You found a home that fits your family, your payment estimate looks manageable, and you're finally ready to talk with a lender. Then the conversation shifts. The lender says your debt to income ratio, or DTI, is too high.

That moment catches many first-time homebuyers off guard. People often focus on credit scores, down payments, and interest rates, but underwriters spend just as much time studying whether your current monthly obligations leave enough room for a new mortgage payment. A high DTI doesn't mean you've been irresponsible. It means the numbers on paper tell the lender you may already be stretched too thin.

That can feel frustrating, especially if you're paying your bills and trying to do everything right. The good news is that DTI is not a mystery metric. It's a formula. Once you understand how lenders calculate it, you can make practical decisions that improve your mortgage readiness, whether you're preparing for FHA loan preparation, VA loan preparation, conventional mortgage approval, or USDA loan preparation.

Table of Contents

- Why Your Debt to Income Ratio Is Critical for Mortgage Approval

- Calculate Your DTI Like a Mortgage Lender

- Strategic Debt Reduction to Lower Your Ratio

- Documenting and Maximizing Your Verifiable Income

- Advanced Strategies Debt Consolidation and Credit Repair

- Your Lender-Ready DTI Improvement Checklist

- Frequently Asked Questions About DTI Ratios

Why Your Debt to Income Ratio Is Critical for Mortgage Approval

A common homebuyer story goes like this. Someone has a steady job, enough saved to start looking, and a decent idea of what monthly mortgage payment feels affordable. Then underwriting reviews the file and sees student loans, a car payment, credit card minimums, and maybe a personal loan or child support obligation. The lender isn't judging the person. The lender is judging whether the monthly budget can safely absorb one more major payment.

That is why DTI matters so much. It shows how much of your gross monthly income is already committed to debt. From a lender's perspective, this is a risk screen. If too much income is already spoken for, there is less room for a mortgage, property taxes, homeowners insurance, and the normal surprises that come with owning a home.

Why lenders look at DTI so closely

Mortgage underwriting is built on consistency and documentation. Credit scores tell lenders part of the story, but DTI tells them whether your income can carry your current obligations plus the new loan. That's especially important for first-time buyers dealing with high credit utilization, collections before mortgage approval, or recent financial recovery after divorce, hardship, or missed payments.

Practical rule: DTI is not a personality test. It's a monthly cash-flow test.

Lenders also separate the issue of desire from capacity. You may strongly want the house and may even have a down payment ready, but underwriters still need to see a payment structure that fits established guidelines. That is why many buyers who seem close to approval still get told to reduce debt first.

Why this matters before you apply

If you review DTI early, you gain options. You can pay down the right debt, delay a financed purchase, document eligible income correctly, and avoid surprises from hidden obligations. If you're preparing your file, Superior Credit Repair's homebuyer guide gives a useful overview of what underwriters study beyond just a credit score.

For many borrowers, learning how to lower debt to income ratio is one of the most practical mortgage credit repair steps they can take before applying.

Calculate Your DTI Like a Mortgage Lender

Lenders don't estimate DTI casually. They calculate it from documented monthly obligations and documented gross income. If you want a realistic picture of where you stand, use the same lens they use.

The basic formula is straightforward. The debt-to-income ratio is calculated by dividing total monthly debt payments, including mortgage, auto loans, credit card minimums, student loans, and child support, by gross monthly income before taxes and multiplying by 100. Lenders generally prefer a DTI under 36%, and 43% or less is an ideal benchmark for mortgage approval according to this explanation of DTI calculations.

What counts in the formula

For mortgage review, think in two layers.

Front-end DTI focuses on housing costs. This usually includes the projected mortgage payment and housing-related obligations the lender uses for qualification.

Back-end DTI includes housing plus other recurring debts. This is the ratio commonly referred to when discussing a high DTI problem.

Include these monthly debts when you calculate:

- Mortgage-related housing payment: Use the expected full housing payment your lender is evaluating.

- Auto loans: Count the required monthly payment, not what you hope to pay extra.

- Student loans: Use the payment the lender will recognize for underwriting.

