USDA Loan Readiness When Old Collections Still Report

USDA Loan Readiness When Old Collections Still Report works best when the plan is sequenced. A rushed file can create avoidable problems: balances report at the wrong time, disputes are opened too close to underwriting, collection updates appear without written terms, or the consumer applies before the report has been checked across all three bureaus.

For a borrower looking at a rural housing option, the timeline matters as much as the task list. A rural housing lender may evaluate old collections differently when the rest of the file shows cleaner recent payments, lower revolving balances, and organized documentation. The goal is not to do everything at once; it is to do the right things in the right order.

This guide breaks USDA loan readiness into practical stages. For a broader view, use mortgage approval credit repair planning with credit repair for apartment approval so your application timing and report cleanup are working from the same plan.

Days 1-30: know what is actually reporting

The first thirty days should be about clarity. Pull all three reports, save copies, list every negative item, and note which items are tied to old collections. Do not assume that the score app is showing every detail. The full report is where account status, dates, and bureau differences become clearer.

This is also the time to stop avoidable damage. Keep current accounts paid on time, avoid unnecessary applications, and review credit card balances before statement closing dates. A good first month is quiet, organized, and focused.

For help understanding bureau differences, use BNPL late payment reporting support. For a broader process, review credit repair for apartment approval.

Days 31-60: choose targeted actions

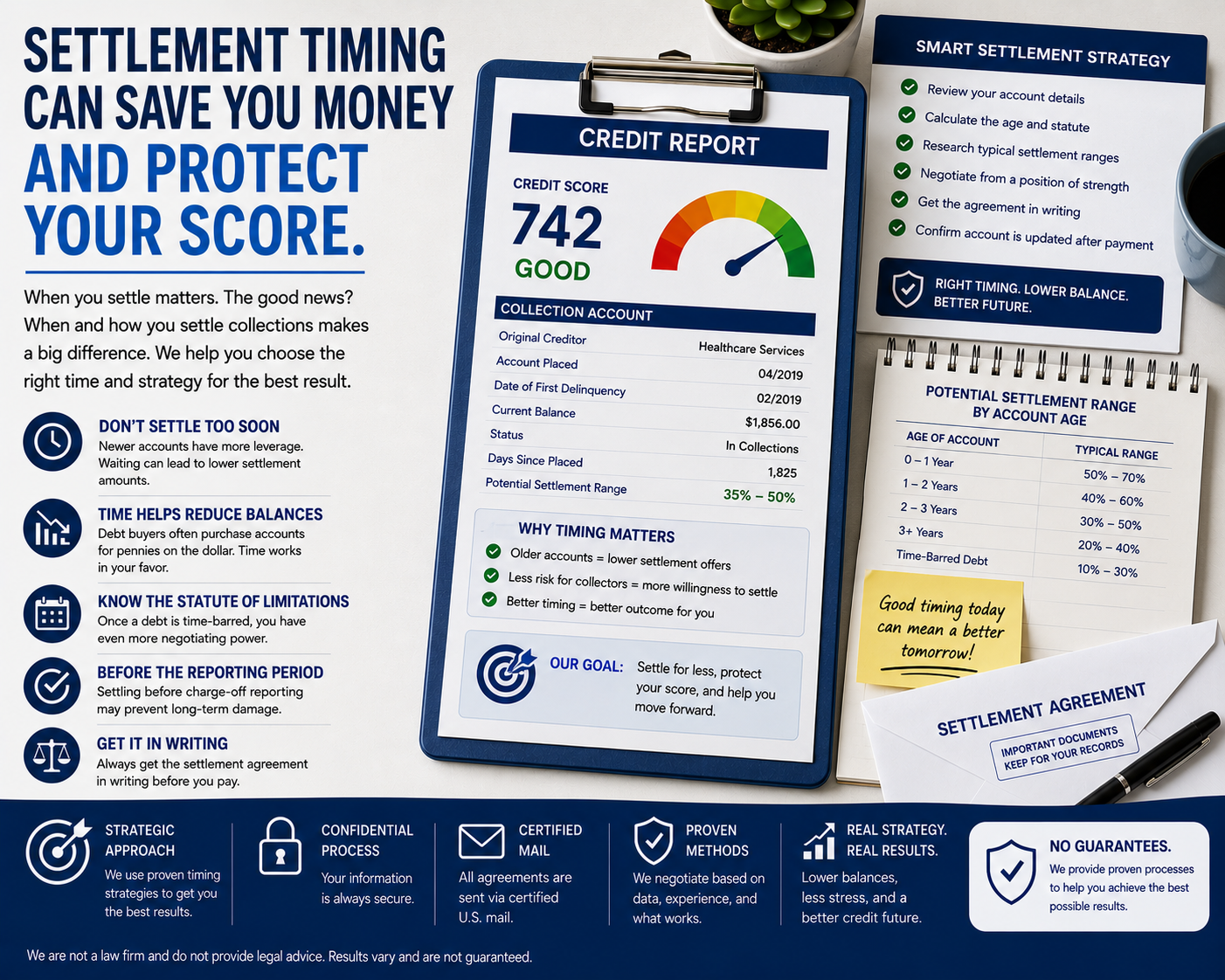

The second stage is where action becomes more selective. If an item is inaccurate, the dispute should identify the specific problem and the supporting evidence. If an account is accurate but unresolved, the consumer may need to evaluate payment, settlement, or explanation based on the approval goal.

