A lot of first-time homebuyers reach the same moment at the same time. The house search starts to feel real, the lender asks about credit, and old worries come rushing back. A collection from years ago. A late payment you thought was resolved. A credit card balance that crept up while life got expensive.

That stress is understandable, but it doesn't mean you're stuck.

To clean up credit history in a lawful, practical way, you need a process. Not a trick. Not a promise. A careful review of what is reporting, what is inaccurate or outdated, what is legally disputable, and what needs to be managed over time so your credit profile looks more stable to a mortgage lender. That approach matters whether you're preparing for FHA loan preparation, VA loan preparation, USDA loan preparation, or a conventional mortgage application.

Table of Contents

- Your Path to a Stronger Credit Profile Starts Here

- Obtaining and Auditing Your Three Credit Reports

- How to Dispute Inaccurate Information with Credit Bureaus

- Managing Legitimate Negative Information

- Rebuilding Your Credit Profile for Long-Term Strength

- Modern Credit Challenges and Mortgage Readiness

- Frequently Asked Questions and Your Next Steps

Your Path to a Stronger Credit Profile Starts Here

A family can do everything right for months, save for a down payment, reduce spending, and still feel unprepared when the mortgage conversation turns to credit. That usually happens because credit reports feel technical and personal at the same time. One line on a report can affect confidence far more than it should.

Clean up credit history work starts by separating emotion from documentation. A credit report isn't a judgment about your character. It's a record, and records can contain inaccurate, outdated, unverifiable, or misleading information. They can also contain accurate negative items that need to be managed patiently while stronger recent behavior takes shape.

What credit cleanup really means

In a compliant setting, credit repair or credit restoration means reviewing your reports, identifying questionable reporting, gathering records, and using the legal dispute process under the Fair Credit Reporting Act, often called the FCRA. It also means being honest about what cannot be removed solely on the grounds of inconvenience.

That distinction matters for homebuyers. Mortgage lenders don't just look at a score. They look for stability, consistency, and a file that makes sense.

Practical rule: A lender-ready credit profile is usually cleaner, more accurate, and more consistent. Not necessarily perfect.

Where readers often get confused

Many people assume "bad credit" is one problem. It usually isn't. It may be a mix of several separate issues:

- Reporting errors such as a late payment that wasn't late or an account that isn't yours

- Old derogatory items that may be close to their legal reporting limit

- Current revolving balances that make utilization look too high

- Thin credit files where there isn't enough recent positive history

- Fintech and BNPL activity that doesn't always appear clearly on a traditional report

If you're trying to improve credit score results before buying a home, the right question isn't, "How do I erase everything?" It's, "What does my file say today, and which parts are inaccurate, outdated, or creating avoidable risk?"