- Credit card minimums: Count the minimum required payment on each card.

- Child support or similar obligations: Include court-ordered recurring obligations.

What usually does not go into DTI in the same way are ordinary living expenses like groceries, utilities, gas, or streaming subscriptions. Those costs matter to your real-life budget, but they are not typically the same as the contractual debt items underwriters place in the formal DTI formula.

If you want more background on lender terminology, this guide on debt to income ratio for homebuyers can help you compare your own numbers to mortgage expectations.

A simple example using lender math

Let's keep the math simple and realistic without turning this into a spreadsheet exercise.

Suppose your gross monthly income is $3,500. Your projected housing payment is $1,500, your student loans are $300, and your car loan is $100. Your total monthly debt is $1,900. Using the standard formula, your DTI is ($1,900 ÷ $3,500) × 100 = 54%. That example appears in the Experian guidance referenced in the background materials.

That number tells a lender something important. Too much of your monthly income is already committed before the mortgage file is even approved.

When buyers say, "But I can afford it," underwriters reply with paperwork, not optimism.

Front-end and back-end targets

You'll often hear the 28/36 rule. In plain language, that means many conventional lenders prefer a front-end ratio under 28% and a back-end ratio under 36%. Some programs can allow more flexibility, but those lower thresholds are still important because they often reflect the difference between a borderline file and a stronger one.

If your current back-end DTI is above that comfort range, don't panic. It means your next step is to decide whether reducing debt, documenting more qualifying income, or correcting inaccurate account information would improve the file most effectively.

