Buying a home often starts the same way. You check listings late at night, save a few favorites, then wonder whether a lender will approve you. For many first-time buyers, that's the stressful part. It can feel like lenders use a secret formula that nobody explains clearly.

They don't.

Mortgage approval is a structured review. Lenders are trying to answer one practical question: does this application show a stable, documented ability to repay the loan on a property that supports the financing? Once you understand that, the process gets less mysterious and much easier to prepare for.

That matters if you're dealing with old collections, high credit card balances, late payments, a thin file, recent credit repair activity, or modern payment patterns like BNPL accounts. It also matters if you're choosing between FHA, VA, USDA, and conventional financing and need to know where to focus first.

If you're early in the process, this essential guide for BC home buyers can help you understand how pre-approval fits into your planning. The details vary by market, but the basic lesson is useful everywhere. Clear preparation usually beats guesswork.

Table of Contents

- Preparing for Your Homeownership Journey

- The Four Cs of Mortgage Underwriting

- A Deep Dive into Your Credit Profile

- Assessing Your Capacity to Repay the Loan

- Meeting Requirements for Different Loan Types

- How to Avoid Common Underwriting Red Flags

- Your Lender-Ready Action Plan

- Frequently Asked Questions

Preparing for Your Homeownership Journey

A lot of buyers start with the wrong assumption. They think the lender is hunting for a perfect borrower.

In reality, the lender is reviewing risk in a consistent way. That's good news, because consistent rules mean you can prepare for them. If your credit report has errors, if your balances are too high, or if your income documentation is messy, those are issues you can work through in an orderly way.

A first-time buyer might have a steady job, enough income to feel comfortable with a house payment, and still get nervous because of an old medical collection or a few high cards. Another buyer may have a decent score but little savings after the down payment. Someone else may have used BNPL apps heavily and not realize that scattered activity can make the file look less stable than they expected.

Mortgage underwriting is not a personality test. It's a documentation and risk review.

The most useful way to understand what mortgage lenders look for is through the Four Cs. Lenders look at your credit, your capacity, your capital, and the collateral itself. Those four buckets explain almost every document request, every condition, and every follow-up question you'll receive.

If you keep that framework in mind, the process starts to feel more manageable. You don't need a magic trick. You need a lender-ready profile that shows accuracy, stability, and the ability to handle the payment over time.

The Four Cs of Mortgage Underwriting

Mortgage lenders use a long-standing framework when they review home loan applications. Freddie Mac describes it this way: lenders assess the four C's of credit, meaning credit, capacity, capital, and collateral, to determine whether a borrower is likely to repay the loan, as explained in Freddie Mac's overview of the four C's of qualifying for a mortgage.

A simple way to think like an underwriter

If you want the plain-English version, think of the Four Cs like this:

- Credit is your financial reputation.

- Capacity is your ability to handle the payment from current income.

- Capital is your safety net.

- Collateral is the house itself and whether it supports the loan.

That framework matters because many buyers focus only on score. Score matters, but lenders don't stop there. They also want to know whether the payment fits your income, whether you have funds available, and whether the property is acceptable for financing.

What each C is really asking

Credit

This asks: How has this person handled credit over time?

Lenders review your score, payment history, and the overall accuracy of the credit report. They're looking for signs of consistency. A file with on-time payments and modest balances tells a different story than a file with recent late payments, disputed account confusion, or heavy revolving debt.

Capacity

This asks: Can this person reasonably afford the monthly payment?

Here, the lender reviews income, employment history, and monthly debt obligations. The goal isn't just to see income on paper. The lender wants documented income that appears stable enough to support the new mortgage payment.

Capital

This asks: What financial cushion does this person have?

Capital includes savings, down payment funds, and other assets. Buyers often underestimate this category. Even if you qualify on paper, lenders want to see that you're not arriving at closing with nothing left over. Available funds can help show that you're prepared for closing costs, reserves, or normal homeownership surprises.

