You pull your credit report because you're getting serious about buying a home. You expect to see a few old balances, maybe a late payment, maybe a collection you already know about. Then you notice several hard inquiries. Some look familiar. Some don't. One might be from a lender name you barely recognize.

That's where many homebuyers get stuck. They hear that hard inquiries hurt mortgage approval, search for hard inquiry removal, and find advice that swings between two extremes. Either “don't worry about it” or “remove them all.” Neither is helpful when you're trying to get lender-ready.

A better approach starts with validation first. Before you try to remove anything, you need to confirm what each inquiry is, whether you authorized it, whether it's duplicated, and whether it matters for your mortgage timeline. That process protects you from wasting time on legitimate inquiries that will stay, while helping you act quickly on inquiries that may be inaccurate, unauthorized, outdated, unverifiable, or misleading.

Table of Contents

- Understanding Hard Inquiries and Their Role in Mortgages

- Your Step-by-Step Guide to Auditing Credit Report Inquiries

- Crafting and Submitting a Formal Inquiry Dispute

- Advanced Strategies When Disputes Are Unsuccessful

- Building a Lender-Ready Profile Beyond Hard Inquiries

- When to Partner with a Professional for Credit Restoration

- Frequently Asked Questions

Understanding Hard Inquiries and Their Role in Mortgages

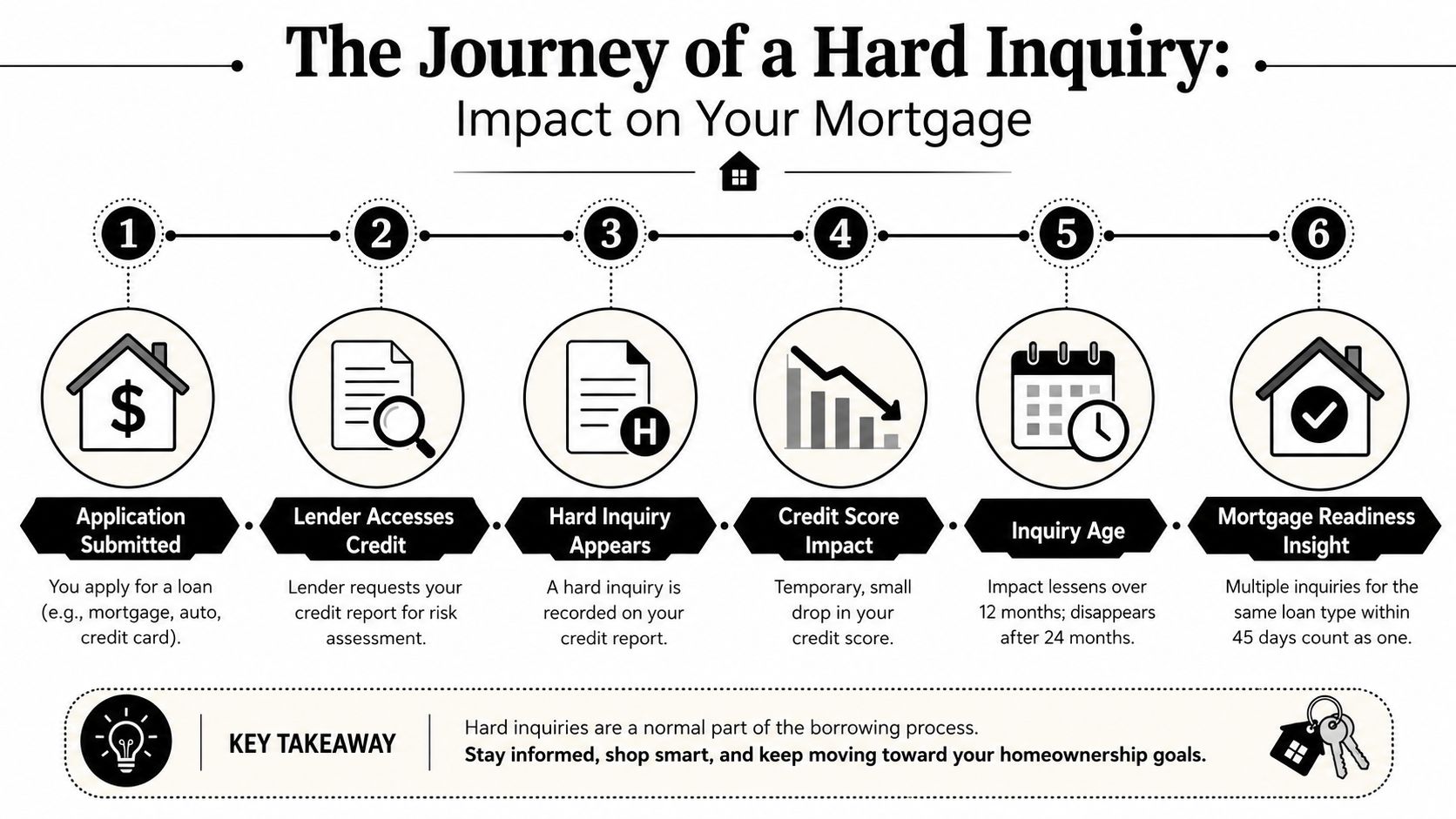

A hard inquiry happens when a lender checks your credit report because you applied for credit. That can happen with a mortgage, auto loan, credit card, personal loan, or private student loan. A soft inquiry is different. Soft inquiries usually happen when you check your own credit, receive a prequalification offer, or go through certain non-lending screenings, and they don't carry the same weight in lending decisions.

