A lot of people start researching voluntary repossession at the same point. The car payment has become too much. Maybe income dropped, expenses went up, or a temporary setback lasted longer than expected. You want to avoid a surprise tow truck, avoid extra chaos, and handle the situation responsibly.

For many families, that feels like the least harmful option. Hand the car back, stop the monthly payment, and move on.

But if you're asking how bad is a voluntary repossession, especially because you still want to buy a home later, the honest answer is this: it's a serious negative event. It can affect your credit, leave you with remaining debt, and create extra mortgage hurdles long after the car is gone. The good news is that it doesn't make recovery impossible. It does mean you need clear expectations and a careful plan.

Table of Contents

- Facing a Difficult Car Loan Decision

- What a Voluntary Repossession Actually Means

- The Immediate Impact on Your Credit Score and Report

- Long-Term Consequences Beyond the Score Drop

- How a Repossession Affects Mortgage Approval

- Alternatives to Consider Before Surrendering Your Vehicle

- Rebuilding Your Credit for Homeownership After a Repossession

- Start with the issues that still affect mortgage approval

- Work on the parts of the credit profile you can improve

- How credit repair fits, and where its limits are

- Rebuilding with FHA, VA, and Conventional financing in mind

- Frequently asked questions

- Can a voluntary repossession stop me from getting a mortgage?

- Is voluntary repossession better than an involuntary repo for my credit score?

- How long does a voluntary repossession stay on my credit report?

- Do I still owe money after giving the car back?

- Can credit repair remove a voluntary repossession?

Facing a Difficult Car Loan Decision

A common situation looks like this. A couple bought a vehicle when work was steady and the payment fit the budget. Then overtime disappeared, daycare went up, groceries cost more, and the car note became the bill that no longer fits. They don't want to ignore the lender. They're trying to avoid embarrassment, towing fees, and a scene in the driveway.

That's why voluntary repossession appeals to people who are under pressure but still trying to act responsibly. It sounds more controlled than waiting for the lender to take the vehicle. In a narrow sense, that's true. You may get to choose the time and place. You may avoid some towing or storage issues. If you're trying to understand related auto risk decisions before things get worse, this guide on when gap insurance is a smart buy can help explain why some borrowers still owe money even after a vehicle is gone.

The hard part is that voluntary surrender is still a default on the loan. Lenders and credit scoring systems don't treat it as a harmless reset. They treat it as a serious sign that the loan was not repaid as agreed.

Practical rule: Voluntary repossession can feel more organized than an involuntary repo, but it isn't a clean exit from the debt or the credit consequences.

For first-time homebuyers, renters planning to buy, and families preparing for FHA, VA, USDA, or conventional mortgage approval, that difference matters. You're not just deciding what to do about a car. You're deciding what kind of credit file a mortgage lender will review later.