Practical rule: A stronger application usually shows both the ability to buy the home and the ability to stay financially steady after closing.

Collateral

This asks: Is the property worth financing?

The home secures the loan, so the lender checks its value and condition. That's where the appraisal and property review come in. Even a financially strong borrower can run into problems if the home doesn't meet lender or program standards.

Here's the short version:

| Four C | What the lender reviews | What the lender wants to know |

|---|---|---|

| Credit | Score, payment history, report accuracy | Do you manage debt responsibly? |

| Capacity | Income, employment, DTI | Can you afford the payment? |

| Capital | Savings, assets, funds to close | Do you have a cushion? |

| Collateral | Appraisal, property condition | Is the home acceptable security? |

Once you see the process through those four lenses, most underwriting questions make sense.

A Deep Dive into Your Credit Profile

A first-time buyer can do everything right for six months, then get confused when the lender asks about a store card balance, a recent dispute, or a buy now, pay later account. That reaction is normal. Credit review feels personal, but underwriting treats it as pattern recognition.

The lender is trying to answer a practical question. Does this credit profile show steady borrowing habits that are likely to continue after closing?

For government-sponsored enterprise loans, borrowers often come in with higher scores than FHA borrowers, according to the Federal Reserve Bank of New York's mortgage market review at Liberty Street Economics. That gap matters because your target should match your loan path. A conventional buyer usually needs a cleaner, more established profile than an FHA buyer, while a VA applicant may have more flexibility in some areas but still needs a file that looks stable and well documented.

