Credit-Score Improvement Education for Petal MS Credit Score Improvement Guide

Petal MS Credit Score Improvement Guide: Practical Credit Preparation

If you are using Petal MS Credit Score Improvement Guide to work through petal ms credit score improvement guide credit score improvement guide, you may have a deadline, a recent denial, or an account you cannot reconcile. For Petal MS Credit Score Improvement Guide, the useful starting point is to compare credit mix, derogatory accounts, and score-model differences with the original statements before selecting a response. A 45-day planning window can help you separate immediate protection from longer-term rebuilding; for Petal MS Credit Score Improvement Guide, use this point to organize the documents you review.

Before sending a letter, reconstruct the account history for Petal MS Credit Score Improvement Guide. The review should identify which information is accurate, which fact is genuinely disputed, and which current behavior is still increasing risk; for Petal MS Credit Score Improvement Guide, compare this detail with the dates and balances on your reports. For you, this means a negative item and an inaccurate item are not the same thing, even when both affect the same application; for Petal MS Credit Score Improvement Guide, use this distinction when deciding whether a dispute is supported.

Main question

petal ms credit score improvement guide credit score improvement guide for Petal MS Credit Score Improvement Guide

Primary objective

a practical score-factor plan for Petal MS Credit Score Improvement Guide

Important limit

Scores vary by model and bureau, and exact point gains cannot be predicted; for Petal MS Credit Score Improvement Guide, keep this limitation in mind before the next application. The October planning example does not change that boundary; for Petal MS Credit Score Improvement Guide, use this example to separate immediate action from long-term rebuilding.

Protect Payment History

For Petal MS Credit Score Improvement Guide, start with verifiable questions about credit mix, derogatory accounts, and score-model differences. You can then compare dates, balances, ownership, and status without turning every concern into the same generic dispute; for Petal MS Credit Score Improvement Guide, compare the records before choosing the next response. For Petal MS Credit Score Improvement Guide, this example gives priority to revolving utilization because that factor is most likely to change the order of the next actions.

A documented Petal MS Credit Score Improvement Guide file may include payment calendars, score disclosures, and account opening dates. Those records create a direct connection between the reported fact and the requested correction or explanation; for Petal MS Credit Score Improvement Guide, keep the financial goal and current obligations in view. When the evidence does not support a dispute, you should record that conclusion and move the issue into a rebuilding, payment, settlement-awareness, or waiting strategy instead; for Petal MS Credit Score Improvement Guide, use this information to prepare a clear follow-up plan.

Use New Credit Carefully

For Petal MS Credit Score Improvement Guide, start with verifiable questions about derogatory accounts, score-model differences, and revolving utilization. You can then compare dates, balances, ownership, and status without turning every concern into the same generic dispute; for Petal MS Credit Score Improvement Guide, review this point against the statements and account history. For Petal MS Credit Score Improvement Guide, this example gives priority to new inquiries because that factor is most likely to change the order of the next actions.

A documented Petal MS Credit Score Improvement Guide file may include account opening dates, full credit reports, and inquiry records. Those records create a direct connection between the reported fact and the requested correction or explanation; for Petal MS Credit Score Improvement Guide, keep the explanation factual and supported by records. When the evidence does not support a dispute, you should record that conclusion and move the issue into a rebuilding, payment, settlement-awareness, or waiting strategy instead; for Petal MS Credit Score Improvement Guide, use this detail to decide whether correction or rebuilding is appropriate.

Consider someone working through Petal MS Credit Score Improvement Guide with approximately $844 associated with derogatory accounts and an application planned in 45 days. you find that score-model differences differs between two records, while revolving utilization appears consistent; for Petal MS Credit Score Improvement Guide, check the result before sending another request. The practical response is to document the one factual mismatch, protect current accounts, and avoid creating several unsupported claims merely to make the file look active; for Petal MS Credit Score Improvement Guide, keep copies of the records used for the review.