What a Voluntary Repossession Actually Means

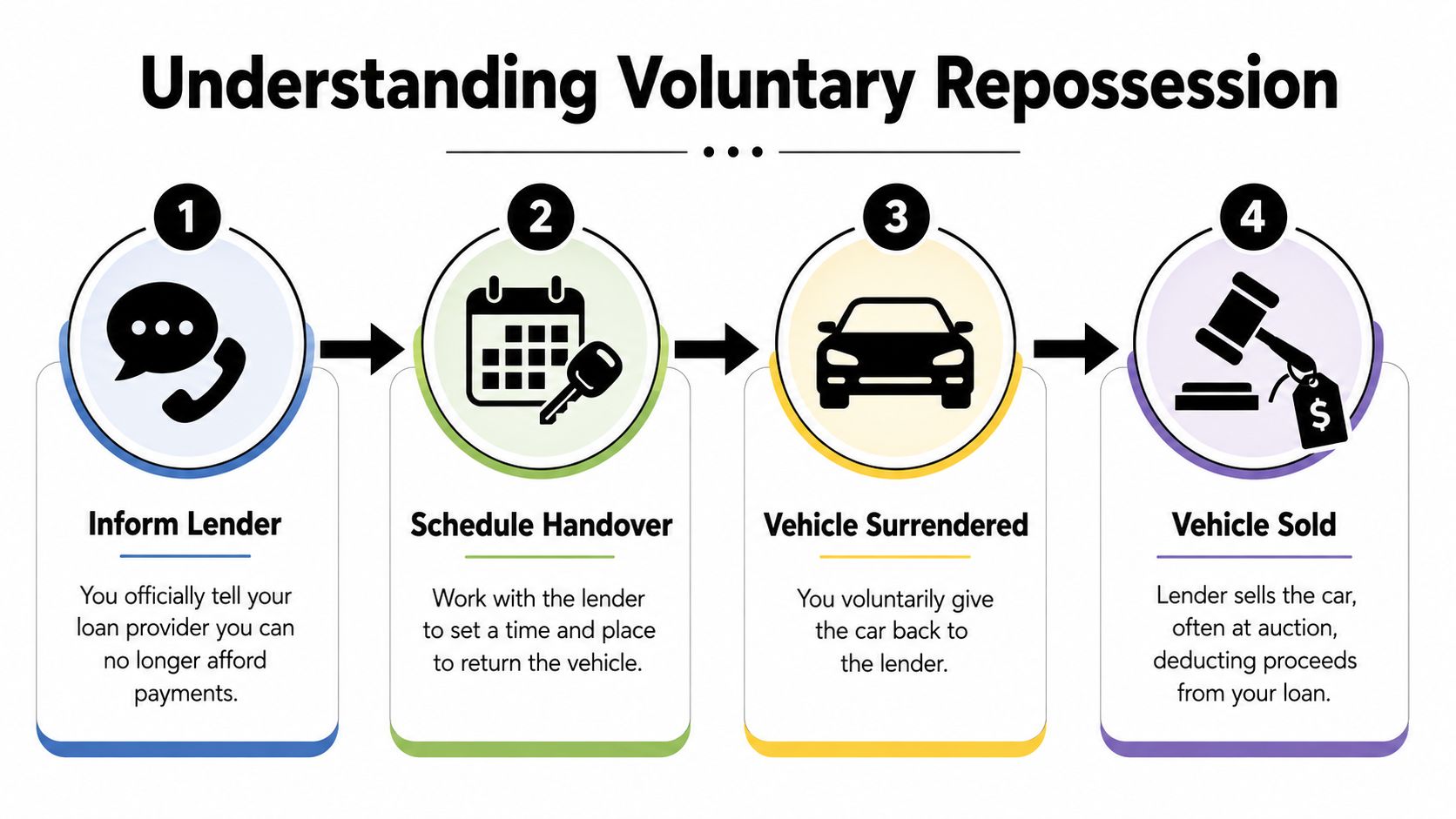

A voluntary repossession happens when you tell the lender you can't keep making payments and arrange to return the vehicle. You're not waiting for a tow truck or a recovery agent. You're initiating the handoff.

That sounds cooperative, and in a practical sense it is. But legally and financially, the loan still failed. The lender still has a defaulted account. The credit report still reflects severe negative history.

How the process usually works

In plain English, the process usually follows a simple pattern:

- You contact the lender and say you can't continue the payments.

- You arrange a return at a set time and place.

- You surrender the vehicle and any required documents or keys.

- The lender sells the vehicle, often through auction, and applies the proceeds to the loan balance.

A practical benefit does exist. As noted by DebtStoppers, “While a voluntary repossession may allow a debtor to return the vehicle at a specific location and time to avoid towing or storage fees, it does not erase the loan debt or prevent the account from showing serious negative history on the credit report prior to the surrender.” You can review that explanation in their article on voluntary repossession pros and cons.

If you're sorting through ownership and title issues before making any decision, it can also help to check lien status with VekTracer. Many borrowers don't fully understand who holds the lien, what interest is recorded, or what has to happen before a vehicle can be sold or surrendered.

For a deeper look at managing credit after voluntary surrender, it helps to separate the emotional relief of returning the car from the financial reality that follows.

Why the debt often doesn't end

This is the part that confuses people most. Returning the car does not mean the account is settled in full.