Think of a hard inquiry as a lender taking a snapshot of your recent credit-seeking activity. The lender isn't just looking at your score. They're also looking at behavior. Have you been applying for several new accounts at once? Are you opening new debt right before trying to qualify for a mortgage? Those patterns can raise questions, even if the score change itself is small.

What a hard inquiry actually means

The core rule is straightforward. Legitimate hard inquiries remain on a consumer's credit report for exactly 24 months and are automatically removed by the credit bureaus. However, their impact on credit scores typically fades much sooner, usually within 12 months for most scoring models like FICO® according to Credit Karma's explanation of hard inquiries.

That rule helps calm a lot of unnecessary panic. If you authorized the application, the inquiry usually isn't something you can remove with a phone call. It has a set reporting life. What matters more is whether it's accurate and whether it's recent enough to affect a lender's review of your file.

If you want a refresher on how inquiries fit into the larger score formula, Superior Credit Repair explains credit scores in plain English.

Why mortgage lenders pay attention

Mortgage underwriting is about stability. A lender wants to see that your credit profile supports the payment you're about to take on. Hard inquiries can matter because they suggest recent borrowing activity, but they are only one piece of the file.

Practical rule: A legitimate inquiry is usually a temporary issue, not a permanent obstacle.

For homebuyers, context matters. One mortgage-related inquiry during normal preparation doesn't carry the same meaning as several scattered applications for credit cards, personal loans, and retail financing while you're trying to qualify for a home loan. That's why a hard inquiry review should never happen in isolation from the rest of your mortgage preparation.

If part of your plan includes future real estate goals beyond your primary home, a financing overview like the LendingXpress investment property guide can help you understand how lenders think about risk across different property types.