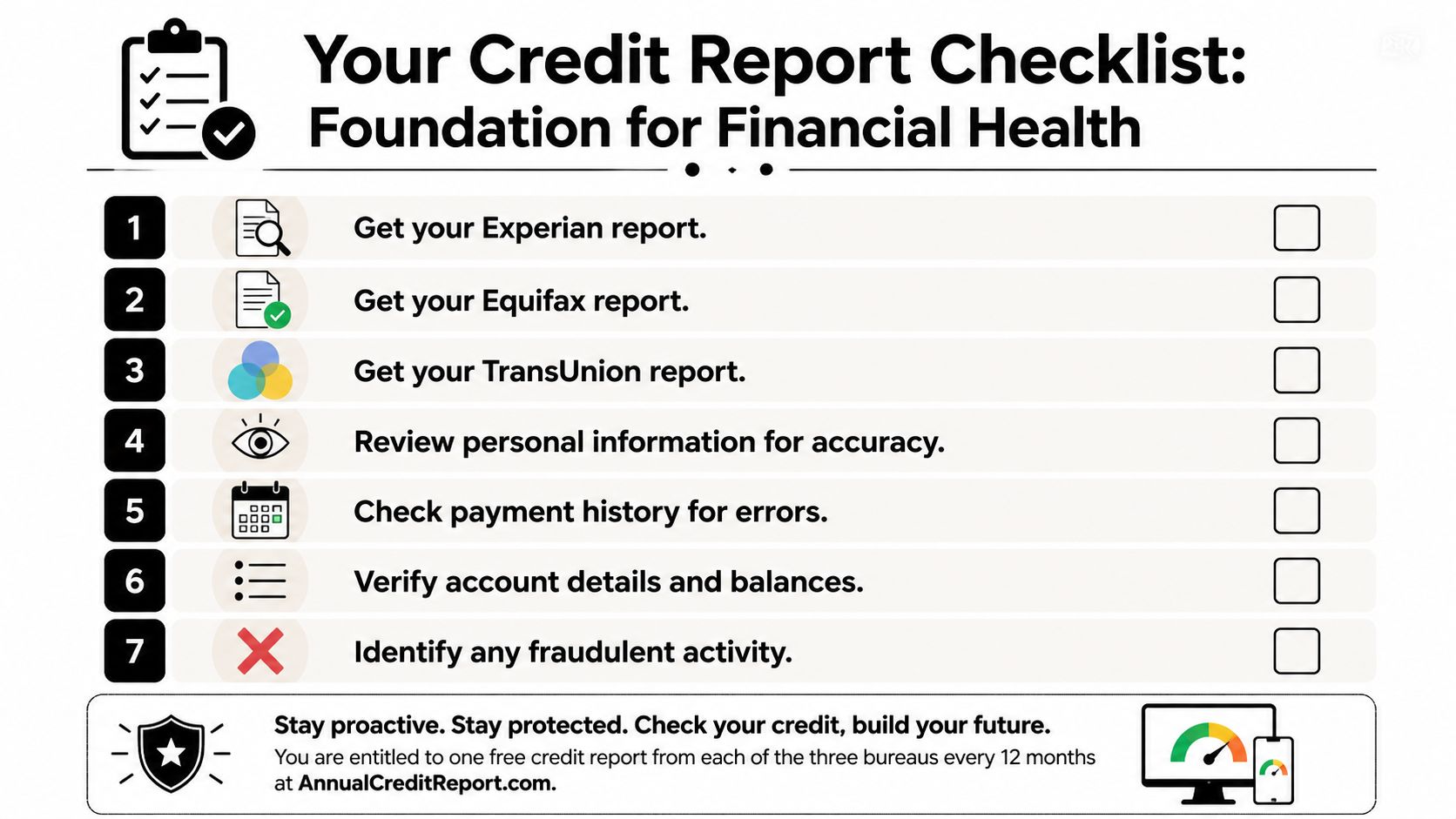

Obtaining and Auditing Your Three Credit Reports

A sound credit cleanup process begins with a full review of your files from all three major bureaus. Information can differ from bureau to bureau, which means an account deleted on one report might still appear on another. A three-bureau audit is part of a technically sound workflow, and a practical sequence is to identify errors, dispute each bureau separately, verify outcomes, then improve utilization and payment habits. The same guidance also notes that keeping revolving balances below 30% is a common benchmark, while many experts prefer 10% or less for stronger scoring signals, as outlined in this step-by-step credit improvement guide.

Why all three reports matter

Mortgage lenders rarely rely on a single credit file. If you're preparing for credit repair before buying a home, review Experian, Equifax, and TransUnion separately. You're looking for consistency, not just major problems.

Some differences are easy to spot. Others are subtle. A balance may be wrong on one report. A collection may show a different date. A late payment may appear in one bureau's file but not the others.

A practical audit checklist

Use a slow, line-by-line review. Don't skim.

- Personal details first. Check your name, former names, addresses, and employers. A wrong address doesn't always hurt a score, but it can signal mixed-file problems.

- Account ownership next. Confirm every tradeline belongs to you. If an account looks unfamiliar, flag it.

- Payment history carefully. Look month by month for reported late payments that don't match your records.

- Balances and limits. Verify current balances, credit limits, and account status. A wrong balance can make utilization look worse than it is.

- Duplicate derogatory reporting. Watch for the same debt appearing multiple ways, especially after a transfer to collections.

- Dates. Check opened dates, closed dates, and delinquency timing. These details affect how long negative information may report.

- Inquiries and public records. Make sure they are recognizable and accurate.

A simple worksheet can help:

| Area to review | What to ask |

|---|---|

| Personal information | Is this identifying information correct and current? |

| Tradelines | Do I recognize this account and its status? |

| Payment history | Were these late marks reported correctly? |

| Balances | Do the balances and limits match my statements? |

| Negative items | Is anything duplicated, misleading, or outdated? |

Pulling all three reports before you dispute helps you avoid a common mistake. Fixing one bureau's file while ignoring the others.