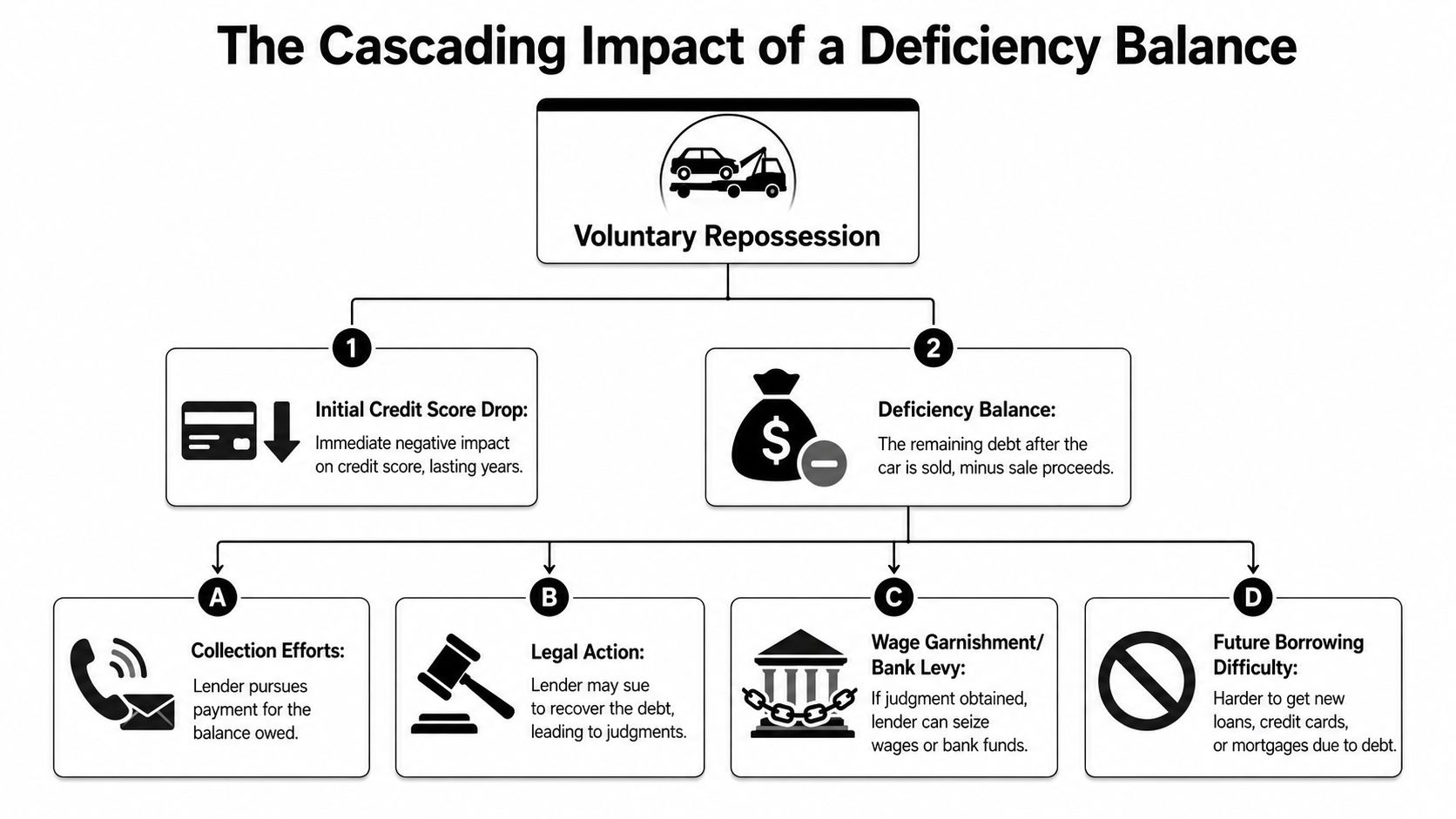

If you owe more on the loan than the lender recovers from the sale, the unpaid part doesn't disappear. That remaining amount is called a deficiency balance. You no longer have the car, but you may still owe part of the debt.

The surrender ends your possession of the vehicle. It doesn't automatically end your financial responsibility for the loan.

That's why voluntary repossession should never be viewed as a mutual cancellation agreement. It is better understood as an organized return of collateral after default.

The Immediate Impact on Your Credit Score and Report

The first direct consequence is credit damage. That damage usually starts before the surrender itself because most borrowers have already missed payments by the time they return the vehicle.