Build a Measurable Improvement Sequence

For Petal MS Credit Score Improvement Guide, start with verifiable questions about score-model differences, revolving utilization, and new inquiries. You can then compare dates, balances, ownership, and status without turning every concern into the same generic dispute; for Petal MS Credit Score Improvement Guide, connect this point to the next lending or housing decision. For Petal MS Credit Score Improvement Guide, this example gives priority to derogatory accounts because that factor is most likely to change the order of the next actions.

A documented Petal MS Credit Score Improvement Guide file may include score disclosures, account opening dates, and score disclosures. Those records create a direct connection between the reported fact and the requested correction or explanation; for Petal MS Credit Score Improvement Guide, use this information to avoid unsupported or repeated disputes. When the evidence does not support a dispute, you should record that conclusion and move the issue into a rebuilding, payment, settlement-awareness, or waiting strategy instead; for Petal MS Credit Score Improvement Guide, compare each bureau response with the original evidence.

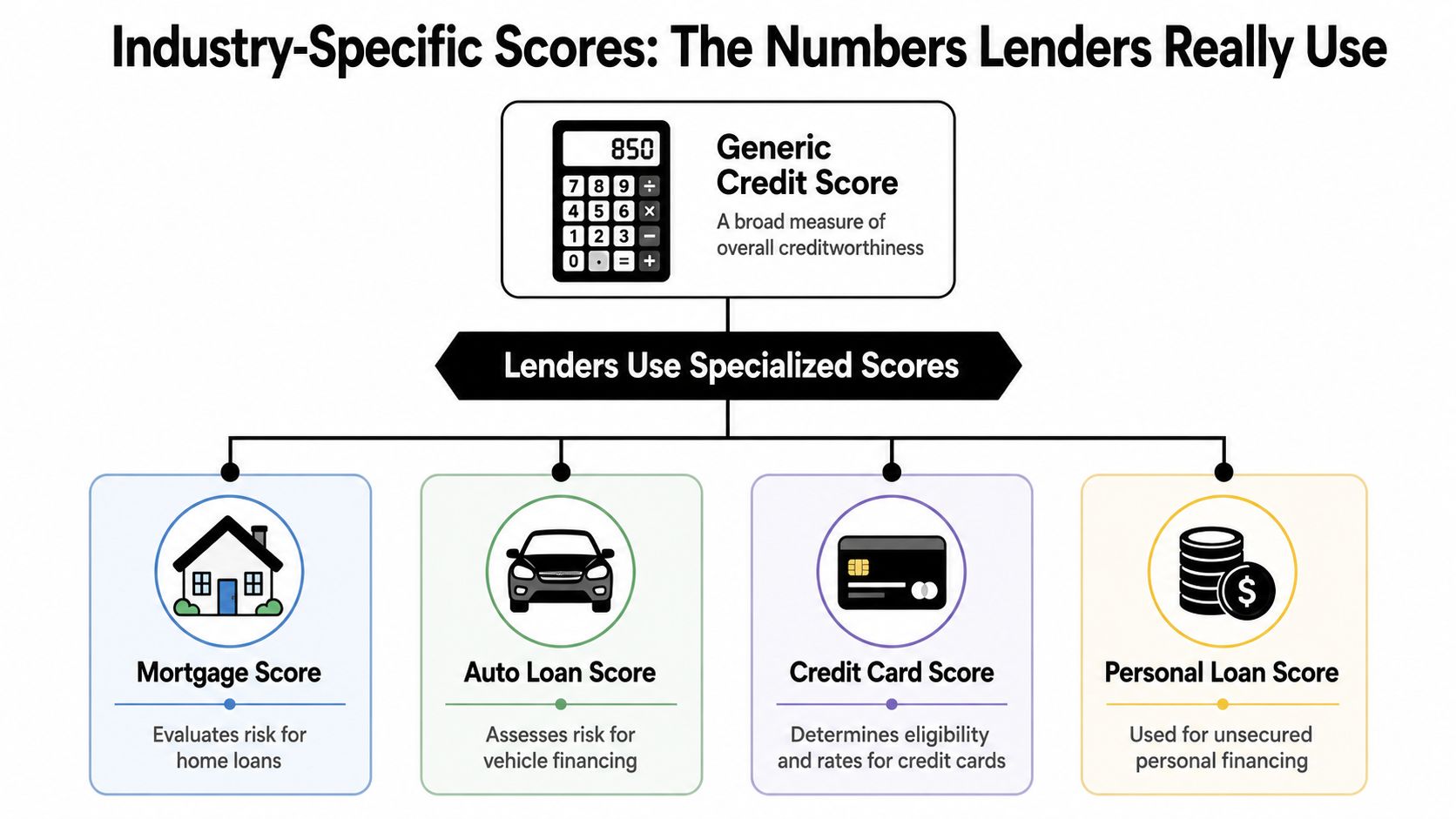

Understand the Score Factors

For Petal MS Credit Score Improvement Guide, start with verifiable questions about revolving utilization, new inquiries, and derogatory accounts. You can then compare dates, balances, ownership, and status without turning every concern into the same generic dispute; for Petal MS Credit Score Improvement Guide, keep current accounts protected while the review continues. For Petal MS Credit Score Improvement Guide, this example gives priority to bureau differences because that factor is most likely to change the order of the next actions.

A documented Petal MS Credit Score Improvement Guide file may include full credit reports, inquiry records, and lender feedback. Those records create a direct connection between the reported fact and the requested correction or explanation; for Petal MS Credit Score Improvement Guide, use the documented facts to choose the next step. When the evidence does not support a dispute, you should record that conclusion and move the issue into a rebuilding, payment, settlement-awareness, or waiting strategy instead; for Petal MS Credit Score Improvement Guide, check whether the balance, date, ownership, and status agree.

A related but different situation appears in Shannon MS Post-Bankruptcy Credit Rebuilding Guide. That resource can help you compare another approval or reporting issue for Petal MS Credit Score Improvement Guide without merging two separate fact patterns into one request.