Feeling overwhelmed often prompts many readers to search for local credit repair companies. That's understandable. Still, whether you handle the first review yourself or get collections dispute help, the foundation is the same. Audit first. Document second. Dispute only what you can explain and support.

How to Dispute Inaccurate Information with Credit Bureaus

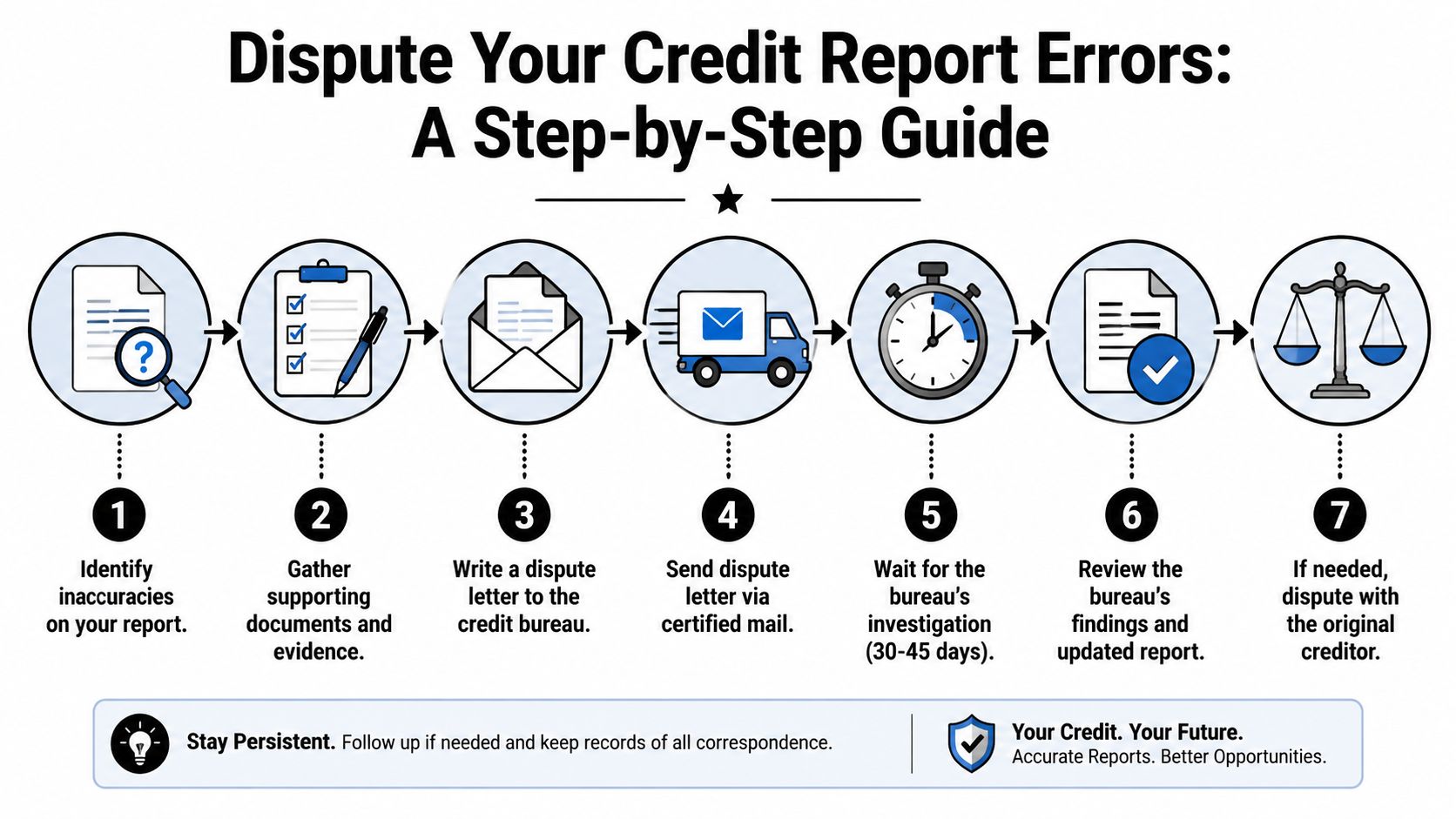

Once you've identified a reporting issue, the next step is formal. The FCRA gives consumers the right to dispute information they believe is inaccurate, outdated, or unverifiable. That process is legal and document-based. It isn't about sending angry letters or disputing everything on the page.

