You may be in this position right now. You have a car payment you need to get rid of, and someone else is willing to take the vehicle. It could be an ex-spouse, an adult child, a sibling, or a friend. On the surface, the solution feels simple. Hand over the keys, let them make the payments, and move on.

That's where people get hurt.

A car loan is usually tied to the borrower, not just the vehicle. So when people ask, can car loans be transferred to another person, the honest answer is yes in limited cases, but usually not in the casual way people hope. Most of the time, a true transfer requires lender approval, a new credit review, updated title paperwork, and a formal process that looks a lot like a brand-new loan.

If you skip that process and rely on trust, you can stay legally responsible for the debt while someone else controls the car. That can create credit damage, debt-to-income problems, and serious mortgage issues later.

For readers preparing to buy a home, this matters more than most auto finance articles admit. A car loan that still reports in your name can affect underwriting even if someone else has been making the payments. If those payments stop, the fallout lands on your credit file first.

Table of Contents

- Introduction Is Transferring a Car Loan Possible

- Why Most Auto Lenders Prohibit Loan Transfers

- Understanding Loan Assumption The Official Transfer Process

- The Major Risks of Informal Payment Agreements

- Safer Alternatives to Transferring Your Car Loan

- How Your Credit Profile Impacts Your Options

- Your Actionable Checklist Before Making a Decision

- Frequently Asked Questions About Car Loan Transfers

- Can a co-signer be removed or take over the car loan

- What happens in divorce or separation

- Can you transfer a car loan to a family member to keep the same terms

- Should you check for existing finance before buying a used car from someone else

- Should you pay someone to help with your credit before applying again

Introduction Is Transferring a Car Loan Possible

Yes, car loans can sometimes be transferred to another person, but that answer needs a hard qualification. In most cases, the lender won't let one person directly step into your place and keep everything unchanged.

Chase says mainstream lenders generally refuse transfer requests and that “most car loans can't be assumed by someone else,” and describes direct transfer as a “rare and unique circumstance” in its guide on how to transfer a car loan to another person. That matches what many borrowers find in real life. The contract often controls the answer, and if it doesn't allow assumption, the original borrower usually remains responsible.

That distinction matters because people often confuse using the car with owing the debt. They are not the same thing.

Practical rule: If the lender hasn't approved the change in writing, assume the loan is still yours.

The official path, when available, is usually called loan assumption or a replacement arrangement. It is not a favor between two people. It is a lender-controlled approval process.

If your real goal is financial relief, getting rid of the payment, or preparing for a mortgage, you need to think beyond the word “transfer.” The right question is this: How do I remove my legal and credit responsibility safely?

