Collection Accounts After Settlement: What To Check Once the Payment Clears

Collection accounts after settlement can create confusion because the account may involve an original creditor, a collector, a debt buyer, a service company, or several bureau updates over time. The goal is to slow the decision down, read the reporting carefully, and build a plan that protects post-settlement review.

Timing changes the entire strategy. A consumer who has six months before applying for a mortgage can move differently than someone already sitting in a lender’s portal. When collection accounts after settlement is involved, the plan should match the 30, 60, 90, and 180 day window.

That does not mean rushing into payment or sending a vague dispute. It means sequencing the file: confirm the facts, protect documentation, address reporting errors where supported, stabilize utilization, and avoid new mistakes while the account is under review.

This post is built for consumers who want a practical path. It explains how to review settled accounts that still report incorrectly, inconsistently, or in a way that confuses lenders, what to save, how payment timing can affect the next review, and why rebuilding current credit behavior matters at the same time. It also connects related guides such as Jefferson Capital Systems collection guidance and three-bureau report review when those topics overlap.

Quick review checklist

- Save current Equifax, Experian, and TransUnion reports before taking action.

- Compare the collector name, original creditor, balance, status, and dates across all bureaus.

- Separate accuracy problems from payment decisions so the next step is not rushed.

- Keep settlement offers, payment proof, letters, and bureau responses in one folder.

- Review current utilization and late-payment risk while the collection issue is being handled.

- Match the strategy to the approval goal: mortgage, auto, apartment, refinance, or rebuilding.

A practical 30/60/90/180 day sequence

The first 30 days should be about building the file map. Pull all three reports, save PDFs, list each collection or charge-off, identify duplicate reporting, note current utilization, and organize payment records. Do not rely on memory. The report in front of you is what lenders, landlords, and scoring models may be reacting to.

Days 31 to 60 are usually where targeted action begins. That may mean disputing inaccurate fields, requesting validation where appropriate, negotiating written settlement terms, lowering reported balances, or pausing new applications. The action should match the problem. A wrong date is not handled the same way as a valid unpaid balance.

Days 61 to 90 are about verification. Review bureau responses, compare old and new reports, check whether updated accounts are reporting correctly, and decide whether a follow-up is supported. If a collection is paid, settled, deleted, or corrected, save the proof. If nothing changed, the next step should be based on evidence, not frustration.

Days 91 to 180 should focus on stability. Keep payments current, keep utilization controlled, avoid unnecessary applications, and prepare any explanation documents needed for a lender or landlord. The broader credit repair timeline can help organize the rebuild when several accounts are moving at the same time.

Documents and reporting fields to review

The first practical step is a three-bureau comparison. Save the current Equifax, Experian, and TransUnion reports before calling, paying, settling, or disputing. Look for the collector name, original creditor, account number fragment, balance, date opened or assigned, last reported date, payment status, and any remarks. If one bureau reports a different balance or date, keep a copy of that difference.

Useful documents include credit reports, collector letters, original creditor statements, settlement offers, proof of payment, identity records, address history, and any bureau responses. For medical debt, insurance explanations of benefits and billing records may matter. For rental accounts, move-out records, lease ledgers, deposit notices, and correspondence can matter. For BNPL-related collections, account screenshots and payment history can be important; the Afterpay credit repair guide and Affirm credit repair guide examples show why small balances still need documentation.

Vague disputes are easier to verify because they do not identify the exact reporting problem. A stronger dispute focuses on a field: wrong balance, wrong status, duplicate reporting, outdated timeline, inaccurate original creditor, or identity mismatch. The goal is not to overwhelm the bureau. The goal is to make the error clear enough that the investigation can address the actual problem.

For collection accounts after settlement, do not assume every bureau is showing the same version of the account. One bureau may show a balance, another may show a different status, and another may omit the original creditor. When that happens, save the reports side by side and note the exact field that does not match.

Payment, settlement, and update timing

Payment can sometimes help when a lender, landlord, or funding source requires an unpaid collection to be resolved. But payment by itself does not guarantee removal, approval, or a score increase. A paid collection can still remain visible, and a settled account may still need review after it updates. Before sending money, get the terms in writing and understand how the account is expected to report afterward.

Settlement timing should be matched to the goal. Someone months away from applying may have time to dispute inaccuracies first, request validation where appropriate, or negotiate written terms. Someone close to an approval date may need a faster decision because the reviewer is waiting. A structured plan weighs accuracy, timing, written settlement terms, current balances, and the impact of other negative accounts.

After a payment or settlement clears, check all three reports again. Confirm whether the balance updates, whether the status changes, whether the account is marked paid or settled, whether the date fields stayed accurate, and whether any duplicate collection remains. If the reporting changes incorrectly, the new report and the old report become the comparison record.