How it appears on your credit report

Credit reports may show the event with wording such as voluntary surrender instead of repossession. That label can create false comfort. It may give context to a human reader, but it does not meaningfully soften how the event is calculated in standard credit scoring.

ScoreSense explains that a voluntary surrender notation may appear on the tradeline, but it does not meaningfully change the calculated credit score or reduce the severity of the negative mark compared with an involuntary repossession in its discussion of how a voluntary repossession affects credit.

Missed payments leading up to the surrender also matter. If you want to understand why the damage often starts before the repo line appears, review the effects of late payments on credit scores. Many people focus only on the surrender date and overlook the earlier delinquency pattern that lenders can already see.

How much your score can drop

According to Credit Acceptance, a voluntary repossession causes a credit score drop of approximately 50 to 150 points, remains on the credit report for seven years, and its voluntary nature does not meaningfully change the calculated credit score or reduce the severity of the negative mark compared to an involuntary repossession in its guide on the effect of voluntary repo.

That range is significant. People with stronger credit profiles often see the biggest numerical drop because they have more room to fall. The event is still classified as a serious derogatory item.

A few practical points help explain why this hurts so much:

- Missed payments pile on first. By the time surrender happens, the account may already show late history.

- The repossession entry adds another severe negative mark. It tells future lenders the loan ended in default.

- The reporting timeline is long. The account can stay on the report for seven years from the original delinquency that led to the repo, not just from the date you handed over the keys.

| Credit report issue | Why it matters |

|---|---|

| Missed payments | Damages payment history before the surrender |

| Voluntary surrender notation | Shows the account ended in default |

| Seven-year reporting period | Keeps the event visible to future lenders for a long time |

For anyone asking how bad is a voluntary repossession, this is the short credit answer. It's one of the more serious negative events that can appear on a consumer credit report.

Long-Term Consequences Beyond the Score Drop

The score drop gets attention first because it's visible. The longer-lasting problem is what happens after the lender sells the car.

What happens after the lender sells the car

Once the vehicle is surrendered, the lender usually sells it and applies the sale proceeds to the loan. If the proceeds don't cover what you owed, plus any allowed costs, the unpaid amount remains your responsibility.

That unpaid amount is the deficiency balance. It's often the second wave of damage because borrowers assume the surrender closed the account completely.

Here's the practical chain of events many people face:

- The original auto loan shows serious default history on the credit report.

- A remaining balance is still owed after the sale.

- The lender may try to collect it directly.

- The account may be assigned or sold to collections, creating another negative account.

A borrower can end up dealing with two separate problems. One is the repo history itself. The other is a collection account tied to the unpaid deficiency.

Why the problem can keep growing

The financial pressure doesn't always stop with collections calls or letters. If the balance remains unpaid, the creditor or a collector may pursue legal action depending on the account, the documents, and the laws that apply.

That can create new stress at exactly the wrong time, especially if you're trying to become mortgage-ready, rent a new apartment, or qualify for better auto financing later.

Unpaid deficiency debt can follow the repossession and keep affecting borrowing decisions after the vehicle is long gone.

The practical consequences often include:

- Future borrowing gets harder because lenders see unresolved debt.

- Apartment approval and rental screening can become tougher when unpaid collections appear.

- Insurance costs may rise because some insurers view severe credit problems as added risk.

- Mortgage underwriting becomes more complicated if the deficiency remains open or unpaid.

This is why a voluntary repossession isn't just one event. It can become a chain reaction. The surrendered vehicle is only the first step. The deficiency balance is often the issue that keeps the problem alive.