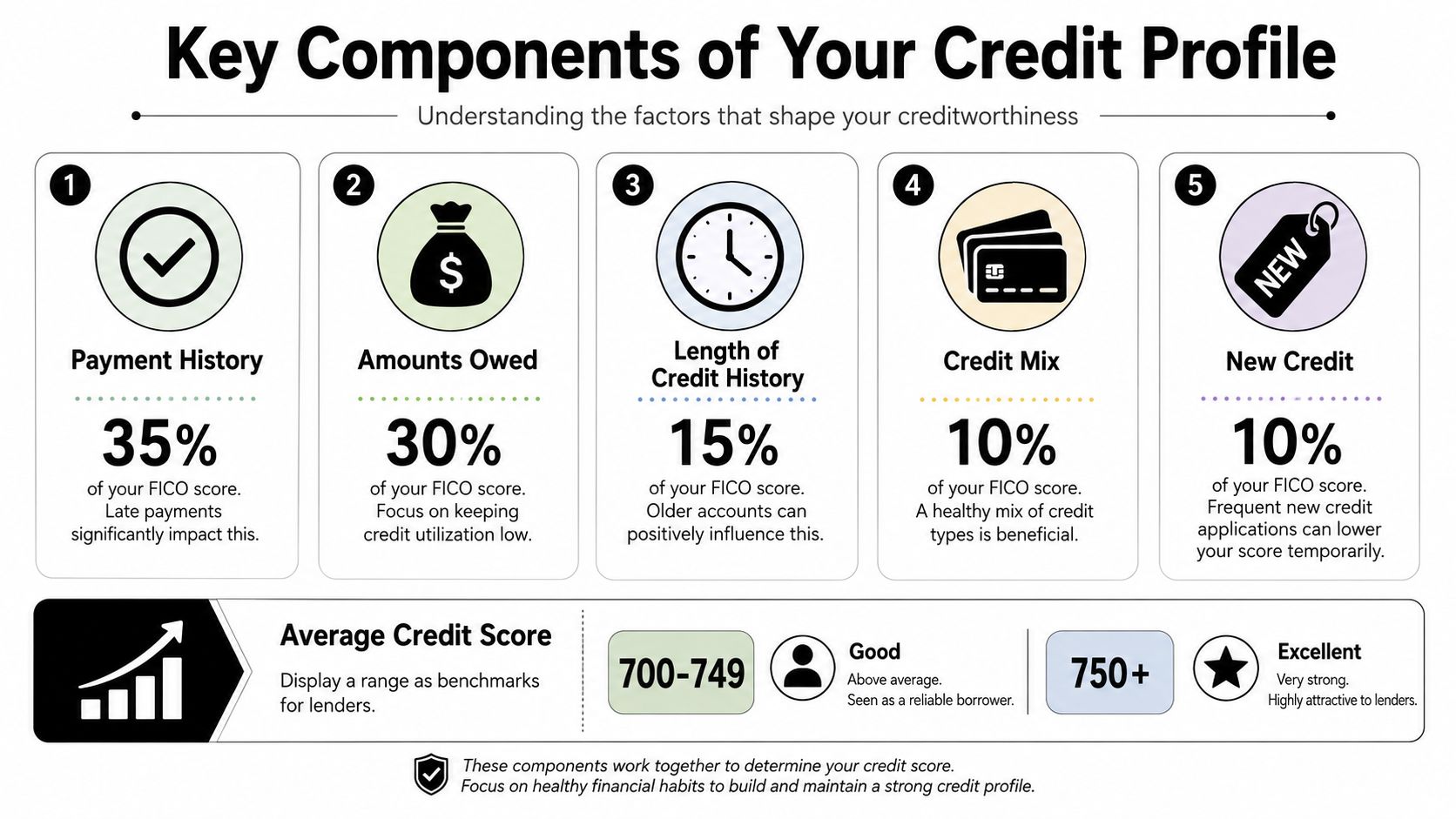

Your score is the headline, not the full story

A credit score gives the lender a quick summary. The credit report shows how that summary was built.

Two applicants can land in a similar score range and still look very different to an underwriter. One may have older accounts, low card balances, and one isolated problem from years ago. Another may have several newly opened accounts, recent balance spikes, and active disputes. The number may be close. The risk picture is not.

If you want a clearer view of the scoring side of mortgage prep, start with this guide on understanding mortgage credit scores.

What underwriters focus on inside the report

Payment history

Payment history often carries the most weight because it answers the most basic lending question. Do you pay obligations on time?

Recent late payments usually draw more attention than older ones. A single late payment from years ago, followed by clean history, often reads very differently from a 30-day late reported two months before application. Underwriters also notice patterns. Several small lates across different accounts can signal stress, even if none of them looks severe on its own.

Revolving balances

Credit cards are useful, but high balances can create two problems at once. They can pull down scores, and they can make the file look tight from a cash flow standpoint.

A card that is nearly maxed out suggests less room for error. Even if you pay on time every month, heavy utilization can make the profile look less stable than it really is. For buyers preparing over the next few months, lowering revolving balances is often one of the fastest ways to improve how the file reads.

Age and mix of accounts

Lenders generally prefer to see accounts that have been open long enough to show a pattern. A profile built gradually tends to look steadier than one built quickly right before a mortgage application.

You do not need every type of credit account. You do want the accounts you have to look established, active, and managed consistently.

Recent applications and new debt

A burst of new credit can raise questions. Underwriters may ask why several accounts were opened recently, whether balances have increased, and whether the borrower is still taking on debt while trying to qualify.

This is one reason mortgage prep works best as an action plan, not a last-minute scramble. Opening accounts to "help your score" shortly before applying can backfire if the report starts to look busy or unstable.

How lenders read modern credit behavior

Underwriting has had to catch up with newer borrowing habits. Buy now, pay later usage is a good example.

Some BNPL accounts may not appear on every report the same way traditional loans do, but lenders still review bank statements, liabilities, and spending patterns. Frequent installment purchases for everyday items can suggest thin cash reserves or a habit of stretching monthly obligations. It does not automatically disqualify you. It does mean the file may need more explanation, especially if your loan program already has tighter credit expectations.

Recent credit repair activity can also draw attention. Disputing inaccurate information is reasonable. Filing a cluster of disputes right before underwriting can slow the process because lenders may ask for updates after the disputes are resolved. If negative items are being challenged, the best approach is usually accuracy first, paper trail second, timing third.