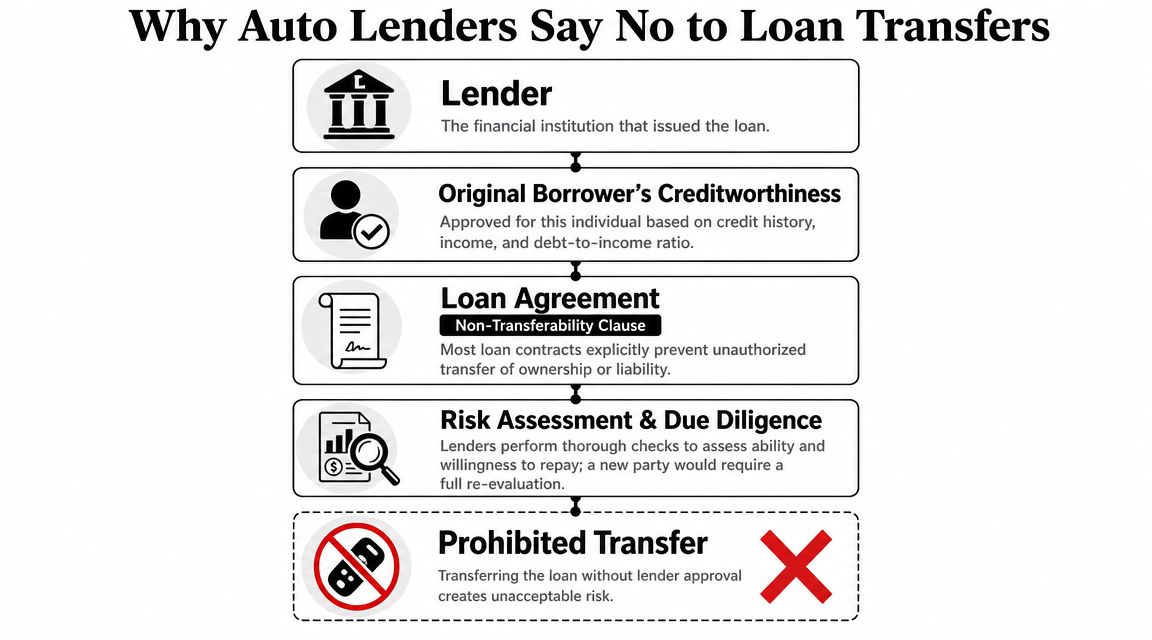

Why Most Auto Lenders Prohibit Loan Transfers

The lender approved you, not the car

Auto lenders don't underwrite a vehicle by itself. They underwrite a person. When the loan was issued, the lender looked at your credit profile, your income, your existing debt, and your ability to handle the payment.

That is why loan transfers are so restricted. The lender didn't agree to lend money to “whoever ends up driving the car.” The lender agreed to lend money to you.

Think of it this way. A car loan may be secured by the vehicle, but the payment promise is still personal. If a different borrower comes in, the lender has a different risk profile in front of it.

Why lenders treat transfers as fresh risk

Lenders are cautious for a reason. Capital One notes that where transfers are possible, the new borrower usually goes through full approval, including income verification, budget review, and a credit check, and says the person taking over the loan typically needs to have a “great credit score” in its article on whether you should transfer a car loan to another person. That same source also cites LendingTree reporting that the average new-car payment reached $767 per month in Q4 2025, up 2.8% from Q4 2024. That's a large monthly obligation, and lenders don't hand that risk to another person without underwriting.

Here is the lender's logic in plain English:

- Credit risk changes: The new driver may have weaker payment history, lower income, or higher debt.

- Contract rights matter: If the agreement doesn't permit assumption, the lender has no reason to allow it.

- Collateral isn't enough: The car can lose value. The lender still cares about the borrower's ability to repay.

- Compliance matters: Title, registration, insurance, and lien records need to match the actual legal arrangement.

The lender is not being difficult. The lender is protecting its ability to collect.

This is why informal transfer requests usually fail, and why a borrower who wants out of the payment often needs a different strategy.

Understanding Loan Assumption The Official Transfer Process

What loan assumption actually means

When people ask whether they can transfer a car loan to another person, the only clean version of that idea is usually loan assumption. That means the lender agrees to let another qualified borrower take legal responsibility for the debt under a formal process.

This doesn't happen automatically. Upstart explains that in major auto-lending markets, a car loan is usually not directly transferable unless the contract is explicitly assumable, and if the agreement lacks assumption language, the original borrower typically remains responsible until the lender approves a transfer or a refinance replaces the debt in its guide on transferring a car loan to another person.

So the first question isn't whether your friend or family member is willing. The first question is whether your loan documents and your lender allow the process at all.

What the new borrower usually has to provide

Where assumption is allowed, the process usually looks very similar to a new loan application. Poonawalla Fincorp explains that transfers are commonly structured as a loan assumption or replacement agreement, not a simple name change, and the new borrower must qualify independently with documentation such as ID, address proof, income proof, insurance, and a credit review. The title and registration also have to be updated, as described in its article about how to transfer a car loan to another person.

In practical terms, expect these steps:

Review the contract

Check whether assumption is allowed at all.Call the lender

Ask for the exact process, required documents, and whether the current loan must be current and in good standing.Have the new borrower apply

The lender usually reviews income, debt obligations, budget, and credit.Wait for approval

Approval is not guaranteed. The new borrower may also get different terms in some cases.Update ownership records

Title, registration, and insurance need to be changed so the legal owner, borrower, and insurer line up.

A lot of people underestimate that last step. If the paperwork doesn't match reality, you can create a mess involving ownership disputes, insurance gaps, or both.

| Issue | Informal arrangement | Formal assumption |

|---|---|---|

| Legal borrower | Original borrower | Approved new borrower |

| Credit reporting risk | Stays with original borrower | Moves according to approved structure |

| Title and registration | Often mismatched | Updated through proper process |

| Lender approval | None | Required |

If you're hoping for a quick signature and a key handoff, that's not this process. Official transfer is possible in some cases, but it's paperwork-heavy for a reason.

The Major Risks of Informal Payment Agreements

Why handshake deals go wrong

This is the part people try to talk themselves out of. They say, “It's my cousin.” Or, “My ex said they'll handle it.” Or, “My son has been paying me on time.”

None of that changes the lender's records.

OneMain Financial highlights a problem many articles barely explain. If the transfer is only informal, the original borrower remains legally responsible unless the lender formally approves an assumption, and the debt can still affect debt-to-income calculations, payment history, and credit file stability, which can create problems for future mortgage applications in its article on whether you can transfer a car loan to someone else.