This is also when utilization can start to improve the file if balances are lowered before the right reporting dates. When USDA loan readiness is coming soon, balance timing may matter as much as the dollar amount.

Files with collection ownership questions may need to compare LVNV Funding reporting review or Jefferson Capital Systems collection guidance with the account details on the report.

Days 61-90: verify updates before applying

The third stage is verification. Do not assume that a bureau, collector, or creditor updated everything correctly. Check whether balances changed, statuses updated, remarks appeared, disputes were marked, duplicate accounts remained, or dates moved unexpectedly.

For USDA loan readiness, this is where the application decision starts to become more realistic. If the file is still changing, it may need more time. If the major issues are documented and current balances are improved, the consumer may have a cleaner basis for the next conversation.

Mortgage-focused consumers should compare their progress with three-bureau credit report review; renters can compare with what happens after a credit repair consultation.

Days 91-180: build a file that holds up

A longer runway gives the consumer time to build more than a dispute trail. It allows fresh on-time payments, lower balances, less application activity, better savings, and cleaner documentation. Those details can matter when a lender or landlord wants proof that the file is not only cleaned up but also stable.

If old collections remain visible, the surrounding file should be as strong as possible. That means fewer avoidable risk signals, better organization, and a clear explanation of what has changed.

Use Affirm late payment reporting review for broader rebuilding and nationwide credit repair services when a secured card strategy fits the file.

Documentation makes the plan stronger

Documentation does not need to be complicated. It needs to be complete enough that the next step is based on proof rather than memory. Keep credit reports, collection letters, settlement offers, payment receipts, insurance explanations, police reports when applicable, identity documents when required, and any bureau responses in one place.

For old collections, document the account name, account number fragment, balance, date opened or assigned, date of first delinquency if shown, status, remarks, and whether the account appears on one bureau or all three. A clean comparison can reveal whether the issue is a true debt question, a reporting accuracy question, or both.

If the situation involves medical bills, identity concerns, or bureau mismatches, a documentation-first approach becomes even more important. Start with BNPL late payment reporting support so each bureau is reviewed separately, then connect the finding to the timing plan in credit repair for apartment approval.

Do not ignore utilization while reviewing negatives

Many consumers focus so heavily on collections and charge-offs that they miss a faster-moving part of the file: revolving utilization. High reported balances can make a file look strained even when the older negative items are being handled correctly.

Before USDA loan readiness, review each open credit card balance, limit, due date, and statement closing date. Paying a balance after the statement has already reported may not help the version of the file a lender sees. Timing matters because the reported balance can be different from the current balance inside the account portal.

A consumer working through old collections can still improve the surrounding file by lowering balances, avoiding unnecessary new accounts, and keeping all open accounts current. Use secured credit card rebuilding habits and Affirm late payment reporting review when the file needs both cleanup and rebuilding activity.

Apply when the file is easier to explain

The timing of USDA loan readiness should be matched to the credit report, not only to desire. Applying too early can mean higher costs, more conditions, a denial, or a longer explanation process. Waiting forever is not helpful either. The right timing is usually when the file has been reviewed, the most confusing items are documented, and current balances are not reporting at their worst.

If a lender has already told you what must be resolved, do not guess. Ask for the requirement in writing when possible, then compare it to the report. Some requests are about unpaid balances. Some are about dispute remarks. Some are about recent late payments. Some are about debt-to-income, not the negative item itself.

Use three-bureau credit report review for mortgage-specific preparation and credit repair for apartment approval for timing. The two should work together before the application is submitted.

A practical preparation plan

The best plan for USDA loan readiness starts with clarity. First, gather all three reports. Second, list the accounts most likely to affect the review. Third, mark whether each issue is accuracy-based, documentation-based, payment-based, utilization-based, or timing-based. Fourth, decide which items need action now and which items should wait.

The plan should also include recent positive behavior. Keep current accounts paid on time, reduce avoidable balances, avoid unnecessary applications, and keep bank, employment, housing, and payment records organized when a lender or landlord may request them.

When professional support is needed, review mortgage approval credit repair planning and common credit repair questions to understand service structure and expectations. The strongest credit repair process is realistic, document-driven, and matched to the consumer’s actual approval goal.

Common questions

Can old collections stop USDA loan readiness?