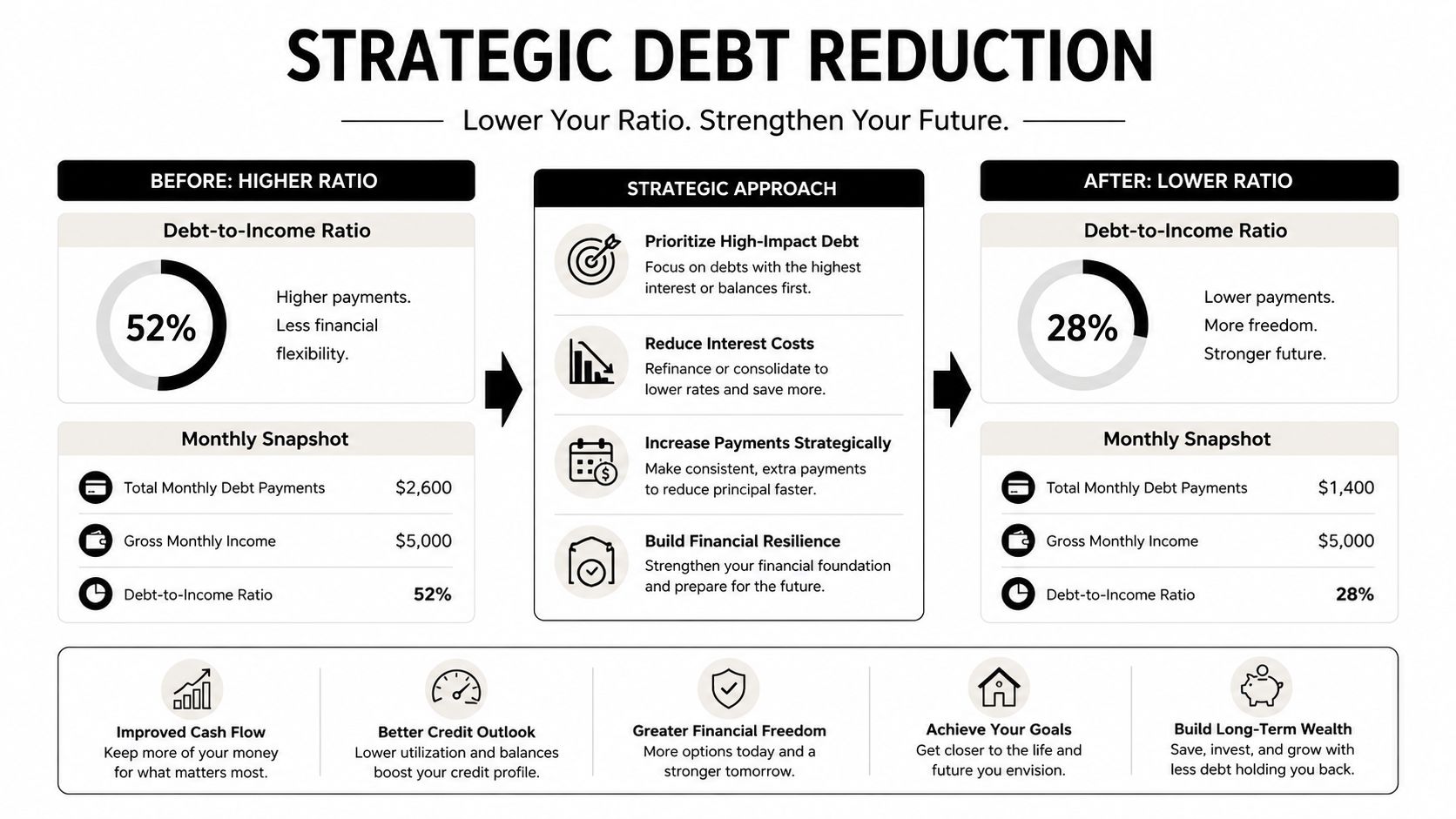

Strategic Debt Reduction to Lower Your Ratio

Once you've done the math, the next question is practical. Which debt should you attack first if your goal is mortgage readiness?