How negative items affect mortgage readiness

Negative marks matter, but context matters just as much.

A collection from years ago is different from a fresh unpaid collection. A charge-off with no recent problems since may be easier to explain than several current late payments. Underwriters want to know what happened, whether the issue is resolved, and what your credit behavior has looked like since then.

A useful way to think about it is this: lenders are not grading your past. They are testing whether the file looks stable now.

Here is how common issues are often interpreted:

- Collections: These can trigger extra review, especially if they are recent, unpaid, or inconsistent with the rest of the file. The right response depends on the loan type. FHA, VA, and conventional underwriting can treat collections differently.

- Charge-offs: These show a prior failure to repay as agreed. The age of the account and the history after the charge-off usually matter more than the label alone.

- Late payments: One isolated late payment is usually easier to explain than a repeating pattern across multiple accounts.

- Credit report errors: Wrong balances, duplicate accounts, mixed files, and incorrect dates can make a borrower look riskier than they are.

A mortgage-ready credit file should look accurate, explainable, and steady.

That standard is more useful than chasing a perfect score.

A structured credit restoration process can help if it focuses on documented errors, outdated information, and habits that improve the file over time. Superior Credit Repair is one option some consumers use for that process. The company reviews reports, helps identify inaccurate or questionable items, and supports a compliance-focused dispute and rebuilding process. Results vary by file, creditor response, and reporting history.

Assessing Your Capacity to Repay the Loan

Capacity is where lenders test whether the mortgage payment fits your real life, not just your hopes.

A buyer may say, “I can afford this.” The underwriter still needs documented proof. That means verified income, employment history, and a review of the debts already competing for your monthly cash flow.

Why income history matters

Lenders generally want to see income that appears stable and likely to continue. That's why employment history gets so much attention. They're not trying to make things difficult. They're trying to confirm that the income used for qualifying is dependable enough to support a long-term mortgage obligation.

A straightforward salary history is usually easier to document than variable income. Commission income, self-employment income, gig work, overtime, and bonuses may still be usable, but the paper trail often matters more.

How to calculate your DTI

One of the primary technical filters lenders use is the debt-to-income ratio, or DTI. The DTI ratio compares total monthly debt obligations to gross monthly income, and for first-time buyers, a DTI that stays above 43% often triggers manual underwriting or added requirements, according to the research summarized in the Journal of Financial and Quantitative Analysis at Cambridge Core.

Use this simple formula:

- Add up your monthly debt payments.

- Use your gross monthly income before taxes.

- Divide total monthly debt by gross monthly income.

Example:

- Car payment

- Student loan

- Credit card minimums

- Personal loan

- Estimated housing payment

Add those monthly obligations together. Then divide by your gross monthly income.

If the result is low enough for the program and the rest of the file is solid, you're in better shape. If it's high, the lender may still review the file, but the path can get narrower.

Buyers often focus on paying off the biggest balance first. For DTI, the more useful move is often reducing the monthly obligation that improves the ratio fastest.

What to do if your DTI is too high

If your DTI looks tight, the most practical fixes are usually:

- Pay down debts with meaningful monthly payments. A smaller balance doesn't matter much if the payment remains on the report.

- Avoid new financing. A new car, new furniture account, or personal loan can weaken a file quickly.

- Review income documentation carefully. Missing documents can make income harder to use.

- Watch utilization at the same time. Lower revolving balances can help the file from more than one angle.

High DTI doesn't always mean no. It often means the file needs stronger support in other areas, cleaner documentation, or a different loan program.