That means several things can happen at once:

Missed payments hit your credit report

If the other person pays late, your file can reflect the damage.Repossession risk stays tied to you

If the loan defaults, the lender pursues the legal borrower.Insurance problems can become your problem

If the vehicle is wrecked and insurance is not handled correctly, the loan balance doesn't disappear.You may lose control of the asset

Someone else has the car, but you still owe the lender.

For readers trying to protect a mortgage timeline, learn what late payments mean for your credit. A single account reporting poorly at the wrong time can make underwriting far more difficult.

Trust does not replace lender approval.

Why this can wreck mortgage timing

Mortgage lenders look at more than your score. They look at debt-to-income ratio, payment history, and whether your file is stable and understandable.

An informal car arrangement creates the opposite of stability. The debt still appears tied to you. The monthly obligation may still count against you. If a payment is missed during mortgage review, you may have to explain a problem you thought was no longer yours.

That's why my advice is firm here. Don't hand over a financed car based on a side agreement if your name remains on the loan. It's not a harmless shortcut. It's a credit and legal exposure that can stay alive for months or years.

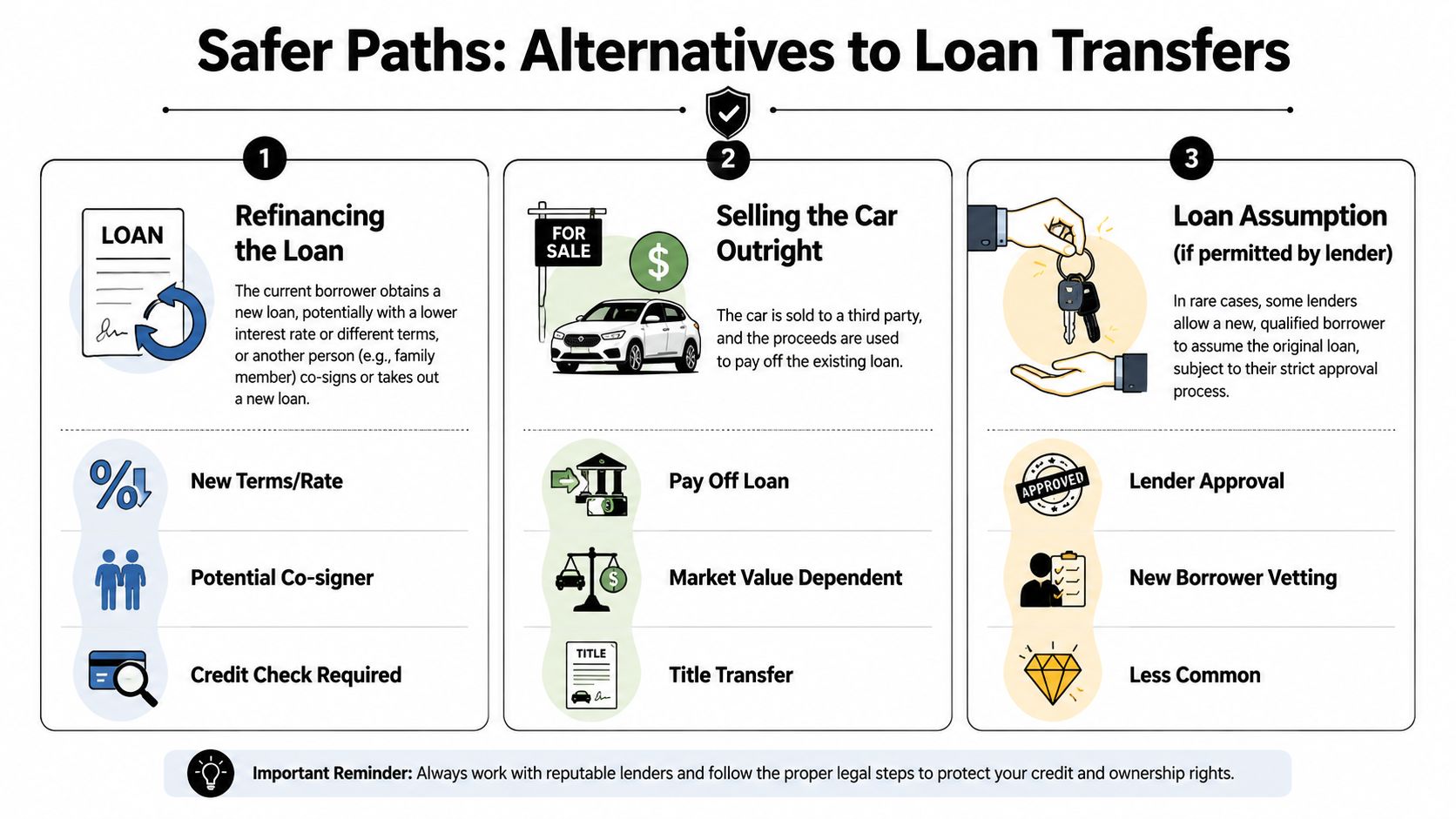

Safer Alternatives to Transferring Your Car Loan

Option one let the other person get their own loan

This is often the cleanest fix. Instead of trying to “take over” your loan, the other person applies for their own financing and buys the car from you. Your lender gets paid off, the debt closes, and legal responsibility is separated clearly.

That structure is usually safer because it matches reality. The person who wants the vehicle becomes the person legally financing it.

If that borrower's credit is borderline, they may need time to improve it first. In that situation, working on payment history, utilization, and report accuracy may help future financing options. Some consumers also need to step back and address larger cash-flow pressure first. If multiple debts are squeezing the budget, it may help to review ways to find debt relief with Cash Compass before making another rushed auto decision.

Option two sell the car and close the debt

Selling the vehicle outright is often the most practical answer when the loan cannot be assumed and the payment no longer fits your budget.

This can happen through:

- A private sale: Often worth exploring if you have a willing buyer and can coordinate payoff with the lender.

- A dealership sale or trade process: Often simpler administratively, especially when time matters.

- A structured payoff plan: Useful if the vehicle's value and loan balance don't line up cleanly.