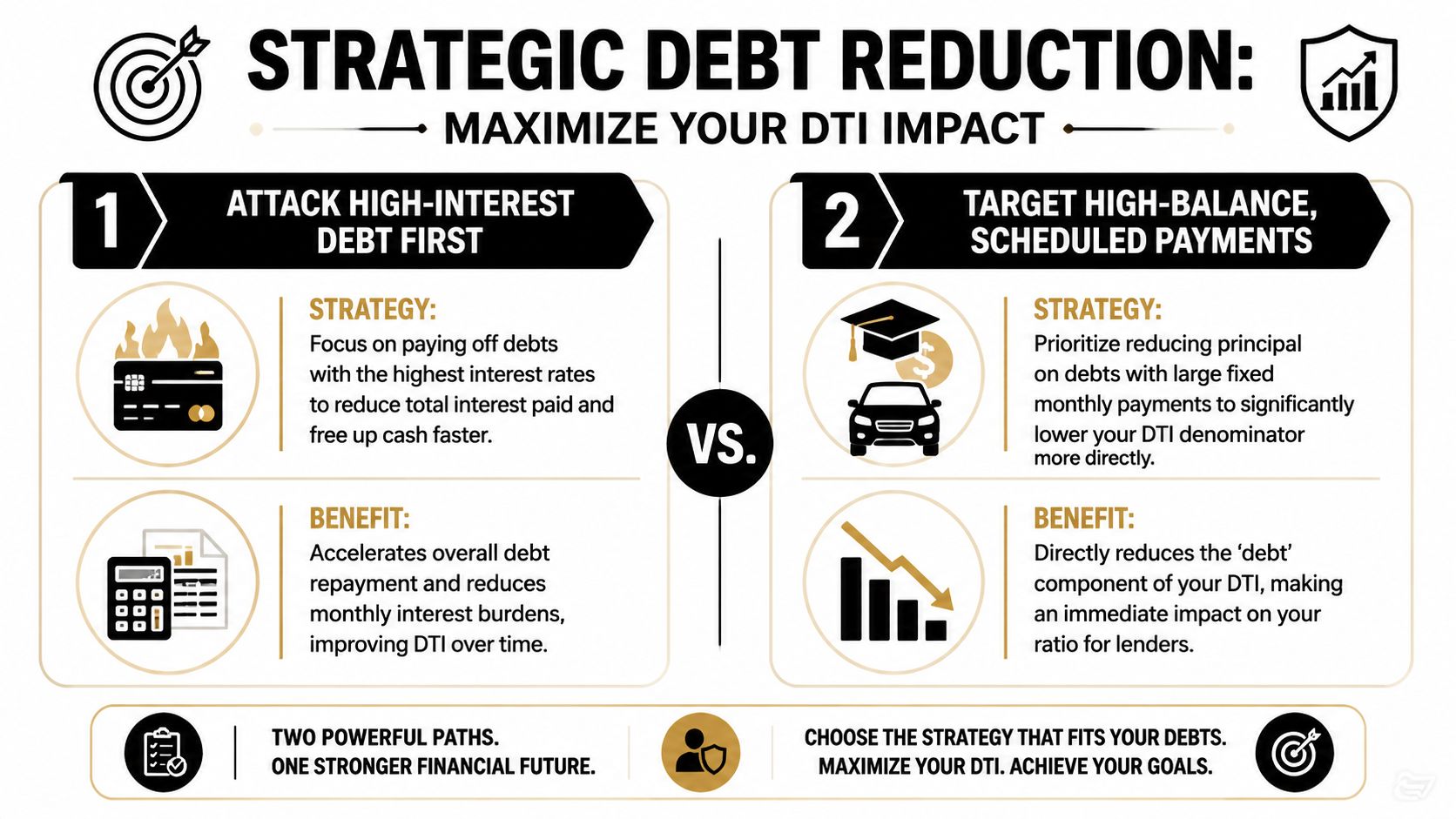

The answer isn't always "pay whatever is smallest." If your goal is emotional momentum, the debt snowball can help some people stay engaged. If your goal is the most efficient path for how to lower debt to income ratio, the debt avalanche often makes more sense.

Debt avalanche versus debt snowball

The debt avalanche method means you keep making minimum payments on all accounts, then put extra money toward the balance with the highest interest rate first. That matters because high-interest credit card balances can keep monthly obligations sticky and expensive.

According to Harvard Federal Credit Union's discussion of high DTI management, paying down high-interest credit card balances first using the debt avalanche method reduces the largest portion of monthly debt obligations most efficiently, since credit card minimums are included in DTI calculations and high rates compound debt faster.

The debt snowball method starts with the smallest balance first. That can build motivation, and motivation matters. But if you're working against a mortgage timeline, math usually deserves more weight than psychology.

A simple comparison helps:

| Method | Best for | Main tradeoff |

|---|---|---|

| Debt avalanche | Lowering cost and attacking expensive debt first | Can feel slower emotionally |

| Debt snowball | Building confidence through quick account wins | May not reduce interest burden as efficiently |

If a mortgage is your near-term goal, choose the strategy that improves the lender's view of your file, not just the one that feels satisfying.

For readers also thinking about long-term habits after approval, this resource on preventing future debt is a practical companion to short-term payoff planning.

The BNPL blind spot underwriters notice

A lot of buyers overlook Buy Now, Pay Later accounts because they don't always feel like debt in the traditional sense. Services like Affirm, Klarna, and Sezzle can blend into everyday spending and may not stand out the way a credit card statement does.

That creates a problem during underwriting. A lender may still identify recurring BNPL obligations by reviewing bank statements and transaction histories. If you have several active plans, those payments can crowd your monthly budget even if they don't feel serious one by one.

BNPL can also create confusion because borrowers sometimes assume, "If it isn't hurting my score, it won't hurt my application." That assumption can backfire. Underwriters care about documented payment obligations, not just what appears in the most obvious part of your credit file.

Which debts deserve your attention first

If you're choosing where to focus, this order is often the most useful from a lender-readiness standpoint:

- High-interest credit cards: These often combine expensive interest with utilization pressure.

- Debts with fixed monthly payments: Large required payments can make your ratio harder to defend.

- Hidden recurring plans: BNPL obligations and similar payment arrangements can drain monthly capacity.

- Any new financing temptation: Hold off on new accounts if you're trying to improve your file before buying.

If your ratios are tight and your scores also need work, learning how to boost credit for free can support the same mortgage-prep timeline without adding new debt.