How a Repossession Affects Mortgage Approval

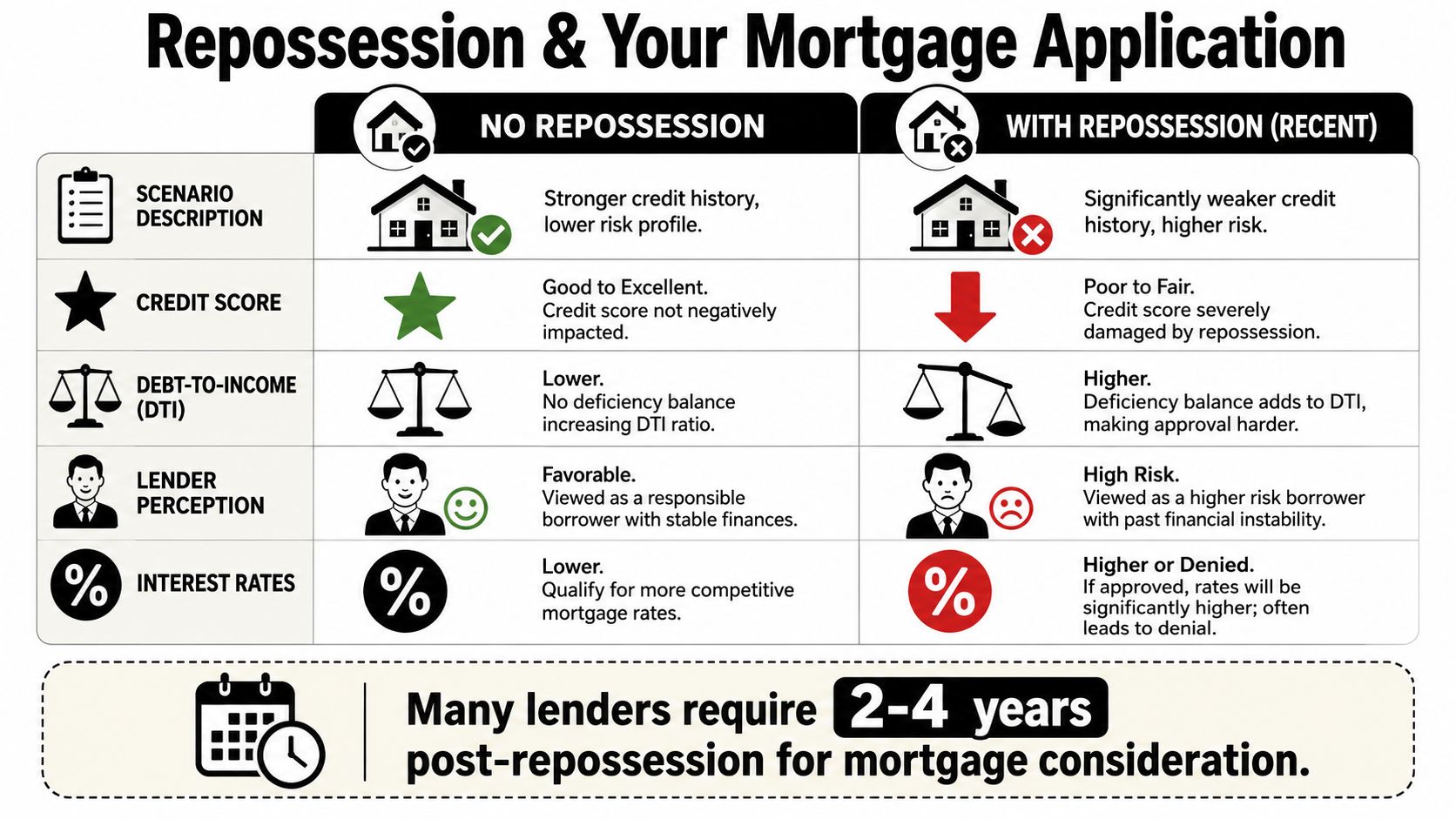

A borrower can be current on rent, save a down payment, and still hit a wall with mortgage approval because of an old car repossession. The problem is not limited to a lower credit score. Mortgage underwriting looks at whether the repo created unpaid debt, whether that debt must be resolved before closing, and whether any payment plan now takes a slice of monthly income that could have gone toward a house payment.

FHA compared with conventional financing

For homebuyers, the main question is usually not "Can I ever get approved?" It is "Which loan program gives me the clearest path, and how much house will I still qualify for?"

That distinction matters.

As noted in an Experian review of how vehicle repossession can affect mortgage approval, FHA may allow approval after a repossession if the deficiency balance is paid or the borrower is on a documented payment plan with at least three on-time payments. Conventional financing can be less flexible because collection accounts tied to a deficiency often must be paid before closing.