Your Step-by-Step Guide to Auditing Credit Report Inquiries

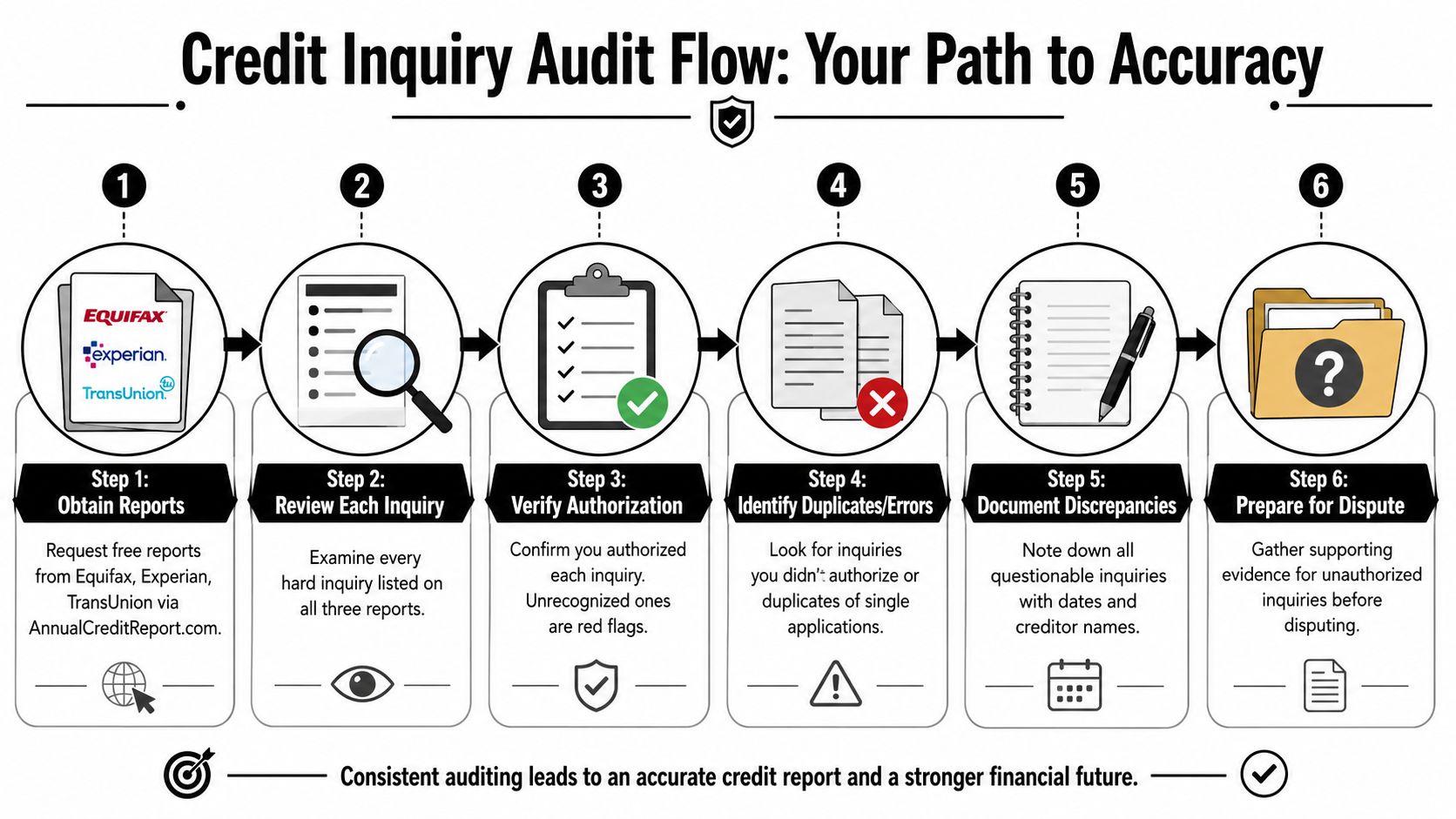

The most effective hard inquiry removal strategy starts long before a dispute letter. It starts with an audit. That means slowing down, reviewing every inquiry line by line, and deciding what belongs, what needs explanation, and what may need to be challenged.

Start with all three credit reports

Pull reports from Equifax, Experian, and TransUnion. Don't rely on only one bureau because an inquiry may appear on one report and not another. Place them side by side if possible.

Then create a basic tracking sheet in a notebook, spreadsheet, or notes app. You don't need anything fancy. A simple layout works:

| Bureau | Creditor Name | Date Listed | Do I Recognize It | Category | Notes |

|---|---|---|---|---|---|

| Experian | Example Lender | Month/Day/Year | Yes/No | Authorized / Duplicate / Unfamiliar | Add details |

This process gives you something many consumers don't have when they start disputing. A clean record of facts.

Use a simple inquiry audit system

Sort each inquiry into one of three categories:

- Authorized and correct. You remember applying, the date makes sense, and the company name matches the lender or partner bank involved.

- Unfamiliar or questionable. You don't recognize the company, the date seems wrong, or the inquiry doesn't match your credit activity.

- Possible duplicate or error. You made one application, but the reporting looks inconsistent or repeated.

It's important to recognize that not every inquiry that looks unfamiliar is unauthorized. Store cards, fintech lenders, and partner banks often report under a legal or servicing name that looks different from the brand you remember.

The score impact also needs perspective. The impact of a single hard inquiry on a FICO Score is typically less than five points. The primary concern for mortgage lenders is not the small score dip but the pattern of multiple recent inquiries, which may signal risk, as noted in this hard inquiry credit impact overview.

Questions to ask for every inquiry

Use the same checklist for each entry so you don't make rushed assumptions.

- Did I apply for credit around this date? Think mortgage preapproval, auto financing, a new credit card, or a personal loan.

- Could the lender name be different from the brand I saw? This happens often with retail cards and financing platforms.

- Was this tied to identity theft, fraud, or a mistaken pull?

- Does this look duplicated compared with another bureau entry or another lender line?

- Is this inquiry the problem, or am I overlooking bigger issues like collections, utilization, late payments, or charge-offs?

A careful audit prevents emotional disputes. Facts win more often than frustration.

If your review turns up broader report problems, not just inquiries, it helps to learn how to dispute inaccurate credit items in a more organized way.

By the end of the audit, your goal is simple. You should know which inquiries are fine, which need more research, and which may justify a formal dispute.

Crafting and Submitting a Formal Inquiry Dispute

If an inquiry appears unauthorized, inaccurate, or tied to identity theft, a formal dispute is the right next step. Hard inquiry removal then transitions from general advice to a documentation-based legal process.