Documenting and Maximizing Your Verifiable Income

Some borrowers focus only on reducing debt and miss the other half of the DTI equation. Income matters too, but only if the lender can verify it properly.

That means extra income doesn't help your mortgage file just because you know you earn it. It helps when it is stable, documented, and acceptable under underwriting rules.

Income sources lenders may count

Some applicants have income beyond base salary, such as bonuses, commissions, alimony, child support, or property income. When those sources meet lender standards, they can strengthen the denominator in your DTI formula.

According to the CFPB-related guidance provided, formally documenting and including qualified income sources beyond base salary can potentially increase gross monthly income by 10% to 30%, instantly lowering DTI. However, lenders like FHA and VA require a two-year history and tax return documentation such as IRS Form 1040, and often reject income that lacks that track record, as noted in this CFPB-linked explanation.

That two-year pattern is where many borrowers get tripped up. A new side hustle might help your household budget in real life, but if it hasn't been consistent and documented, an underwriter may not include it.

The paperwork underwriters want

Underwriters are not trying to make life difficult. They are trying to confirm that income is likely to continue and can be verified.

Gather documents such as:

- Tax returns: Especially if you receive commissions, freelance income, or other non-salary earnings.

- Pay stubs and employer verification: These help confirm current income and employment consistency.

- 1099s or similar records: Useful for independent work when applicable.

- Bank statements tied to reported income: Helpful when they support tax-documented deposits.

- Court or legal documentation: Important for support income when a lender permits it.

If you're self-employed or juggling variable income, careful record keeping matters. Even though mortgage standards in the United States differ from business record practices elsewhere, this guide to UK self-employment records is still a helpful reminder that clean documentation makes financial reviews easier.

A practical do and dont table

| Do | Don't |

|---|---|

| Keep tax filings consistent with the income you want counted | Assume cash income with no paper trail will qualify |

| Organize records before applying | Wait until underwriting to search for missing documents |

| Ask which income type your lender will recognize | Assume every deposit in your bank account counts |

| Show stable history where required | Present new gig income as if it were long-established |

Clean income documentation can lower DTI without paying off a single debt. But undocumented income usually doesn't exist in underwriting.

This matters for more than mortgages. It can affect apartment approval, rental screening, auto financing, and overall lender-ready credit profiles.

Advanced Strategies Debt Consolidation and Credit Repair

Sometimes the basic fixes aren't enough. A borrower may already be trimming balances, avoiding new debt, and organizing pay records, but still need a more structured plan. That is where debt consolidation, balance restructuring, and documentation-based credit repair can become relevant.

These tools are not magic. They can help when used carefully and can create new problems when used casually.

When consolidation helps and when it doesn't

Debt consolidation can make sense when it lowers required monthly payments and simplifies your obligations. A balance transfer or consolidation loan may also improve budgeting if you stop juggling several due dates and high-interest accounts.

But lower interest does not automatically mean lower DTI. What matters to underwriting is whether the required monthly payment becomes more manageable and whether the move creates new issues, such as fees, new credit inquiries, or temptation to run balances back up after consolidation.

A balanced way to think about it is this:

- Helpful use case: You reduce required monthly payments and keep old balances from growing again.

- Risky use case: You consolidate, then continue using available credit and end up with both old behavior and new debt.

- Compliance reality: Lenders still review the full file, not just the story you tell about the strategy.

Experian notes that for mortgage approval you should target a DTI below 50%, while conventional lenders often prefer a back-end DTI under 36%. Experian also notes that Fannie Mae's guidelines allow a DTI up to 50% for automated underwriting but may cap it at 36% to 45% for manually underwritten loans with specific credit and reserve requirements, according to Experian's loan preparation guidance.

That tells you something important. Borderline files may still work in some circumstances, but stronger files give you more room to breathe.

How credit repair fits into DTI planning

Credit repair does not erase legitimate debt. It also does not guarantee mortgage approval, score increases, or account deletion. What it can do, when handled correctly, is support a structured review of whether your reports contain inaccurate, outdated, unverifiable, or misleading information that may be affecting how lenders see your obligations.