The hard part is emotional, not technical. People keep bad car loans too long because they don't want to accept a loss, reset transportation plans, or admit the original purchase no longer works.

If your priority is buying a home later, protecting your file matters more than protecting pride.

Option three restructure your broader debt picture

Sometimes the car loan is only one symptom. The underlying issue is that your monthly obligations are stacked too high, and the auto payment is just the loudest one.

That's where a full credit and debt review matters. If your reports contain inaccurate, outdated, unverifiable, or misleading items, a documentation-based dispute process may improve the overall picture over time. If your utilization is high, lowering revolving balances may strengthen your file before you revisit refinancing or mortgage prep. If you're planning ahead for homeownership, it can help to boost credit for mortgage approval.

Superior Credit Repair can review credit reports, help identify questionable negative items, and explain rebuilding steps in plain English as one part of a broader lender-readiness plan. Results vary because every file, creditor response, and account history is different.

Choose the option that actually removes liability, not the option that only feels easier this week.

How Your Credit Profile Impacts Your Options

If your credit is already strained

If your credit file already has late payments, high utilization, collections, or unstable account history, your room to maneuver is smaller. A lender may be less flexible. A refinance may be harder. A sale may become the safest path because default would be worse.

The biggest mistake here is delay. Borrowers with stressed credit often wait for a handshake arrangement to “work itself out.” That usually ends with more risk, not less clarity.

A weak file also means every fresh problem matters more. One more late auto payment can reinforce a pattern lenders already dislike. This is why strong credit education for future homeowners matters before you make a car decision that follows you into a mortgage application.

If you are rebuilding for homeownership

If you're a first-time buyer or preparing for FHA, VA, USDA, or conventional mortgage review, think about this issue through an underwriting lens.

Ask yourself:

- Will this debt still appear to be mine?

- Could this arrangement create a surprise late payment?

- Will the monthly obligation still hurt my debt-to-income profile?

- Can I document the change clearly if a mortgage lender asks?

Those are the right questions.

A car loan handled cleanly can support stability. A car loan handled casually can undermine months of careful progress. For future homeowners, the cleanest path is usually the best path.

