free credit habits don't involve opening anything at all. If you're preparing for a mortgage, that's often a good thing. New accounts can complicate timing, create new inquiries, and shift the focus away from the file you already have.

What you can control right now is how your current accounts report.

Use timing to manage utilization

Credit utilization means how much of your revolving credit you're using compared with your limits. Even if you pay in full every month, a high statement balance can still report and make your file look stretched.

Two no-cost habits can help:

- Pay before the statement closes: If you reduce the balance before the card issuer reports it, your report may show lower usage.

- Make smaller payments during the month: This can keep balances from building up between due dates.

Here's a plain example. If a card gets used heavily for groceries, gas, and recurring bills, the balance might look high at statement time even if you always pay it off later. A payment made before the statement date can change what gets reported.

Think carefully before using an authorized user strategy

Becoming an authorized user on a family member's credit card can sometimes help a thin file, but only if the primary cardholder manages the account very well. If they carry high balances or miss payments, that can work against you.

Use this checklist before agreeing:

- Choose a stable account: The card should have a long, clean history.

- Confirm reporting: Make sure the issuer reports authorized users to the bureaus.

- Set expectations clearly: Decide whether you will use the card or be added for reporting purposes.

Clean habits on existing accounts usually matter more than chasing a new account for the sake of a quick score change.

If your file is very limited and you're considering future rebuilding tools, this overview from Superior Credit Repair on secured card benefits explains how secured cards may fit into a longer-term rebuilding plan. For mortgage preparation, though, timing matters. Many borrowers are better served by stabilizing balances and protecting on-time payments first.

Often, people misunderstand the approach. They search for a free trick, but the bigger win is account consistency. Lower reported balances, no missed due dates, and fewer avoidable changes tend to create a stronger profile than constant credit activity.

Using Alternative Data Rent and Utility Reporting

Alternative data tools appeal to people who pay bills reliably but don't see those payments reflected in traditional credit reporting. That's why rent reporting, utility reporting, and bill-reporting tools get so much attention from renters, thin-file consumers, and people trying to rebuild after hardship.

These tools can be useful. They can also be misunderstood, especially by homebuyers.

How Experian Boost works

Experian Boost is one of the most visible free options. To use it, a person connects their bank account so Experian can verify on-time payments for utility, cell phone, and streaming services. The system scans transaction history for recognized payment descriptors and on-time patterns, then adds eligible positive history to the user's Experian credit file.

According to Experian's explanation of Experian Boost, about 79% of users see an immediate score increase when they first adopt it, and the average increase is 13 points for FICO Score 8.

That sounds encouraging, and for some users it is. But the mechanics matter. If the linked bank account doesn't show enough transaction history, if the payment pattern doesn't qualify, or if the account review is rejected, the result may be no score change at all.

Why mortgage applicants should be cautious

For mortgage readiness, the limitation is more important than the headline.

Experian Boost only affects the Experian file. It does not update Equifax or TransUnion. Many mortgage lenders review a tri-merge report and use older mortgage scoring models, so a consumer-facing increase may not change the score or loan decision that matters in underwriting.

That's why this tactic should be viewed as optional, not foundational.

A simple comparison helps:

| Tool | Possible benefit | Limitation for mortgage shoppers |

|---|---|---|

| Experian Boost | Adds certain positive bill payments to Experian | Doesn't update all three bureaus |

| Rent reporting services | May add rental history to one or more files | Lender treatment varies |

| Utility reporting tools | Can help thin files show payment consistency | May have limited impact on mortgage scoring models |

For renters, housing screening can involve more than a credit score alone. This article with insights for better tenant checks is useful because it shows how rental history and verification can shape decisions outside traditional lending.

The larger point is simple. If you're trying to boost credit score for free before buying a home, don't confuse a score display improvement with true mortgage readiness. Correcting inaccurate items, controlling utilization, and stabilizing the file usually carry more weight than a single-bureau boost.

Next Steps Realistic Timelines and Professional Guidance

Credit improvement usually feels slower than people want and faster than they expect once the right issues are addressed.

Disputes require patience because bureaus need time to investigate. Reporting changes tied to lower balances depend on when creditors update account information. Positive habits matter, but they need time to appear consistently across your file. If you're preparing for a mortgage, this is why last-minute credit repair before buying a home can be stressful. The earlier you start, the more options you usually have.

What progress usually looks like

A realistic plan often moves in stages.

First, you identify errors and gather records. Then you dispute only the items that are inaccurate or unverifiable. After that, you tighten account management, avoid unnecessary applications, and monitor your reports for updates. If you'd like a more detailed expectation framework, this Superior Credit Repair timeline guide explains how different parts of the process can unfold.

Slow progress with good documentation is usually more durable than a rushed approach with weak paperwork.

When outside help makes sense

Professional guidance can be useful when your file is complicated. That includes mixed files, identity theft issues, multiple collections, charge-off dispute help, late payment dispute help, or a mortgage denial that left you unsure what to fix first.

This is also where one structured option may help. Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. That kind of support isn't a shortcut and shouldn't be treated like one. It's a more organized way to handle a documentation-heavy process.

Be careful with any company that promises guaranteed deletions, guaranteed approval, or immediate score jumps. Ethical credit repair is based on accuracy, records, legal dispute procedures, and better long-term credit habits. Results vary because every credit file is different.

Frequently Asked Questions About Improving Your Credit

Can a goodwill letter remove a late payment

Sometimes, but it isn't a right and it isn't guaranteed. A goodwill letter is a polite request to a creditor asking them to consider removing a late payment after an otherwise strong history. It tends to work best when the late payment was isolated, you can explain the circumstances briefly, and the account is now in good standing.

Should you close an old credit card to simplify your finances

Usually, be cautious. Closing an older card can reduce available revolving credit and may increase utilization on the cards you keep open. If the account has no major downside, keeping it open and lightly used can support a steadier credit profile.

Do paid collections still matter when you're trying to buy a home

They can. Even when a collection is paid, a mortgage lender may still review the history, the timing, and whether the overall file shows stability. That's why homebuyers often need more than a paid receipt. They need a clean explanation of what happened and a stronger current profile.

Does a mortgage prequalification or mortgage in principle hurt your credit

It depends on how the lender handles the inquiry. Some early-stage screening is softer than a full application, but you should always ask. For a plain-language overview from a mortgage perspective, this article on mortgage in principle credit score impact is a helpful reference.

What if your credit problems are complicated

Start local if that feels easier. A practical resource like Superior Credit Repair's local guide can help you think through realistic next steps without hype. Complex files often involve several issues at once, such as utilization, collections dispute help, outdated reporting, and mortgage timing. In that situation, the best move is usually to organize the file problem by problem instead of looking for one universal fix.

If you're trying to boost your credit score for free with a serious goal in mind, especially mortgage approval, focus on what lenders are most likely to care about: accurate reporting, stable payment history, manageable balances, and a file that makes sense. Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation to better understand your options.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile. Share your experience with Superior Credit Repair