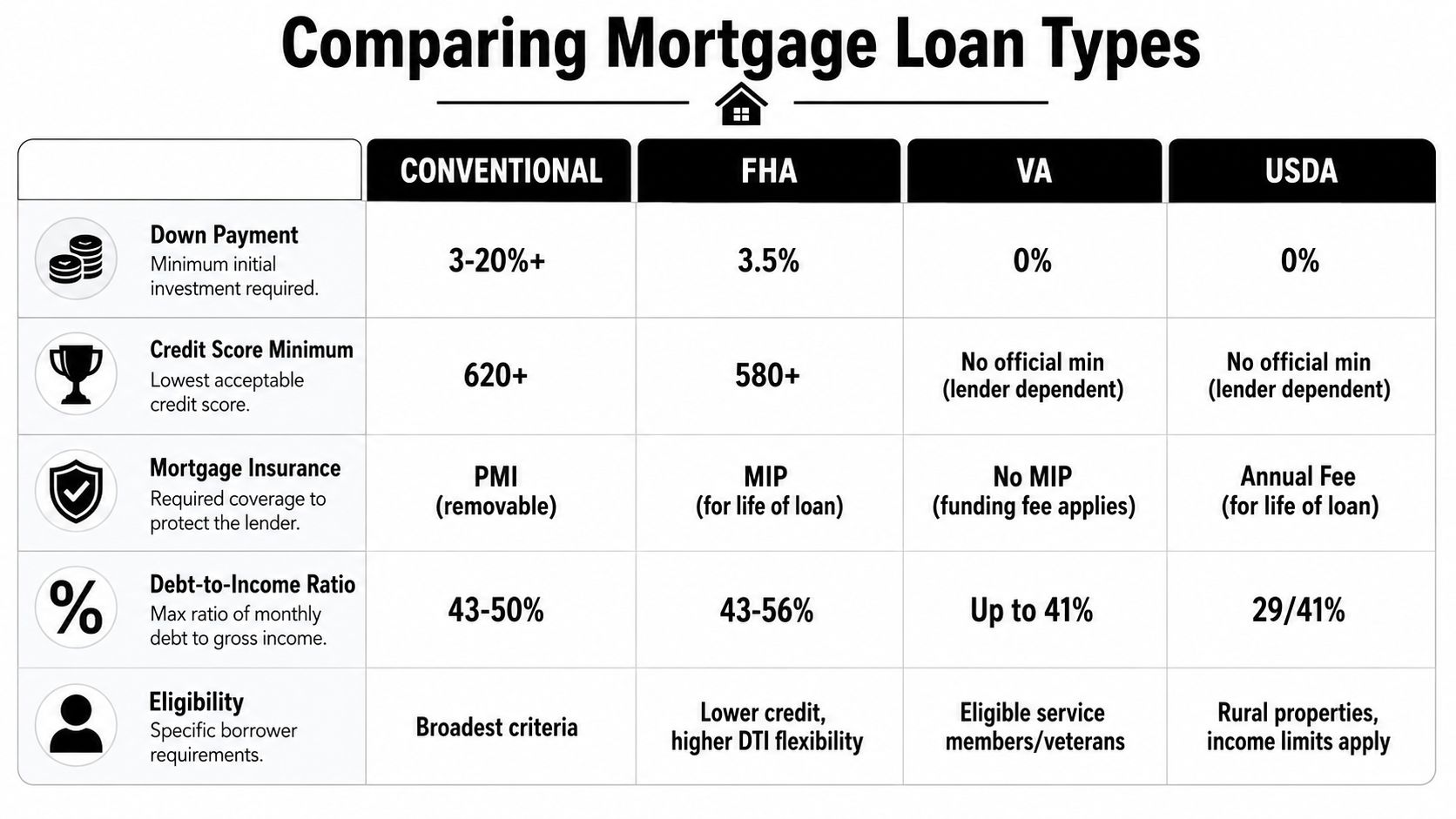

Meeting Requirements for Different Loan Types

A first-time buyer can look solid on paper and still fit one loan program better than another. That is because lenders do not read every file through the same lens. They are asking a slightly different version of the same question with each program: does this borrower match the risk rules for this loan type?

A useful way to think about it is matching your file to the lane that fits it now. Conventional usually rewards a cleaner, more established profile. FHA often gives more room for past credit issues if recent behavior is steady. VA and USDA have their own strengths, but both still require a file that looks understandable, documented, and stable.