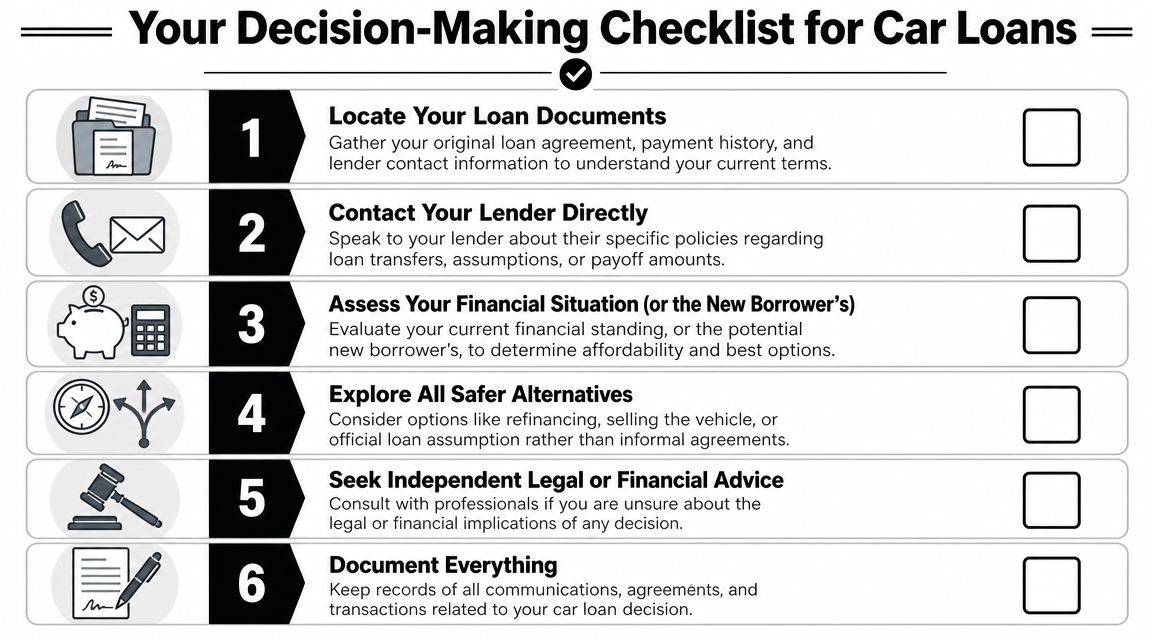

Your Actionable Checklist Before Making a Decision

Six moves to make before you sign or hand over keys

Use this checklist before you let anyone drive off with a financed vehicle.

Pull your loan agreement

Look for assumption language or restrictions on transfer.Contact the lender directly

Ask whether assumption, replacement financing, or payoff coordination is available.Request a current payoff quote

You need exact numbers before comparing alternatives.Check the car's realistic market value

That tells you whether sale proceeds can satisfy the debt or whether you may need extra funds.Review the other person's financial strength

Will they qualify for financing on their own, or are you being asked to carry the risk for them?Document your next steps

Keep records of calls, emails, payoff statements, and ownership paperwork.

Upstart's guidance is useful here. In major auto-lending markets, a car loan is usually not directly transferable unless the contract is explicitly assumable, and if it is not, the original borrower typically remains responsible until the lender approves a transfer or a refinance replaces the debt. If you're also trying to repair your file before a larger financing move, it helps to have realistic expectations about understanding credit repair timelines.

If you can't explain the final arrangement in one clear sentence, don't proceed yet.

Frequently Asked Questions About Car Loan Transfers

Can a co-signer be removed or take over the car loan

Sometimes, but not by request alone. The lender usually has to approve a refinance, replacement loan, or another formal change. If the lender does nothing, the original structure usually stays in place.

What happens in divorce or separation

A divorce agreement between two people does not automatically change the lender's rights. If both names remain tied to the loan and the lender has not approved a formal change, the lender can still look to the obligated borrower or borrowers for payment. This is why auto debt after separation causes so many post-divorce credit problems.

Can you transfer a car loan to a family member to keep the same terms

Usually no. Family relationship does not override lender policy. In some cases, a lender may allow formal assumption, but many mainstream loans are not set up that way.

Should you check for existing finance before buying a used car from someone else

Yes. If you're the person taking over a vehicle arrangement, verify ownership and debt status carefully before paying anyone. If you want a buyer-focused guide on how to verify outstanding finance on cars, that resource explains why hidden finance can create serious problems.

Should you pay someone to help with your credit before applying again

Sometimes it makes sense, but only if the help is compliant, documentation-based, and realistic. If you're weighing that decision, review this guide on Paying someone to fix your credit. The right help should focus on report accuracy, legal dispute procedures, and long-term rebuilding habits, not promises.

If you're trying to protect your credit while dealing with a car loan problem, Superior Credit Repair can review your credit report, help identify inaccurate or questionable items, and explain a step-by-step plan for improving your credit profile. You can request a free credit analysis or consultation to better understand your options. Results vary based on your credit file, documentation, creditor responses, and current account behavior.

Was this guide helpful?

Superior Credit Repair Online provides educational credit guidance for individuals and families preparing for major financial goals like buying a home, applying for a mortgage, refinancing, or rebuilding after credit challenges.

If this information helped you better understand your credit report or your next steps, we would appreciate your honest feedback. You are welcome to share your experience with Superior Credit Repair on our Google Business Profile.