Here is the practical difference:

| Loan path | How repo-related debt can affect approval |

|---|---|

| FHA | Approval may still be possible if the deficiency is paid, or if a documented payment plan is established and seasoned with on-time payments |

| Conventional | Deficiency-related collections often need to be resolved before closing, which can delay or block approval |

The payment-plan issue is where many buyers get surprised. Mortgage lenders calculate your debt-to-income ratio, or DTI, by comparing required monthly debt payments to gross monthly income. A repo deficiency payment works like adding another weight to one side of the scale. Even if the payment seems manageable on its own, it can reduce the amount of mortgage payment the lender will allow.

That can lower purchasing power. Experian gives an example showing that a borrower who qualifies for one price range before the added payment may qualify for a lower range once that payment is counted in DTI. The exact impact depends on income, other debts, taxes, insurance, and the loan program, but the basic rule is simple. More required monthly debt usually means less room for the house payment.

If you are trying to clean up your file before applying, it helps to understand what underwriters review before you prepare for mortgage approval.

What this means for VA and USDA borrowers

VA and USDA borrowers often want a fixed waiting period after a voluntary surrender. In practice, the better question is whether the overall file now meets lender and program standards.

Available guidance does not give a single universal seasoning rule that clearly separates voluntary surrender from involuntary repossession in every case. Lenders usually look at the full credit picture instead. That includes whether the deficiency is still open, whether there are collections, how recent the delinquency was, and whether the borrower has re-established steady payment history since then.

For VA and USDA applicants, the safest approach is straightforward:

- resolve repo-related deficiency debt when possible

- document any payment arrangement clearly

- keep all current accounts paid on time

- lower revolving credit balances where you can

- avoid taking on new debt before the mortgage application

A repossession does not automatically end the path to homeownership. It does mean the mortgage file needs to show cleaner debt management, stronger payment history, and enough income left over to support the home payment the borrower wants.

Alternatives to Consider Before Surrendering Your Vehicle

If you haven't given the car back yet, pause before assuming surrender is your only option. In many cases, the least damaging move is the one that prevents the repo from happening at all.

Options that may reduce the damage

Start with the lender. Some borrowers avoid repossession by asking for short-term relief, a payment change, or another workout option. The lender may say no, but asking early is usually better than calling after the account is already far behind.

A private sale can also be worth exploring. It can sometimes produce a better result than letting the lender sell the vehicle after surrender. The goal is simple. If the sale covers more of the loan, you may reduce or avoid a deficiency balance.

Other options may include:

- Refinancing the auto loan if your credit is still in shape to qualify.

- Trading into a more affordable vehicle if the numbers improve your monthly budget.

- Having another qualified buyer take over the obligation, where legally and contractually possible. If that path is worth exploring, read more about how to transfer car loan to another person.

- Reviewing your full monthly budget to identify whether the car payment problem is temporary or permanent.

A short comparison can help:

| Option | Main goal |

|---|---|

| Work with lender | Avoid default and preserve credit history if possible |

| Private sale | Reduce the chance of a deficiency balance |

| Refinance | Lower payment or change term |

| Transfer or replacement strategy | Move into a more sustainable vehicle situation |

None of these options is easy. But if one of them prevents a repossession from hitting your credit report, the long-term payoff can be substantial.

Rebuilding Your Credit for Homeownership After a Repossession

A repossession does not end the path to buying a home. It changes the timeline, the paperwork, and the margin for error.

A good way to view recovery is this. Your mortgage profile is a four-part picture: payment history, debt levels, cash reserves, and time since the negative event. The repossession sits in one corner of that picture. You usually cannot erase that corner overnight, but you can strengthen the other three.

Start with the issues that still affect mortgage approval

Begin by checking whether the auto loan still has unfinished business attached to it. If the lender sold the car for less than you owed, the remaining amount is called a deficiency balance. For a future mortgage application, that balance matters in two separate ways. It can hurt your credit report if it is reported incorrectly or sent to collections, and it can affect debt-to-income ratio if you are making monthly payments on it.

That second point often gets missed by homebuyers.

A mortgage underwriter does not look only at your score. They also ask a simple math question: after counting your monthly debts, is there enough room in your budget for the new house payment? If a deficiency balance adds even a modest monthly obligation, your maximum home payment may shrink. That can reduce purchasing power, especially for FHA and conventional borrowers who are already close to program debt ratio limits.

So the first job is clarity. Review the repossession paperwork, confirm the balance, verify who owns the debt now, and make sure the account is being reported accurately.