A good dispute is calm, specific, and supported by records. It does not rely on anger, long personal stories, or broad claims that everything on the report is wrong. Credit bureaus and furnishers respond better when the issue is narrow and clearly documented.

What to include in the dispute letter

Your dispute should identify you and identify the inquiry with precision. Include:

- Your identifying information. Full name, current address, date of birth, and the file details the bureau requires.

- The exact inquiry being disputed. Name of the creditor as shown, bureau where it appears, and date listed.

- A clear reason for the dispute. State whether the inquiry was unauthorized, fraudulent, duplicated, or otherwise inaccurate.

- Supporting documents. Identity theft records, account statements, proof of address, and copies of report pages with the inquiry highlighted if relevant.

Short works better than dramatic. For example, “I am disputing the hard inquiry from [creditor name] dated [date] because I did not authorize this credit application. Please investigate and remove the inquiry if it cannot be verified as authorized.”

If you need help organizing a compliant letter, this guide on how to dispute inaccurate credit report items can help you structure it properly.

How to send the dispute and track the response

You can usually dispute through an online portal or by mail. Online is convenient. Certified mail creates a stronger paper trail. For serious cases, especially identity theft or repeated reporting errors, a paper trail can be valuable because it documents what you sent and when the bureau received it.

A simple tracking log can include:

| Item | Example entry |

|---|---|

| Bureau | TransUnion |

| Date sent | Month/Day/Year |

| Delivery method | Certified mail or online portal |

| Inquiry disputed | Creditor name and date |

| Documents enclosed | ID, proof of address, report copy, FTC report |

| Response deadline | Note based on receipt date |

| Result | Deleted, verified, corrected, pending |

Under the Fair Credit Reporting Act, there is an important enforcement path when the issue is unauthorized activity. Under the FCRA, consumers can sue creditors for failing to remove unauthorized hard pulls. To strengthen a dispute, you can also file an identity theft report with the FTC and a formal complaint with the CFPB, according to American Express's credit inquiry guidance.

Keep copies of every letter, every upload, every response, and every mailing receipt. If the issue escalates, your records matter.

If the bureau verifies the inquiry as authorized, that doesn't always mean the matter is over. It means the bureau believes the furnisher confirmed it. At that point, the quality of your evidence determines whether escalation makes sense.

Advanced Strategies When Disputes Are Unsuccessful

Sometimes a bureau comes back with a verification result and the inquiry stays. That can happen even when the consumer still believes something is wrong. When that happens, you need a more strategic response, not a louder one.

When a CFPB complaint makes sense

A complaint with the Consumer Financial Protection Bureau can be useful when you have already disputed the inquiry, preserved your records, and still haven't received a meaningful response. This isn't a shortcut. It's an escalation path.

A strong CFPB complaint includes a timeline. State when you found the inquiry, when you disputed it, what documents you submitted, what the bureau or creditor said, and why the response remains inadequate. Attach the same evidence you used in your dispute package.

This approach works best when the issue is concrete. Unauthorized inquiry. Mismatched identity data. Clear documentation of fraud. Inconsistent reporting between bureaus. It is less effective when the inquiry is legitimate and the request is to remove it because you no longer want it there.

How to contact the creditor directly

Direct contact with the creditor is a separate path from a bureau dispute. It isn't a legal demand in the same way. It's a customer-service or file-accuracy request.

While most content states legitimate inquiries cannot be removed, a nuanced strategy involves contacting the creditor's fraud or customer service department directly to request a "goodwill deletion for file accuracy," which may succeed in specific cases where a formal dispute would fail, as described in this discussion of creditor-side inquiry deletion requests.

That approach is worth considering in narrow situations:

- The lender name is confusing and you need clarification before disputing further.

- The inquiry came from a mistaken application flow or incomplete process.

- The pull followed a fraud alert or identity mix-up and the creditor can see the issue internally.

- You need documentation quickly because you're preparing for mortgage underwriting and want the creditor's written position.

Keep your request factual. Ask whether the creditor can confirm authorization, explain the inquiry, or review a deletion request for file accuracy. Don't present it as a guaranteed method, because it isn't. Some creditors will decline. Some may respond only in writing. Others may point you back to the bureau process.

If a formal dispute fails, switch from arguing to documenting. The stronger your records, the better your next move.

Building a Lender-Ready Profile Beyond Hard Inquiries

Hard inquiry removal gets a lot of attention because it feels concrete. You can see the entries, count them, and focus on them. Mortgage approval, though, usually turns on broader signs of financial stability.