That matters when an account balance is reported incorrectly, when a collection does not belong to you, when a charge-off is misstated, or when an old item should be reviewed for accuracy and verification. In those situations, a legal dispute and verification process may help clean up the file if documentation supports the challenge.

For homebuyers, this can be especially relevant in cases involving:

- Credit report errors: Incorrect balances or account statuses can distort your file.

- Collections dispute help: A questionable collection may require documentation review.

- Late payment dispute help: Reporting accuracy matters if the timeline or account history is wrong.

- Charge-off dispute help: Account details should match the creditor's records.

If you're trying to create a lender-ready credit profile before buying a home, reviewing the steps to repair your credit profile can help you understand how dispute work and rebuilding strategy fit together. Results vary based on your file, supporting records, creditor responses, and current credit behavior.

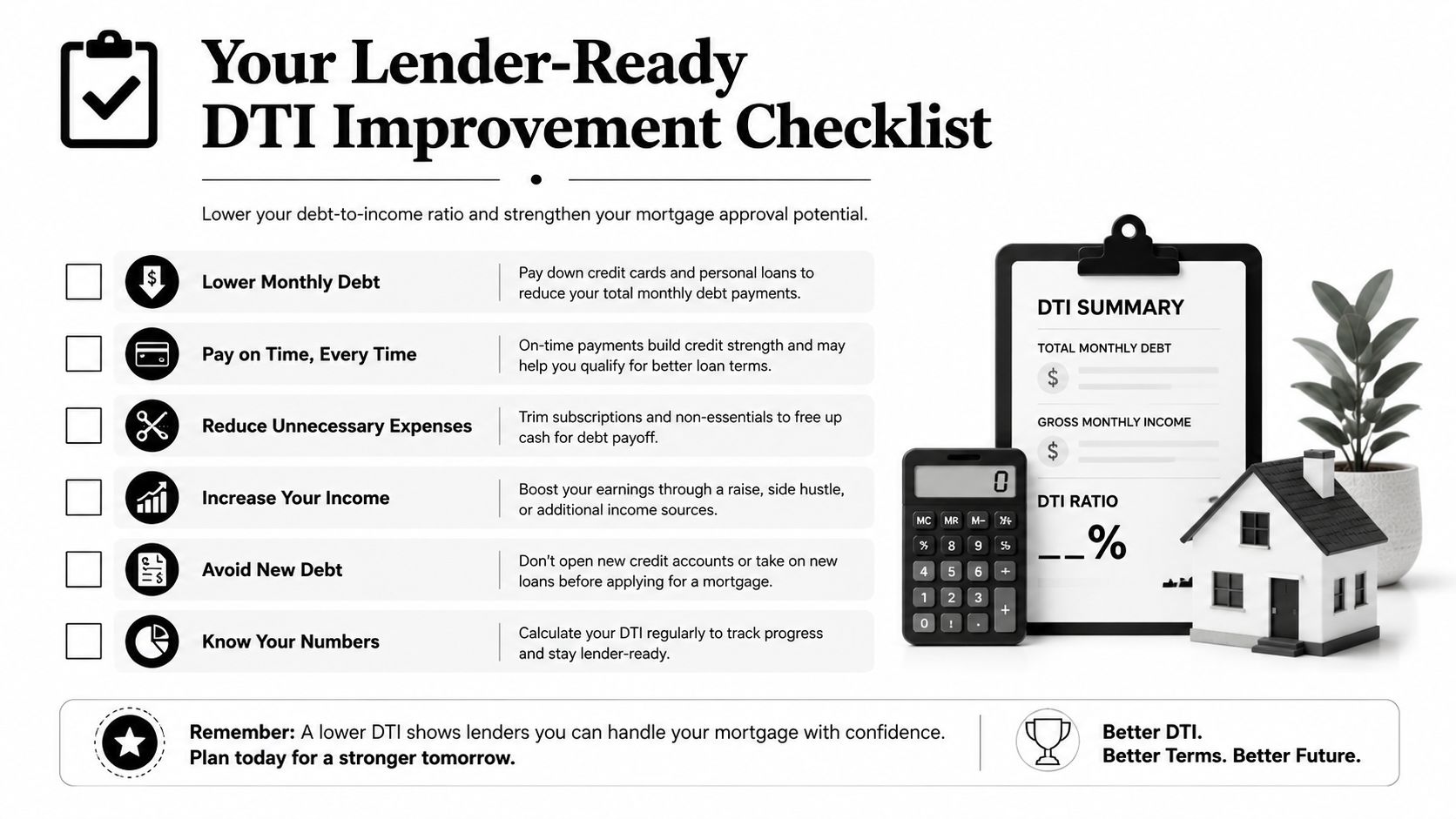

Your Lender-Ready DTI Improvement Checklist

When buyers feel overwhelmed, a checklist helps. Mortgage readiness becomes much easier when you stop treating DTI like a vague problem and start treating it like a file-prep project.

What to gather first

Start with documents, not guesses.

- Current pay records: Gather recent pay stubs and any documentation for bonus or commission income.

- Debt statements: Pull current statements for credit cards, auto loans, student loans, personal loans, and any support obligations.

- Bank activity: Review recent transactions for recurring BNPL payments or overlooked financed purchases.

- Tax records: Keep returns ready if you plan to include self-employment, side income, or other non-base earnings.

- Credit reports: Review for credit report errors, collections, outdated information, and questionable balances.

What to do next

After you have the paperwork, follow a lender-minded sequence.

- Calculate your real DTI using required monthly payments, not rough estimates.

- Prioritize debt reduction on accounts that create the most pressure on your monthly obligations.

- Pause new borrowing while you're preparing for a mortgage review.

- Document all qualifying income that meets lender standards.

- Review account accuracy if collections, charge-offs, or balance reporting look wrong.

- Track progress monthly so you know whether your file is improving.

A realistic timeline depends on what is driving the problem. Some changes, like paying down a revolving account, can affect your numbers relatively quickly once updated. Other improvements, such as building a longer documented income history or resolving disputed reporting, take more time and careful follow-through.