Compare Bureau and Model Differences

For Petal MS Credit Score Improvement Guide, start with verifiable questions about new inquiries, derogatory accounts, and bureau differences. You can then compare dates, balances, ownership, and status without turning every concern into the same generic dispute; for Petal MS Credit Score Improvement Guide, keep the timeline realistic and based on verified information. For Petal MS Credit Score Improvement Guide, this example gives priority to score-model differences because that factor is most likely to change the order of the next actions.

A documented Petal MS Credit Score Improvement Guide file may include account opening dates, score disclosures, and payment calendars. Those records create a direct connection between the reported fact and the requested correction or explanation; for Petal MS Credit Score Improvement Guide, use this point to prepare for lender or landlord questions. When the evidence does not support a dispute, you should record that conclusion and move the issue into a rebuilding, payment, settlement-awareness, or waiting strategy instead; for Petal MS Credit Score Improvement Guide, compare the outcome with the goal you are working toward.

Reduce Utilization Volatility

For Petal MS Credit Score Improvement Guide, start with verifiable questions about derogatory accounts, bureau differences, and score-model differences. You can then compare dates, balances, ownership, and status without turning every concern into the same generic dispute; for Petal MS Credit Score Improvement Guide, keep the account history organized for future follow-up. For Petal MS Credit Score Improvement Guide, this example gives priority to credit mix because that factor is most likely to change the order of the next actions.

A documented Petal MS Credit Score Improvement Guide file may include inquiry records, lender feedback, and account opening dates. Those records create a direct connection between the reported fact and the requested correction or explanation; for Petal MS Credit Score Improvement Guide, use this information to make a clear and informed decision. When the evidence does not support a dispute, you should record that conclusion and move the issue into a rebuilding, payment, settlement-awareness, or waiting strategy instead; for Petal MS Credit Score Improvement Guide, use this point to organize the documents you review.

For another distinct example, review Bakersville NC Credit Bureau Error and Dispute Review. Return to the Petal MS Credit Score Improvement Guide evidence list, because the right action depends on the dates, documents, and financial goal you are working toward.