Credit report accuracy matters because nearly 20% to 25% of consumers have errors on their reports that could significantly affect their credit scores, and payment history makes up 35% of FICO scoring models. The FCRA requires bureaus to investigate disputes within 30 days, and nearly 40% of disputes result in a modification or deletion. For homebuyers, that can matter because a single 30-day late payment can lower a score by 60 to 100 points. Those figures are part of the verified data provided for this article.

What makes a dispute strong

A strong dispute is specific. It names the account, identifies the exact error, and includes supporting records.

You don't need legal language. You do need clarity.

A useful dispute packet usually includes:

- A short dispute letter identifying the bureau and the account in question

- A clear explanation of what is wrong

- Copies of supporting documents such as statements, payment records, identity documents, or correspondence

- A copy of the report page with the disputed item marked

Send each dispute to the correct bureau for the item showing on that bureau's report. If the same problem appears on all three, prepare separate disputes.

A practical example helps. If a late payment is showing for a month when you have proof the account was paid on time, your letter should state the account name, account number as shown on the report, the month being challenged, and the document proving timely payment. That's much stronger than writing, "This account is hurting me, please remove it."

Readers who want a model can review this resource for first-time homebuyers to dispute credit.

What happens after you send it

The bureau generally has 30 days to investigate. During that window, it reviews the dispute and contacts the furnisher of the information.

Three outcomes are common:

- The item is corrected

- The item is deleted

- The item is verified as reported

If information can't be verified, it must be corrected or removed. Keep copies of everything you send and everything you receive back. That paper trail matters.

Send disputes with documentation and keep organized records. A well-supported dispute gives the bureau something concrete to investigate.

Some consumers also dispute directly with the creditor or collector furnishing the information. That can be appropriate, especially when the creditor holds the underlying records. The key is consistency. Your explanation and documents should match across the bureau dispute and any direct creditor dispute.

For mortgage credit repair, this disciplined approach is often more useful than broad, unsupported challenges. Lenders respect files that show clear corrections and responsible follow-through.