If your credit file has errors, old collections, high utilization, or confusing account status issues, Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation to better understand your options. That kind of review can be useful for mortgage credit repair, credit repair for homebuyers, and lender-readiness planning. Results vary, and any improvement depends on the accuracy of the information, available documentation, account history, and creditor or bureau responses.

Frequently Asked Questions About DTI Ratios

Does closing a credit card help my DTI

Usually, not by itself. DTI focuses on required monthly debt payments, not your available credit limits. If you close a card with a balance, the payment obligation remains. Even if the card has no balance, closing it can sometimes hurt your broader credit profile by affecting utilization and account mix, which may not help your mortgage file overall.

Does co-signing a loan affect mortgage underwriting

It often can. If your name is on the loan, the lender may treat that payment as part of your obligations unless there is acceptable documentation showing another party has been making the payments in a way the lender recognizes. Co-signing is easy to underestimate because the debt may feel like someone else's responsibility, but underwriting often sees it differently.

Can a large down payment overcome a high DTI

A larger down payment can strengthen a mortgage application, but it doesn't erase DTI concerns. Underwriters still evaluate monthly affordability. If the ratio is too high, the down payment alone may not solve the issue.

Should I stop saving and only pay debt

It depends on your situation, but many homebuyers need balance. You don't want to drain every dollar and leave yourself unprepared for reserves, closing costs, or emergencies. At the same time, if your DTI is the main barrier, debt reduction may deserve more immediate attention than building a larger down payment.

Where can I learn more about related credit issues

If you're sorting through collections, utilization, reporting errors, or lender-readiness concerns beyond DTI, these frequently asked questions can help clarify common credit repair and mortgage preparation topics.

Superior Credit Repair provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges. If you're working on how to lower debt to income ratio while also dealing with collections, late payments, charge-offs, medical collection credit repair issues, or high utilization, Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation to better understand your options. Results vary based on each person's credit file, documentation, creditor responses, account history, and current credit behavior.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile. Superior Credit Repair Google Business Profile