Petal MS Credit Score Improvement Guide Document and Decision Checklist

Records to organize

- Payment calendars

- Account opening dates

- Score disclosures

- Full credit reports

- Account opening dates

- Inquiry records

Errors to avoid

- Opening new credit for a quick fix during Petal MS Credit Score Improvement Guide step 1

- Chasing a single app score during Petal MS Credit Score Improvement Guide step 2

- Opening new credit for a quick fix during Petal MS Credit Score Improvement Guide step 3

- Expecting every bureau to show the same number during Petal MS Credit Score Improvement Guide step 4

- Assuming that “petal ms credit score improvement guide credit score improvement guide ” guarantees a deletion, score increase, or approval

A 45-Day Working Timeline for Petal MS Credit Score Improvement Guide

Opening review

Inventory credit mix and derogatory accounts, protect every current due date, and save the baseline reports for the October file; for Petal MS Credit Score Improvement Guide, compare this detail with the dates and balances on your reports.

Evidence stage

Compare payment calendars with account opening dates, write one precise concern, and avoid opening new credit for a quick fix while the facts are still being organized; for Petal MS Credit Score Improvement Guide, use this distinction when deciding whether a dispute is supported.

Response stage

Log delivery and response dates, compare any update with score-model differences, and preserve proof of changes for the next Petal MS Credit Score Improvement Guide decision.

Stability stage

Review revolving utilization, keep balances and applications controlled, and measure progress against better application timing rather than a daily score fluctuation; for Petal MS Credit Score Improvement Guide, keep this limitation in mind before the next application.

Petal MS Credit Score Improvement Guide Frequently Asked Questions

What should be reviewed first?

Start with credit mix, derogatory accounts, and the most recent version of payment calendars; for Petal MS Credit Score Improvement Guide, use this example to separate immediate action from long-term rebuilding. For Petal MS Credit Score Improvement Guide, the first action should match the next decision and the strongest available evidence.

Which documents are most useful?

Account opening dates, score disclosures, and full credit reports can be useful when they directly prove the fact being questioned; for Petal MS Credit Score Improvement Guide, compare the records before choosing the next response. The Petal MS Credit Score Improvement Guide file should not include unrelated paperwork simply to make the packet larger.

Can this help before an application?

The process can organize score-model differences, address supported inaccuracies, and work toward better application timing; for Petal MS Credit Score Improvement Guide, keep the financial goal and current obligations in view. It cannot force a lender, landlord, creditor, bureau, or scoring model to produce a promised result; for Petal MS Credit Score Improvement Guide, use this information to prepare a clear follow-up plan.

How long can the process take?

Timing depends on the number of accounts, response periods, documentation quality, and current payment behavior; for Petal MS Credit Score Improvement Guide, review this point against the statements and account history. The 45-day Petal MS Credit Score Improvement Guide example is a planning framework rather than a completion promise.

What should be avoided?

Avoid chasing a single app score and opening new credit for a quick fix; for Petal MS Credit Score Improvement Guide, keep the explanation factual and supported by records. Continue protecting current payments and keep a dated record of every communication tied to petal ms credit score improvement guide credit score improvement guide.

Turn the Findings Into Written Next Steps

The completed review for Petal MS Credit Score Improvement Guide should identify the account or score factor, list the evidence, record the action date, and explain what you will do while waiting. For Petal MS Credit Score Improvement Guide, that written sequence centers on petal ms credit score improvement guide credit score improvement guide and clearer understanding of report versus score. A clear record helps you follow up consistently without repeating unsupported requests; for Petal MS Credit Score Improvement Guide, use this detail to decide whether correction or rebuilding is appropriate.

Request a Free Credit AnalysisResults for Petal MS Credit Score Improvement Guide vary by the consumer file, documentation, bureau or furnisher responses, scoring model, lender or landlord standards, and timing. Superior Credit Repair does not promise specific deletions, approvals, score increases, or completion dates; for Petal MS Credit Score Improvement Guide, check the result before sending another request.