Managing Legitimate Negative Information

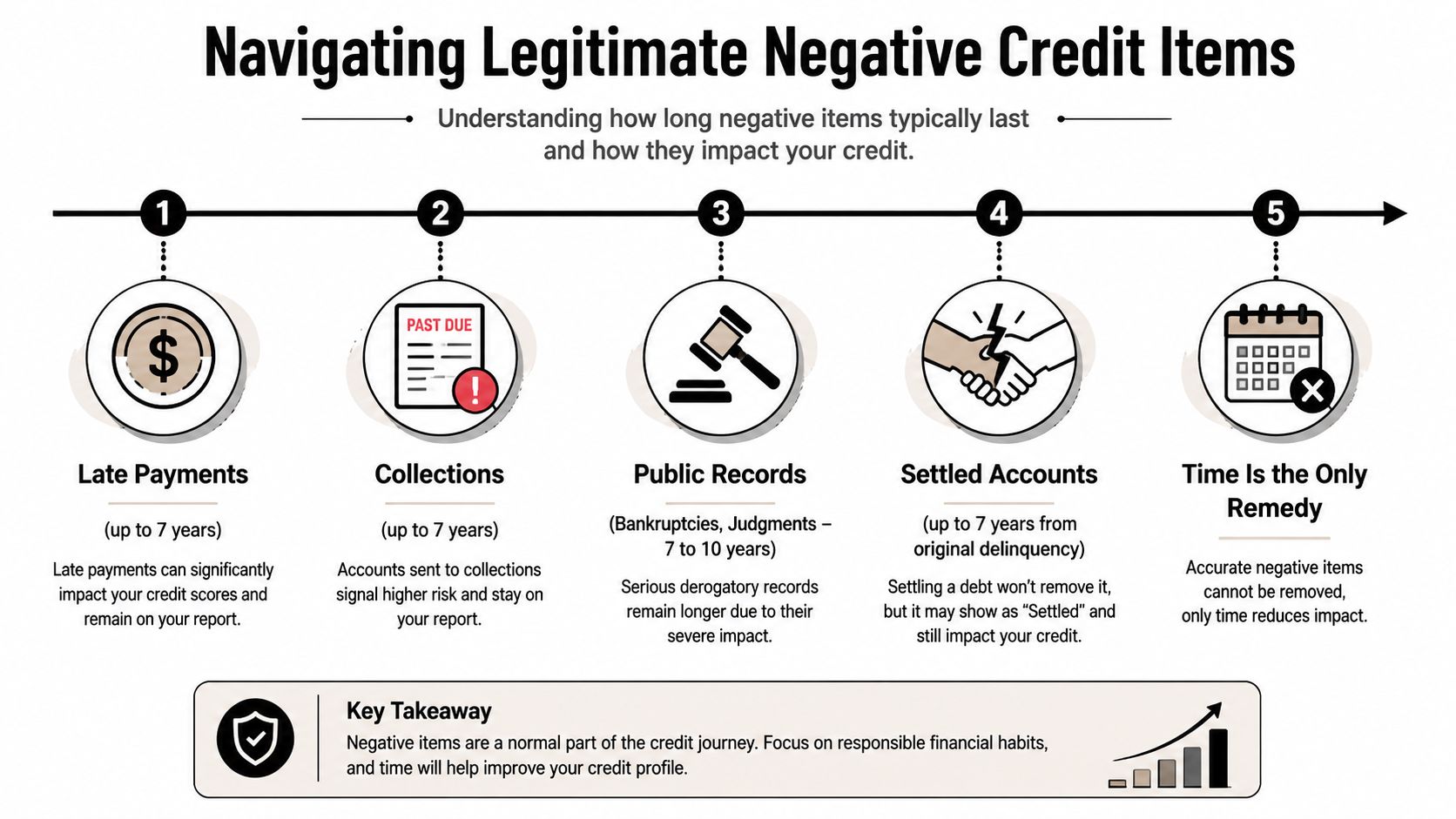

Not every negative account is an error. Some late payments, collections, and charge-offs are accurate. When that happens, the job shifts from removal efforts to smart management, timing, and rebuilding. That's a major part of responsible credit repair for homebuyers.

What the seven-year rule means

Under the FCRA, late payments, collections, and charge-offs remain on a consumer's file for exactly seven years from the date of the initial missed payment. If a collection account was sent out in 2019, it would age off in 2026. If a negative item remains beyond that period, the consumer has the right to dispute it for deletion because continued reporting would violate the law. Those reporting rules are part of the verified data provided for this article.

That timeline helps in two ways. First, it prevents panic about old items that are already moving toward expiration. Second, it helps you spot reporting problems if an account should have aged off but didn't.

What to do when the item is accurate

When an item is valid, be realistic. Disputing accurate information without evidence usually doesn't help. It can waste time you could spend improving current behavior.

Here are the common options:

- Wait for lawful aging off. If the item is old and near the end of its reporting period, patience may be the most practical strategy.

- Address active debts carefully. If a collection or charge-off still affects your mortgage planning, talk with your lender or a qualified advisor about how underwriters may view it.

- Consider goodwill requests cautiously. For an isolated late payment on an otherwise strong account, some consumers ask the creditor for a courtesy adjustment. That's optional and not guaranteed.

- Be careful with informal deals. Some people ask for "pay-for-delete" arrangements. These are not guaranteed, and consumers should understand that a verbal promise is not the same as a reliable reporting outcome.

If wage garnishment or severe collection pressure is part of the broader financial problem, legal context may matter as much as credit reporting. In those situations, guidance on protecting wages from creditors can help you understand one part of the bigger picture.

A lot of homebuyers also underestimate the financial impact of late payments. Even when a late mark is accurate and stays on the report, its influence can become easier to offset when the rest of the file shows stable, current performance.

Rebuilding Your Credit Profile for Long-Term Strength

Correcting errors is only half of the work. The other half is showing lenders that your present credit behavior is steady. That's what helps rebuild credit profile strength over time.

The habits lenders notice

The most visible signal is often credit utilization, which means how much of your revolving credit you're using compared with your limits. If your cards are close to maxed out, the file can look strained even if you've never missed a payment.

A practical target is to keep balances low and avoid letting revolving accounts report heavy usage right before a mortgage review. Smaller balances usually present a more stable picture than accounts that swing up and down.