Mortgage, apartment, and auto approval context

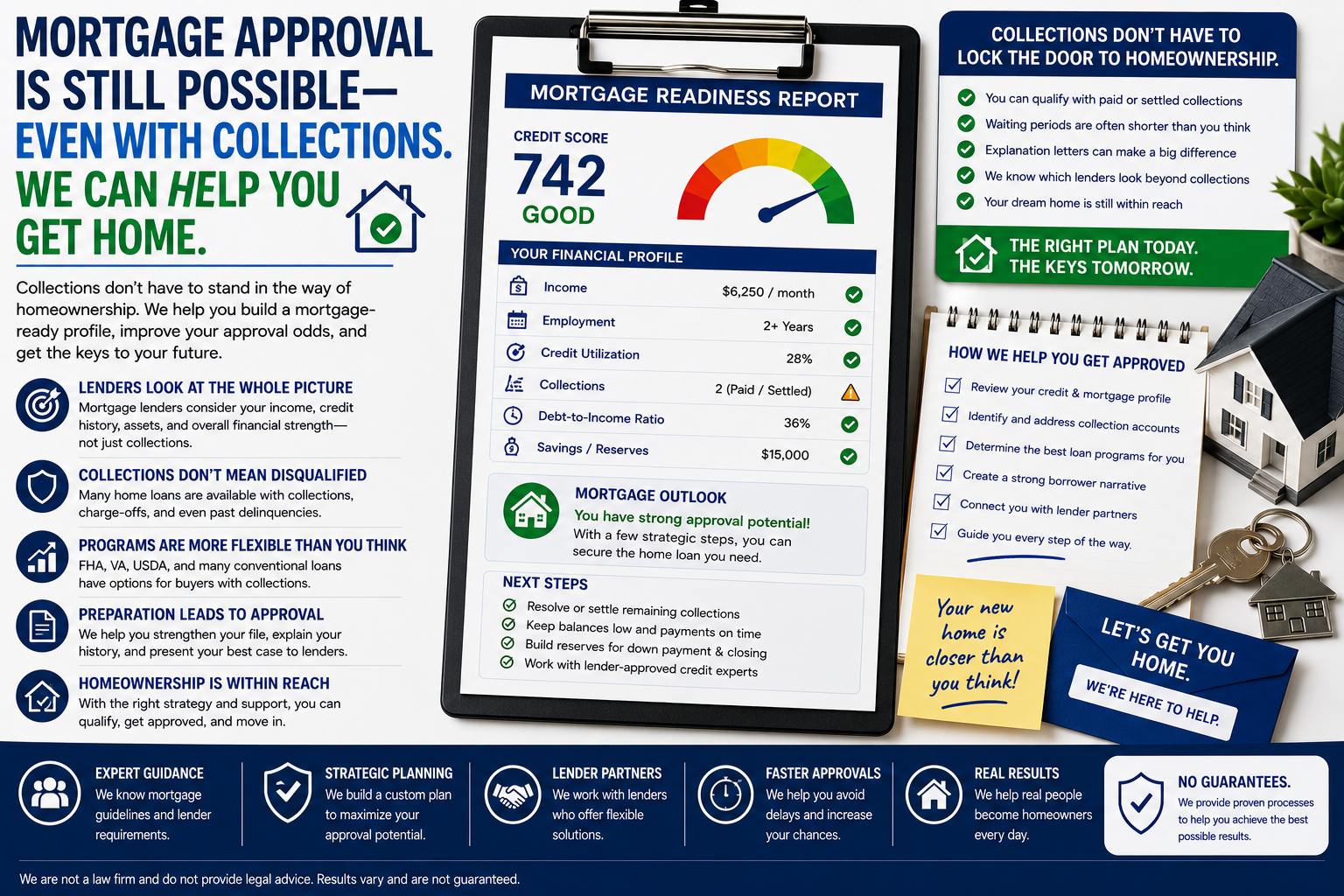

Mortgage review is document-heavy. A mortgage file may be reviewed for unpaid collections, dispute remarks, late payments, charge-offs, utilization, debt-to-income ratio, and source of funds. If a collection is disputed near underwriting, the lender may ask questions. If a collection is paid near closing, the lender may ask for proof. The plan should be coordinated before the application is in motion.

Apartment screening can be more direct. A landlord or screening company may review unpaid balances, rental-related collections, recent derogatories, identity consistency, and open obligations. A consumer preparing for a lease should keep proof organized and should address incorrect reporting before the screening window whenever possible.

Auto financing often turns on risk, income, down payment, and recent credit behavior. A collection may not automatically prevent financing, but it can affect terms, required down payment, or lender comfort. Cleaning up obvious errors and lowering current balances may matter as much as the collection decision itself.

This is also where related issues matter. A file with collections plus a repossession may need the charge-off and repossession reporting perspective. A file with medical accounts may need the medical debt credit repair perspective. A file with several unpaid collectors should still be reviewed as one connected approval picture.

Rebuilding while the account is being reviewed

Even when a collection is corrected, resolved, or removed, the file still needs positive movement. On-time payments, lower utilization, fewer unnecessary applications, and stable open accounts help show that the current file is improving. A consumer who only focuses on the negative item may miss the positive behaviors that make the next review easier.