They can affect the review, but the impact depends on age, status, balance, bureau consistency, recent payment behavior, and the reviewer involved. Some files need correction, some need documentation, and some need more rebuilding time.

Should I dispute before I pay?

Not always. If the reporting appears inaccurate, incomplete, outdated, duplicated, or tied to the wrong person, documentation and dispute planning may come first. If the account is accurate and a lender requires it to be resolved, payment or settlement timing may become part of the plan. Written terms matter.

Will paying a collection automatically remove it?

Payment can update the account, but it does not automatically erase the history. After payment or settlement, the report should still be checked to make sure the balance, status, and dates are reported correctly.

How early should I prepare before applying?

More time usually gives the file room to update, but the right timeline depends on the report. A consumer with high utilization, active collections, or documentation problems may need more runway than someone with one older issue and strong recent payment history.

What is the safest first step?

Start with a three-bureau review and a clear list of priorities. If you need help deciding what should happen first, compare the file with rebuild damaged credit and build the plan from documentation rather than guesswork.

The strongest preparation for USDA loan readiness is a calm, documented file: accurate reporting where corrections are supported, lower avoidable balances where possible, clean recent payment behavior, and a timeline that fits the application. Outcomes vary by file, bureau response, creditor reporting, lender standards, and consumer follow-through, so the plan should stay realistic and evidence-based.

When professional review may help

A consumer can do a great deal alone by saving reports, comparing bureaus, and keeping payment records. Professional review may help when the file has several moving parts at once: old collections, high utilization, possible duplicate reporting, recent late payments, and an application goal that cannot afford random decisions.

The useful review is not a scare tactic. It should identify what appears inaccurate, what is already documented, what may need more proof, and what should be left alone until the timing is right. For USDA loan readiness, a quiet, organized plan is usually better than sending the same dispute language to every account.

The consumer should also understand the limits. Credit repair is not a promise of a specific score, a promised approval, or a fixed timeline. It is a process of report review, supported challenges when the facts justify them, and practical rebuilding steps that make the file easier to understand over time.

When professional review may help

A consumer can do a great deal alone by saving reports, comparing bureaus, and keeping payment records. Professional review may help when the file has several moving parts at once: old collections, high utilization, possible duplicate reporting, recent late payments, and an application goal that cannot afford random decisions.

The useful review is not a scare tactic. It should identify what appears inaccurate, what is already documented, what may need more proof, and what should be left alone until the timing is right. For USDA loan readiness, a quiet, organized plan is usually better than sending the same dispute language to every account.

The consumer should also understand the limits. Credit repair is not a promise of a specific score, a promised approval, or a fixed timeline. It is a process of report review, supported challenges when the facts justify them, and practical rebuilding steps that make the file easier to understand over time.

When professional review may help

A consumer can do a great deal alone by saving reports, comparing bureaus, and keeping payment records. Professional review may help when the file has several moving parts at once: old collections, high utilization, possible duplicate reporting, recent late payments, and an application goal that cannot afford random decisions.

The useful review is not a scare tactic. It should identify what appears inaccurate, what is already documented, what may need more proof, and what should be left alone until the timing is right. For USDA loan readiness, a quiet, organized plan is usually better than sending the same dispute language to every account.

The consumer should also understand the limits. Credit repair is not a promise of a specific score, a promised approval, or a fixed timeline. It is a process of report review, supported challenges when the facts justify them, and practical rebuilding steps that make the file easier to understand over time.

When professional review may help

A consumer can do a great deal alone by saving reports, comparing bureaus, and keeping payment records. Professional review may help when the file has several moving parts at once: old collections, high utilization, possible duplicate reporting, recent late payments, and an application goal that cannot afford random decisions.

The useful review is not a scare tactic. It should identify what appears inaccurate, what is already documented, what may need more proof, and what should be left alone until the timing is right. For USDA loan readiness, a quiet, organized plan is usually better than sending the same dispute language to every account.

The consumer should also understand the limits. Credit repair is not a promise of a specific score, a promised approval, or a fixed timeline. It is a process of report review, supported challenges when the facts justify them, and practical rebuilding steps that make the file easier to understand over time.

When professional review may help

A consumer can do a great deal alone by saving reports, comparing bureaus, and keeping payment records. Professional review may help when the file has several moving parts at once: old collections, high utilization, possible duplicate reporting, recent late payments, and an application goal that cannot afford random decisions.

The useful review is not a scare tactic. It should identify what appears inaccurate, what is already documented, what may need more proof, and what should be left alone until the timing is right. For USDA loan readiness, a quiet, organized plan is usually better than sending the same dispute language to every account.

The consumer should also understand the limits. Credit repair is not a promise of a specific score, a promised approval, or a fixed timeline. It is a process of report review, supported challenges when the facts justify them, and practical rebuilding steps that make the file easier to understand over time.