A helpful mindset shift is this. Cleaning up inaccurate inquiries is good credit hygiene. Building a lender-ready file is what moves most homebuyers closer to FHA, VA, USDA, or conventional mortgage preparation.

What lenders usually care about more

If you're putting your time somewhere, start with the areas that shape underwriting decisions most heavily.

- Payment history. Lenders want to see that bills are paid on time, especially recent obligations.

- Credit utilization. High revolving balances can make a file look stretched, even when payments are current.

- Collections and charge-offs. These often create more underwriting friction than a few inquiries.

- Account stability. Older, well-managed accounts can help show consistency.

- Debt-to-income concerns. A mortgage lender looks at the relationship between your income and your monthly obligations, not just your score.

Experian notes that legitimate hard inquiries automatically fall off a credit report after 24 months, and their impact on credit scores typically diminishes or becomes unscoreable after just 12 months, making them a low-priority factor for long-term credit health in this Experian explanation of hard inquiry timing.

That's why a person with a few old inquiries but solid payment history may be in better mortgage shape than someone with no recent inquiries and several active delinquencies.

Practical moves that strengthen mortgage readiness

Here's where many borrowers see better long-term progress.

| Focus area | What to do |

|---|---|

| Payment history | Bring every open account current and protect on-time payments going forward |

| Revolving balances | Pay down credit cards strategically and avoid running balances back up |

| Collections | Review for accuracy and understand how unresolved collections may affect loan preparation |

| Account age | Keep seasoned accounts open when appropriate |

| New applications | Pause unnecessary credit activity while preparing for underwriting |

If you're working on the bigger picture, this resource on nationwide credit score improvement offers practical rebuilding ideas that go beyond inquiry cleanup.

Mortgage credit repair works best when it's tied to the full profile. That includes late payment dispute help when reporting is inaccurate, collections dispute help when balances or ownership are questionable, charge-off dispute help when information is misleading, and smarter utilization management when cards are near their limits. For many first-time homebuyers, those steps matter more than chasing every legitimate inquiry on the report.

When to Partner with a Professional for Credit Restoration

Some people can manage inquiry disputes on their own with a clean audit trail and a little patience. Others are dealing with a file that's much more layered. That's where professional credit restoration can make sense.

Signs the do-it-yourself route may not be enough

The do-it-yourself process tends to get harder when the issue isn't just one inquiry. A file may also contain collections, medical collection credit repair issues, charge-offs, late payments, repossessions, identity theft concerns, or mixed reporting across bureaus. Add a home purchase timeline, and the risk of missed details goes up.

It can also become inefficient when you're trying to prepare for FHA loan preparation, VA loan preparation, USDA loan preparation, or conventional mortgage approval while juggling lender conditions, apartment approval concerns, and debt-to-income cleanup at the same time.

Why professional support can help

A compliance-focused credit repair company should approach the file as a structured review process, not a promise machine. The value is in identifying inaccurate, outdated, unverifiable, or misleading items, organizing documentation, handling dispute workflow, and helping you rebuild stronger habits while results develop over time.

If you've wondered whether it makes sense to pay someone to fix your credit, the better question is whether your situation calls for guidance, documentation support, and a lender-readiness strategy. For many homebuyers, especially those working through several issues at once, that can be a practical decision.

Frequently Asked Questions

Can legitimate hard inquiries be removed?

Usually, no. If you authorized the credit application, the inquiry generally stays for its normal reporting period. The main exception is when the inquiry was unauthorized, fraudulent, duplicated, or otherwise inaccurate.

Will removing a hard inquiry guarantee mortgage approval?

No. Mortgage approval depends on the full credit profile, income, debts, documentation, loan program rules, and lender standards. Hard inquiries are only one piece of the decision.

Should I dispute every inquiry I don't recognize right away?

Not immediately. Audit it first. Some lender names appear differently on the report than they did during the application process. Confirm the facts before filing a dispute.

Do hard inquiries matter more for first-time homebuyers?

They can matter if they show a pattern of recent credit-seeking activity close to mortgage application time. Still, first-time homebuyers usually benefit more from improving payment history, reducing utilization, and addressing report errors across the file.

Can hard inquiry removal improve credit score?

It can, but the effect is often modest and depends on the file. The stronger reason to pursue removal is accuracy. If an inquiry is unauthorized or incorrect, it should be challenged because your report should reflect only legitimate activity.

Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. If you're preparing for a home purchase, trying to rebuild after credit challenges, or dealing with credit report errors that affect financing, you can request a free credit analysis or consultation through Superior Credit Repair to better understand your options. Results vary based on your credit file, documentation, creditor responses, account history, and current credit behavior.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile. Share your experience with Superior Credit Repair