High utilization can overpower progress on collections. If revolving cards are reporting near their limits, the score and approval picture may remain strained even after a collection update. The plan should include balance reporting dates, statement timing, and realistic payoff priorities. The guide on using secured credit cards responsibly can also support rebuilding when a file needs more positive depth.

One of the most common mistakes is opening new accounts or applying repeatedly while a credit file is already fragile. New inquiries, new balances, and new late payments can make a reviewer less comfortable. During cleanup, the safest path is usually stability: protect current payments, keep balances under control, save documents, and make each action intentional.

A cleaner file should also become a stronger file. That means reviewing whether positive open accounts are aging well, whether card balances are reporting at a manageable level, and whether the consumer is avoiding new late payments during the cleanup window. The good credit versus bad credit planning can help explain why small changes in credit strength matter over time.

Identity, mixed-file, and wrong-account concerns

If the account does not look familiar, treat it as a possible identity, mixed-file, or reporting problem before treating it as a simple unpaid debt. Compare names, addresses, partial account numbers, original creditor details, and dates. A collection that belongs to someone with a similar name, a family member, or a previous address can require a different kind of documentation.

Warning signs include addresses you never used, employers that are not yours, accounts opened in places you never lived, balances that do not match any records, and a collector tied to a creditor you never had. Mixed-file issues should be documented carefully because the dispute is about identity accuracy, not just whether the debt is inconvenient.

Identity records can include a government ID, proof of address, police or identity theft reports where appropriate, creditor correspondence, and bureau reports showing the mismatch. The goal is to help the bureau understand why the account does not belong on the file or why certain identifying information is wrong.

How reviewers may read this account

Reviewers care about collections because they can point to unresolved risk. The account might be old, but the balance, last update, dispute remark, or unpaid status can still influence how a file is read. A mortgage underwriter may ask whether an unpaid collection has to be resolved. A landlord may care more about open balances and identity consistency. An auto lender may focus on recent payment behavior and how much current revolving debt is already reporting.

The balance is only one field. A collection can also reveal whether the consumer has recently had financial stress, whether the original creditor charged off the account, whether a debt buyer now owns it, and whether the credit report tells a consistent story. That is why a smart review compares the account with current utilization, open accounts, and other derogatory items. A consumer working through collection accounts after settlement may also need a broader plan for credit repair timeline instead of focusing only on one trade line.

Approval context matters because the same collection can be treated differently by different reviewers. A small paid medical collection may not carry the same weight as a recent unpaid rental collection. A charged-off installment account may raise different concerns than a transferred credit card balance. When the goal is mortgage, auto, apartment, or business funding, the account should be evaluated through that lens before action is taken.

Common scenarios for collection accounts after settlement

Not every account fits the same path. Use the scenario closest to your file, then adjust after reviewing the documents.

- The account is unfamiliar: review identity records, addresses, and original creditor details before payment.

- The account is accurate but unpaid: decide whether settlement timing matters for an upcoming review.

- The account is paid but still negative: confirm the balance and status update correctly across all bureaus.

- The account is duplicated: compare account numbers, dates, balances, and collector names before disputing.

- The account is tied to a charge-off: review both the original creditor and the collection so the file tells one consistent story.

How to turn the review into a cleaner plan

The best plan starts with the actual report, not assumptions. If collection accounts after settlement is one part of a larger credit problem, compare it with late payments, utilization, charge-offs, repossession history, medical collections, and any active disputes. Then decide which action has the strongest documentation and the best timing.

A consumer who is months away from applying can often build a steadier sequence than someone already facing a denial. Use the credit repair results timeline to think through pacing and review clear credit repair pricing so expectations stay realistic from the beginning.

Important: credit outcomes vary by consumer file, bureau responses, creditor reporting, documentation, and lender standards. No deletions, score increases, approvals, or timelines are guaranteed. Accurate current information cannot be promised for removal.

Frequently asked questions

Can collection accounts after settlement affect mortgage approval?

It can. Mortgage reviewers may consider unpaid collections, dispute remarks, charge-offs, utilization, late payments, and file stability. The impact depends on the loan program, the lender, and the rest of the credit profile.

Will paying a collection remove it from my credit report?

Payment does not guarantee removal. A paid or settled collection can still remain visible. After payment, review all three reports to confirm the status and balance update correctly.

What if this collection is not mine?

Treat it as a possible identity, fraud, or mixed-file problem. Save reports, identity records, address history, letters, and any records showing why the account does not match you.

How long should I keep collection documents?

Keep the documents for the entire reporting and approval planning period. Old reports, settlement terms, payment confirmations, and bureau responses can matter if the account changes later.

Can a collection be corrected or removed?

It may be corrected or removed if the reporting is inaccurate, incomplete, outdated, duplicated, or not properly verifiable. Accurate current information cannot be promised for deletion.

Should I dispute every negative account at once?

No. A stronger plan prioritizes the accounts with clear reporting problems, approval impact, and documentation support. Unsupported mass disputes can create confusion and weak follow-up.

Can this affect apartment approval?

Yes. Many screening processes review open collections, unpaid rental balances, recent derogatories, and identity consistency. Organize proof before the application window when possible.