Work on the parts of the credit profile you can improve

Credit recovery after a repossession works much like rebuilding a file after any major derogatory event. The negative mark may remain for years, but newer positive behavior can gradually carry more weight.

Focus on these steps:

- Bring all open accounts current and keep them current. A repossession followed by fresh late payments tells a lender the problem is ongoing, not isolated.

- Reduce revolving card balances where possible. Lower credit card utilization can help scores and can also improve debt-to-income flexibility if you are making large monthly card payments.

- Add new credit cautiously, only if it serves a purpose. A secured card or a small starter account can help rebuild positive history if you use it lightly and pay on time.

- Limit unnecessary credit applications. Multiple new inquiries and new accounts can make a mortgage file look unstable during the rebuilding phase.

- Build cash reserves. Savings will not remove a repossession, but reserves can strengthen a mortgage application, especially if the credit file is still recovering.

If your goal is homeownership, budget planning needs to include more than the future mortgage payment. Property taxes, insurance, and maintenance all affect affordability. Buyers in New Jersey who want to estimate ownership costs more accurately can review the Liberty Insurance guide for NJ homeowners.

How credit repair fits, and where its limits are

A voluntary repossession usually stays on the credit report unless the reporting is inaccurate, outdated, or cannot be verified. Time matters here. Accuracy matters too.

Credit repair can help by reviewing the repo account and any related collection entries for reporting problems such as:

- Incorrect balances

- Wrong delinquency dates

- Duplicate accounts

- Collection details that conflict with the original tradeline

- Inaccurate account status or remarks

That work should be document-based and specific. A proper dispute is not a generic request to remove something negative. It is a challenge to information that appears wrong, incomplete, inconsistent, or unverifiable.

For mortgage preparation, that distinction matters. A cleaned-up report with accurate balances, fewer reporting errors, and stronger current payment history gives an underwriter a more reliable file to evaluate. If you want to strengthen the foundation of your scores while preparing for a future home purchase, this guide on how to reach a 700 credit score faster explains the habits that usually matter most.

Rebuilding with FHA, VA, and Conventional financing in mind

Homebuyers often ask the wrong question first. They ask, “How many points did the repossession cost me?” A better question is, “What will an underwriter need to see before approving me for the loan program I want?”

Here is the practical difference:

- FHA borrowers often have a path back sooner if the rest of the file has stabilized. Clean recent payment history, manageable debt, and resolution of any related deficiency or collection issues can matter as much as the score itself.

- VA borrowers are also evaluated on the full credit picture, not just the repossession line by itself. Stable income, acceptable residual income, and a clear explanation of what happened can help.

- Conventional borrowers often face tighter scrutiny on overall credit quality. Lower revolving balances, fewer unresolved derogatory accounts, and stronger reserves can make a bigger difference here.

The common thread is simple. Mortgage approval after a repossession is rarely about one item in isolation. It is about whether the rest of the file now shows stability.

Frequently asked questions

Can a voluntary repossession stop me from getting a mortgage?

It can make approval harder, but it does not automatically block approval. Lenders usually look at the full file, including current credit behavior, any deficiency balance, related collections, and how the repossession affects debt-to-income ratio and cash reserves.

Is voluntary repossession better than an involuntary repo for my credit score?

In scoring terms, the difference is usually limited. A voluntary surrender may provide context in the account history, but the event is still a serious derogatory mark.

How long does a voluntary repossession stay on my credit report?

It can remain for seven years from the original delinquency date that led to the repossession.

Do I still owe money after giving the car back?

You might. If the lender sells the vehicle for less than the total loan balance and fees, the remaining amount may still be owed as a deficiency balance.

Can credit repair remove a voluntary repossession?

It may help remove or correct the item only if the reporting is inaccurate, outdated, inconsistent, or unverifiable. If the account is reported correctly, it usually remains until the reporting period ends.

Good recovery work is steady, documented, and realistic.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. If you're dealing with repossessions, collections, late payments, charge-offs, high utilization, or mortgage credit repair concerns, you can request a free credit analysis or consultation through Superior Credit Repair to better understand your options. Results vary based on your credit file, documentation, account history, creditor responses, and current credit behavior.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile. Share your feedback on Google