Conventional loans

Conventional financing usually suits borrowers whose credit profile already looks settled. Underwriters tend to pay close attention to score, revolving utilization, cash reserves, and whether the report shows recent stress.

This is also the loan type where modern credit behavior can matter more than buyers expect. Frequent Buy Now, Pay Later activity, fresh balance transfers, and recent credit repair bursts may not always lower a score much, but they can still make the file look newly managed rather than consistently strong. A conventional file usually reads best when accounts have been handled predictably for a while.

FHA loans

FHA loans often work well for first-time buyers, borrowers recovering from older setbacks, or applicants with thinner credit files. The standard is not perfection. The standard is a reasonable credit story supported by current stability.

If you are comparing this path with other options, FHA loan eligibility for homebuyers can help you sort out what to review before applying. FHA underwriting may be more forgiving about past issues, but lenders still notice recent late payments, unresolved collections, sudden score jumps tied to disputes, and heavy new account activity. They want to see that the improvement is real and likely to last.

VA loans

VA financing can be one of the strongest options for eligible service members and veterans. Eligibility helps. It does not replace underwriting.

Lenders still review credit habits, income consistency, and the overall picture of financial readiness. For VA borrowers, the file often benefits from a simple pattern: bills paid on time, limited new debt, and no signs that the household budget is getting stretched. If BNPL accounts, high card usage, or recent credit cleanup activity appear on the report, the lender may ask whether those changes reflect lasting improvement or short-term positioning before application.

USDA loans

USDA loans can be a good fit for eligible buyers purchasing in qualified rural areas. The program can be very attractive, but it asks for a careful match between borrower, property, and household income.

USDA files usually benefit from conservative credit behavior in the months before applying. High card balances, new installment debt, or payment patterns that look uneven can create extra friction. This is one of the clearer examples of why a stable profile matters more than a single score. A borrower with modest credit but consistent habits may present better than someone with a higher score and lots of recent account movement.

A practical way to choose your best fit

Instead of asking, “Which loan is easiest?” ask, “Which loan matches the file I have today?”

| Loan type | Often fits buyers who | Main preparation focus |

|---|---|---|

| Conventional | Have stronger credit and established account history | Lower utilization, fewer recent account changes, reserves, clean payment pattern |

| FHA | Need more flexibility for past credit issues or thinner files | Recent stability, explanation of older problems, documented improvement |

| VA | Are eligible through military service | Overall consistency, manageable obligations, clean recent credit behavior |

| USDA | Meet location and program requirements | Stable household finances, careful debt use, complete documentation |

Loan structure matters, too. Buyers comparing lending systems in other countries can see a similar principle in this guide to understanding Australian offset accounts. The product is different, but the lesson is the same. The right loan is the one that fits both the property and the borrower's financial pattern.

The strongest next step is to prepare for the program that best matches your current profile, then improve the few items that matter most for that specific lane.

How to Avoid Common Underwriting Red Flags

Many buyers work hard to improve their credit, then accidentally create new problems right before underwriting. That usually happens when someone chases speed instead of stability.

A cleaner mortgage file is not just about getting a higher score. It's about avoiding behavior that makes the file look fragile, inconsistent, or hard to document.

Why quick fixes can create new problems

Applicants whose scores rise sharply over a short period, such as 80 or more points in 6 to 12 months, are more likely to be flagged for manual review because underwriters may worry the profile reflects aggressive optimization rather than stable improvement, as discussed in this mortgage underwriting overview from Castle & Cooke Mortgage.

That doesn't mean score improvement is bad. It means underwriters want to understand how it happened.

If the change came from correcting inaccurate reporting, paying down balances, and adding consistent positive behavior, that can be a healthy story. If the file suddenly shifts because of dispute waves, questionable tradeline strategies, or a burst of new activity, the underwriter may slow down and ask for more explanation.