Another habit is simple but powerful. Pay every account on time from this point forward. Once the report is accurate, current behavior becomes your strongest evidence that the past isn't the whole story.

A cleaner report works better when it is paired with boring, predictable account management. Lenders usually like boring.

Ways to add positive history carefully

If your file is thin or damaged, adding positive information may help over time. The method matters.

- Secured credit cards. These can help establish or re-establish revolving history if used lightly and paid on time.

- Credit-builder products. Some consumers use installment-based tools to create documented payment history.

- Authorized user strategy. Being added to a well-managed account can help in some cases, but it also carries risk if the primary account holder misses payments or runs high balances.

- Account stability. Avoid opening several new accounts at once unless there's a clear reason. Too much new activity can make a file look unsettled.

For people who want outside structure, a compliance-based service can help organize the review and rebuilding steps. Superior Credit Repair works within a documentation-based dispute process and also helps consumers understand rebuilding actions that support mortgage readiness. If you're comparing options, this guide for mortgage-ready credit gives a practical overview.

A stronger file usually doesn't come from one dramatic move. It comes from fewer mistakes, lower balances, and more months of clean payment history stacked together.

Modern Credit Challenges and Mortgage Readiness

Mortgage underwriting today isn't limited to traditional credit cards and auto loans. Many first-time buyers use financial tools that weren't part of the old playbook, especially buy now, pay later, often shortened to BNPL.

Why BNPL can confuse homebuyers

The CFPB has noted that BNPL use has expanded quickly and raised concerns about how these loans are reported and whether consumers can easily dispute them, as reflected in the verified data and in the FTC's consumer guidance on fixing credit reports and related issues.

That matters because a BNPL-heavy file can create liabilities that don't always show up clearly in the way consumers expect. A report may look thin or even clean, while bank statements and debt-to-income review tell a different story to an underwriter.

If you use tools like Affirm, Klarna, Afterpay, Sezzle, or PayPal installment products, review them the same way you'd review any other debt obligation. Confirm whether they appear on your reports. Track the payment schedule. Reduce account clutter where possible. If you're working through this issue in detail, these strategies for managing credit with BNPL can help frame the questions to ask before a mortgage application.

What lender-ready really means

For FHA, VA, USDA, and conventional mortgage preparation, a lender-ready profile usually means more than a score. It means your credit file, bank activity, and debt picture tell the same story.

That story should show:

- Stable recent payment behavior

- Reasonable revolving balances

- Few surprises in underwriting

- Clear explanations for any past hardship

For buyers in Florida, local housing context can also be useful alongside credit planning. A market-specific Palm Coast home buying credit score guide can help you compare general credit expectations with what buyers often encounter during the purchase process.

A modern mortgage review is part credit report, part documentation review, and part common-sense risk analysis. The cleaner and more understandable your file is, the easier it becomes to present yourself as a prepared borrower.

Frequently Asked Questions and Your Next Steps

Common questions from homebuyers

How long does it take to clean up a credit history?

Results vary. A straightforward reporting error may be addressed within the bureau's investigation period, while broader rebuilding can take much longer. The timeline depends on the accounts involved, your documentation, creditor responses, and how consistently you manage current credit.

Can a credit repair company guarantee deletions or mortgage approval?

No. A compliant credit repair company can't guarantee that a negative item will be removed, and it can't promise loan approval. The legal process is based on accuracy, verification, and documentation.

Should I dispute every negative item on my report?

No. Dispute information that is inaccurate, outdated, unverifiable, or misleading. Disputing accurate items without evidence usually isn't productive.

Do I need professional help?

Not always. Some consumers can handle the review and dispute process on their own. Others prefer guidance because the file is complex, the mortgage timeline is tight, or they want help staying organized. If you're weighing that option, this article on understanding professional credit repair for homebuyers may help.

What should I focus on first before applying for a mortgage?

Start with accuracy. Then work on current payment consistency, lower revolving balances, and simpler overall account management. Lenders generally respond well to a file that looks stable and well-documented.

If you feel stuck, slow the process down and return to the basics. Review all three reports. Mark the specific issues. Gather records. Challenge only what you can support. Then improve the habits that shape your file going forward.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation to better understand your options.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile.

If you're preparing for homeownership and want a clearer, compliance-focused plan, Superior Credit Repair can help you review your reports, identify questionable items, and understand practical next steps for building a stronger credit profile.