For people working on older derogatory accounts, Cleaning up old accounts is often more effective when it's done in a paced, documented, lender-aware way rather than as a last-minute push.

Modern credit patterns lenders may question

Alternative credit behavior can confuse buyers because it feels responsible in everyday life but may still look messy in underwriting.

Examples include:

- Heavy BNPL usage: Even when payments are made on time, fragmented short-term accounts can make the file appear busier and less stable.

- Frequent hard inquiries: Multiple recent applications can suggest rising credit dependence.

- Thin tradelines spread across fintech products: A file with many small, recent accounts may not look as durable as a simpler, older profile.

- Large unexplained changes: Sudden payoffs, unusual reporting updates, or fast dispute results can lead to follow-up questions.

Stability usually looks boring on paper, and that's often exactly what lenders want.

What stability looks like before closing

Strong mortgage preparation is often about what you don't do in the final stretch.

- Don't open new credit accounts unless your loan officer specifically says it won't affect the file.

- Don't run up card balances after pre-approval.

- Don't move money around carelessly if it will create documentation questions.

- Don't assume every negative item should be handled the same way. Some accounts call for payment, some call for documentation review, and some call for dispute attention if the reporting is inaccurate.

Credit repair before buying a home works best when it supports a stable story. Lenders want to see that your current habits match the improvement showing on the report.

Your Lender-Ready Action Plan

Most buyers don't need more random tips. They need a clear order of operations.

Start here, and work from top priority to lower priority. That prevents wasted effort and helps you focus on the parts of the file lenders care about most.

- Review all three credit reports. Look for inaccurate balances, duplicate accounts, wrong dates, mixed information, and negative items that can't be properly verified.

- Calculate your DTI. Include current debts and the projected housing payment.

- Lower revolving balances where possible. That can improve both utilization and overall file strength.

- Document your funds. Make sure your down payment, reserves, and source of funds are easy to explain.

- Pause unnecessary applications. New debt can hurt both underwriting and pricing.

- Choose the loan path that matches your profile. FHA, VA, USDA, and conventional loans don't reward the same file in the same way.

- Keep your job and payment habits steady. Underwriters value consistency.

If you're working on the credit side, this guide to 2026 credit score strategies can help you think through practical next steps.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation to better understand your options.

Frequently Asked Questions

Can I get a mortgage with a collection account?

Sometimes, yes. It depends on the loan type, the details of the account, and the rest of the file. The more important question is whether the collection is accurate, how recent it is, whether it affects underwriting for your chosen program, and whether the lender wants it resolved before closing.

Do lenders count self-employment or gig income?

They can, but documentation becomes more important. Lenders usually want income that is stable, traceable, and likely to continue. If your income changes a lot from month to month, expect closer review and more paperwork.

What is the difference between a soft inquiry and a hard inquiry?

A soft inquiry generally doesn't reflect a new borrowing decision in the same way a hard inquiry does. A hard inquiry usually appears when you apply for new credit, and a cluster of recent hard pulls can make a file look more active than a lender wants to see before mortgage approval.

Is job history always a problem if I changed employers?

Not always. A change within the same field may be easier to explain than a complete shift with unclear income continuity. The concern is not the job title by itself. The concern is whether the income used for qualifying appears stable and well documented.

Should I try to repair credit right before applying?

Only with a plan. Mortgage credit repair can help when it focuses on report accuracy, documentation, and long-term stability. It can hurt if it turns into rushed disputes, unnecessary new accounts, or confusing activity right before underwriting. Buyers in the region can learn more about Superior Credit Repair Texas services if they want local guidance with a compliance-focused process.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile. Share your feedback with Superior Credit Repair

Superior Credit Repair provides structured credit repair and credit restoration support for people preparing for mortgage approval, apartment screening, refinancing, and other major financing goals. If you want help reviewing credit report errors, dispute options, utilization issues, collections, charge-offs, or late payments before applying for a home loan, you can learn more at Superior Credit Repair.